.svg)

%2Bcopy.webp)

.svg)

%20(1).jpeg)

.jpg)

.webp)

Mergers and acquisitions gathered pace across the micromobility sector in 2025, as operators, manufacturers, and service providers turned to consolidation to strengthen their positions in a more disciplined market. This year’s deals have largely focused on survival, scale, and strategic fit, spanning shared mobility operations, e bike brands, software, insurance, and multimodal platforms.

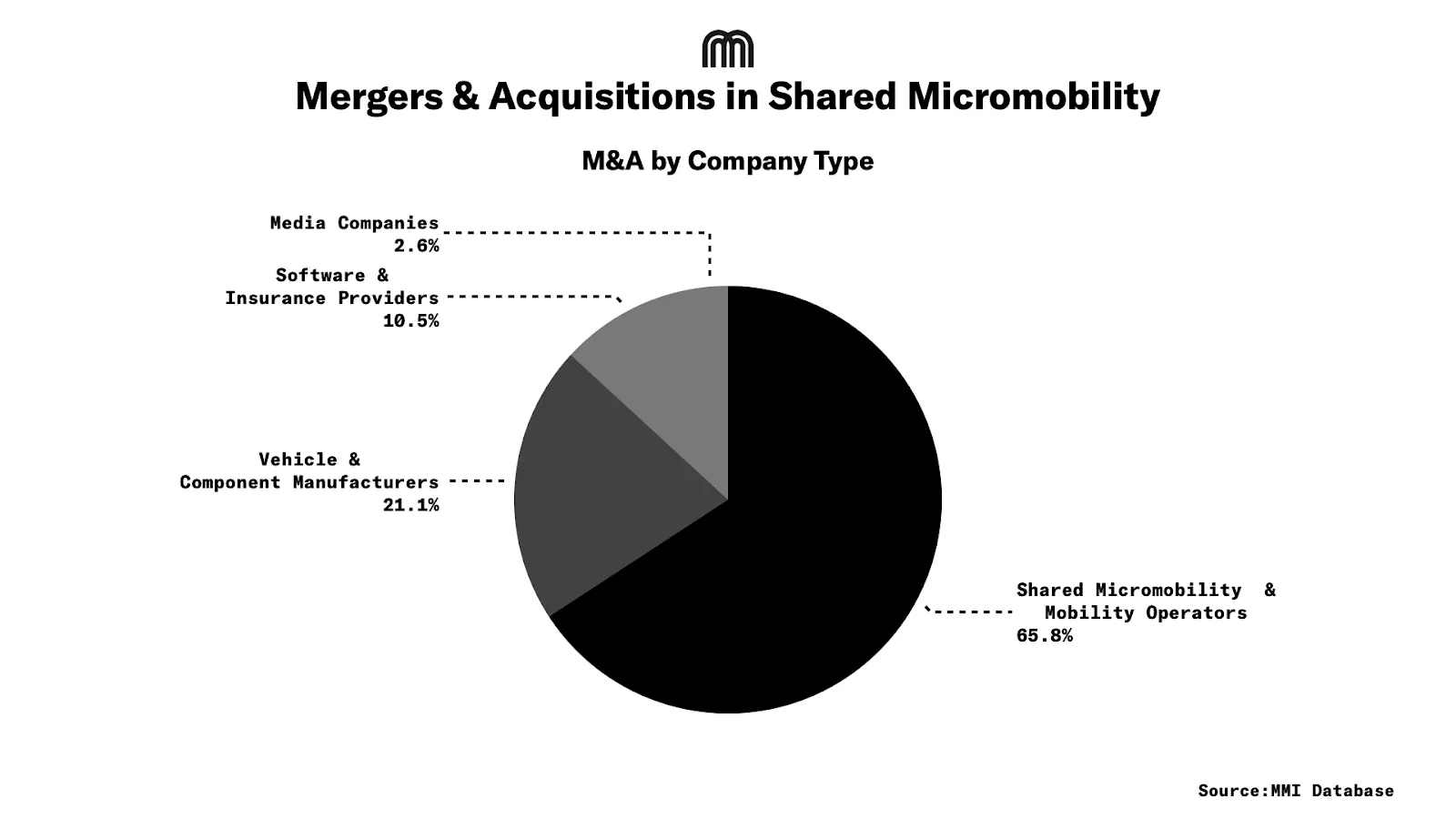

About one third of acquisitions since 2017 have occurred in the shared operators segment, underscoring how challenging it is to build a sustainable business model in an asset heavy industry like shared micromobility.

