.svg)

%2Bcopy.avif)

.svg)

%20(1).jpg)

.webp)

.webp)

Welcome to Micromobility Pro, a bi-weekly publication which is part of The Micromobility Newsletter, where we deep-dive into the financials of micromobility companies and share exclusive insights tailored for professionals and members.

Micromobility Europe 2026 | Berlin

Only two days left!!! New Year Sale Ends on January 31st!

Micromobility Europe 2026 brings the global micromobility community together for two days of high-impact ideas, products, and connections shaping what’s next for the industry. Join us in Berlin on June 2-3, 2026, at Arena Berlin.

New Year Sale tickets are available for €349, but the offer ends January 31. Get your tickets today!

Startups - This’s your moment too!

Applications for the Startup Arena are now open, with discounted participation available until January 31.

Submit your application before January 31st to get your spot at a discounted price.

The clock is ticking. Grab your tickets before it’s too late!

[Sponsor/Exhibit] | [Speak at the Event] | [Exhibit as a Startup] | [Get A Free Pass]

Spots are filling fast! Secure yours today and be part of Europe’s bespoke event for all things micromobility.

Tickets for Micromobility America 2026| SFO | Nov 11-12 is right here!

Contents:

- Recap on London Part 1

- London’s parking crisis

- The operators

- Santander Cycles