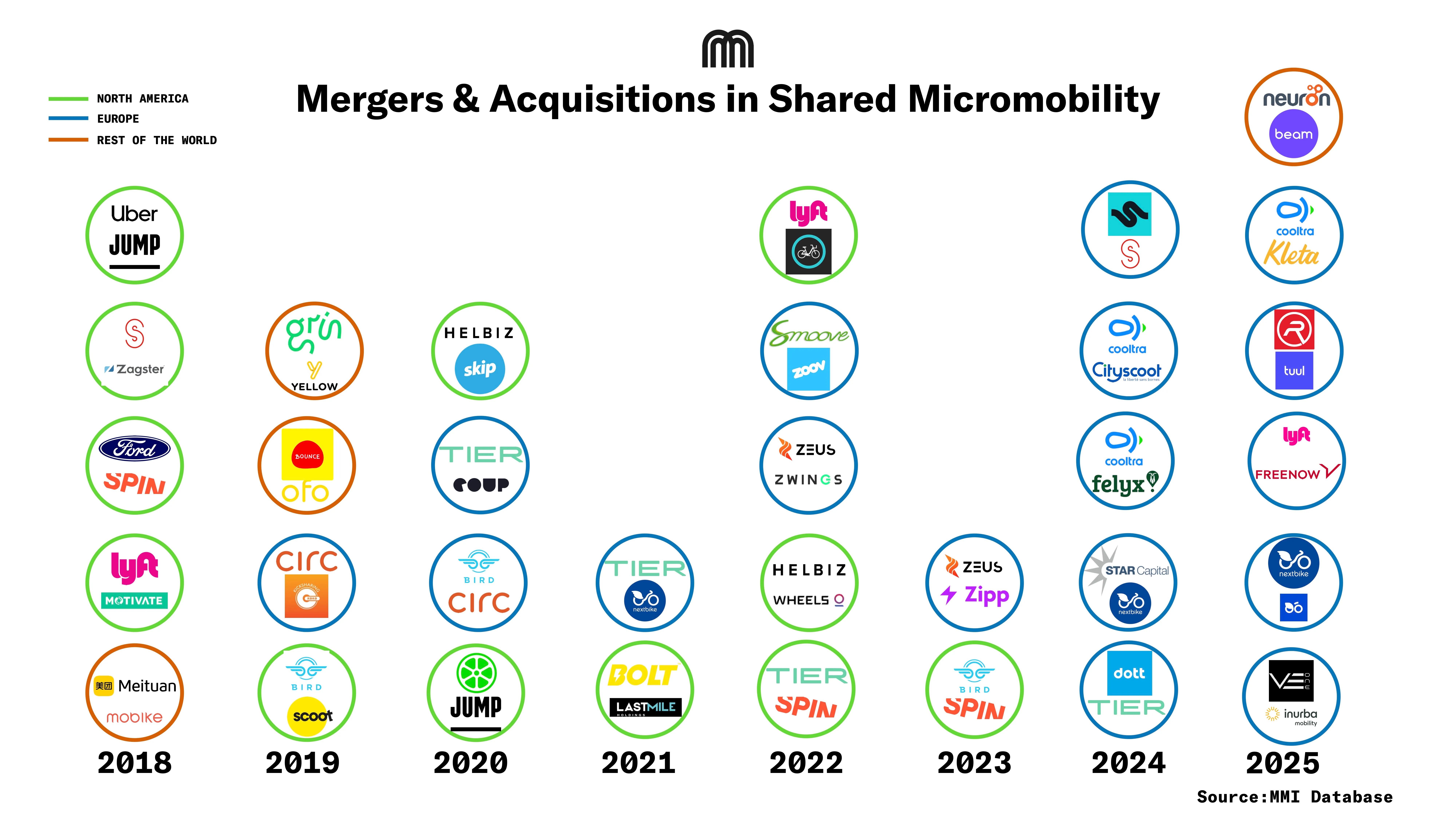

M&A since 2017

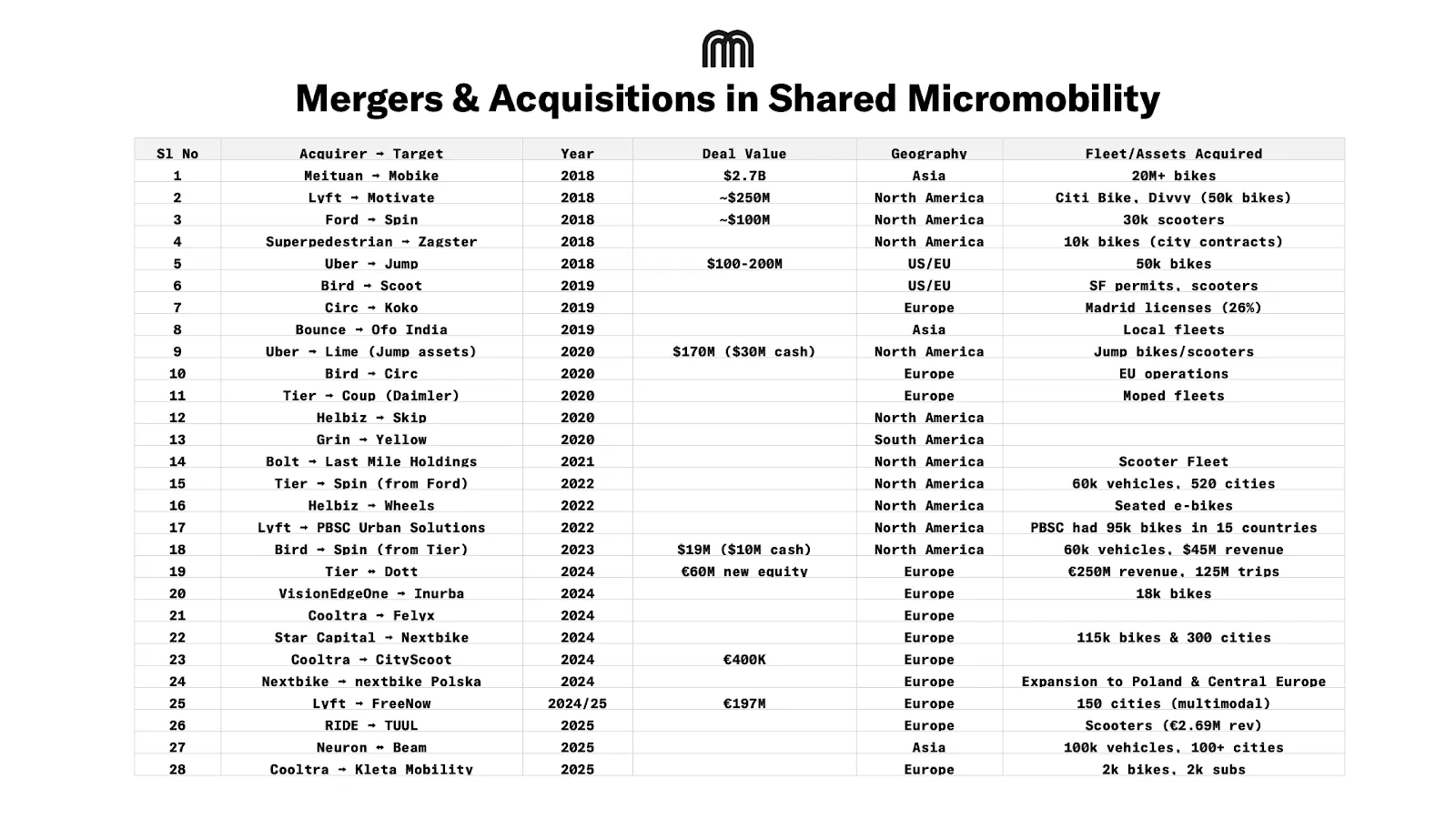

From 2017 onward, operator M&A followed a clear arc: rapid expansion, followed by consolidation and, in some cases, reversal. Early landmark deals included Meituan’s ~$2.7bn acquisition of Mobike in 2018, which accelerated China’s bike-share shakeout, and Lyft’s acquisition of Motivate in mid-2018 (reported around ~$250m), securing control of major US bike-share systems such as Citi Bike and Divvy.

Outside Europe and North America, consolidation followed a similar logic. In India, Bounce acquired Ofo India’s local assets and operations in 2019, marking one of the earliest examples of a global dockless bike-share player exiting a market and handing over fleets and learnings to a regional operator better positioned to navigate local economics.

The Defining Deal: Lime and Uber

The most influential transaction of this period came in May 2020, when Uber exited direct micromobility operations by transferring Jump’s assets to Lime. The deal included $170m in new funding led by Uber, with $30m in cash and the remainder reflecting the value of Jump’s assets, while Uber took an estimated ~29% equity stake in Lime. Uber retained exposure without running fleets, while Lime absorbed Jump’s bikes, scooters, permits, and technology, cementing its position as the world’s largest shared micromobility operator.

Curious Case of Spin

Since founding, Spin went through a series of M&A’s.. Ford acquired Spin for ~$100m in 2018 at peak optimism. Tier bought it in 2022 for an undisclosed amount from Ford, gaining 60k vehicles across 520 cities. In September 203, Bird acquired Spin from Tier in 2023 for just $19m ($10m cash), an 81% cut despite Spin’s $45m revenue.

Survival of the Fittest

Around the same time, Bird acquired Scoot (2019) and later Circ (2020) to expand in Europe, while Tier acquired Daimler’s Coup moped assets, a move that later highlighted the difficulty of shared moped economics. Meanwhile, earlier in April 2019, Germany-based operator Circ had acquired Spain-based startup Koko and had then acquired 26% of e-scooter licenses in Madrid.

By the early 2020s, consolidation accelerated further. Superpedestrian acquired Zagster in 2018, combining its self-balancing scooter technology with Zagster’s experience in city-run bike-share contracts. In 2022, Helbiz completed the acquisition of Wheels, folding Wheels’ US scooter operations into Helbiz’s publicly listed platform. As its strategy evolved beyond shared scooters, Helbiz later rebranded as Micromobility Inc., reflecting a broader focus on mobility services, media, and infrastructure rather than pure fleet operations.

Felyx merged with Cooltra in March 2024, forming one of Europe’s largest shared electric two-wheeler operators while continuing to operate under their respective brands. The combined group now serves 30+ cities across nine countries with ~28k vehicles.

In August 2022, South Korean e-scooter company Gbike acquired Hyundai’s micromobility platform ZET. GBike completed this acquisition to boost market share and gain access to ZET’s fleet management technology.

In the US, Bolt Mobility, based in Miami and co-founded by Olympic gold medalist Usain Bolt, acquired Last Mile Holdings in January 2021. However, just a year later, Bolt Mobility ceased its operations after running out of funds.

2024: Dott Topped Europe’s Shared Micromobility Market

The most recent chapter came in 2024, when Tier and Dott merged, creating one of Europe’s largest shared micromobility operators and marking a decisive shift from competitive expansion to operational consolidation across major EU cities.

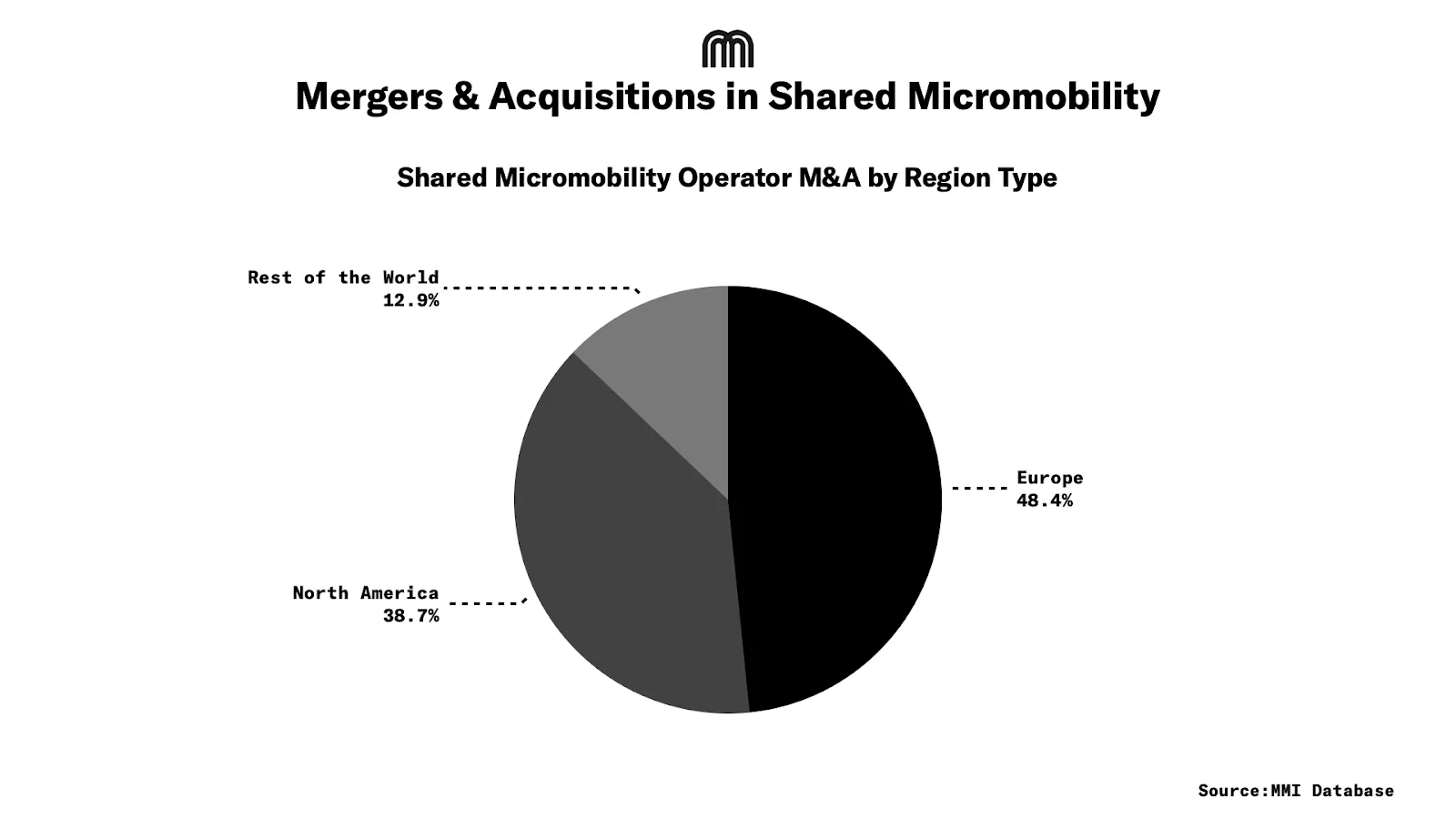

Out of ~30 acquisition deals in the shared micromobility space since 2017, about 15 were from Europe & 12 were from North America, and the rest were from Asia & South America.

Acquisitions in 2025

In Europe, VisionEdgeOne, backed by GCM Grosvenor, bought Barcelona-based Inurba Mobility and its roughly 18k bikes to deepen its hold on long-term city contracts, while Nextbike Group took full control of nextbike Polska to secure its lead across Central and Eastern Europe’s public bike-share schemes.

At the multimodal level, Lyft agreed to acquire FreeNow for approximately €197m, unlocking instant access to 150 European cities and pulling taxis, ride-hailing, and micromobility into a single app.

In the Baltics, RIDE Mobility acquired Estonia’s TUUL scooters and related IP after the operator’s revenue fell to €2.69m in 2024 and losses widened. The deal kept TUUL’s fleet on the road while giving riders one unified service for bikes and scooters.

In October 2025, Cooltra Group acquired Kleta Mobility’s Barcelona urban bike-subscription business unit (undisclosed terms), adding 2k+ active subscriptions and a 2k+ bike fleet (including e-bikes) to Cooltra’s Spain operations.

Undisputed Leader in the Asia-Pacific Region

In Asia-Pacific, Singapore-based rivals Neuron and Beam agreed to merge into the region’s largest shared operator across 100+ cities, with Neuron co-founder Zachary Wang moving up to Chairman and Global CEO, Beam CEO Alan Jiang becoming CEO for Asia, and Beam president Deb Gangopadhyay shifting into a strategic adviser role.

Shifts & Shakeouts

Europe and North America's shared micromobility markets consolidated through 30+ M&A deals since 2017, reducing fragmented competition to regional champions.

During the early years in the 2017-2019 period, most of the acquisitions were strategized on capturing the market with cash-rich deals. About 10 deals that were executed in this period generated a cumulative deal value of $3.5B+.

As funding tightened after 2020, asset-heavy and sub-scale operators exited or were absorbed, accelerating M&A activity and licence transfers. During this period, deals focused on absorbing companies that could not withstand the pandemic or build sustainable unit economics. The deal values during this period were much lower, highlighting how VC-subsidized models were unsustainable.

Micromobility M&A’s have moved from aggressive expansion to careful consolidation, as companies focus on staying viable and building scale in a capital intensive market. The past decade has narrowed the field to a smaller group of regional and global leaders that combine operations, technology, and partnerships. By 2025, consolidation is no longer a reaction to pressure but the standard way the industry grows.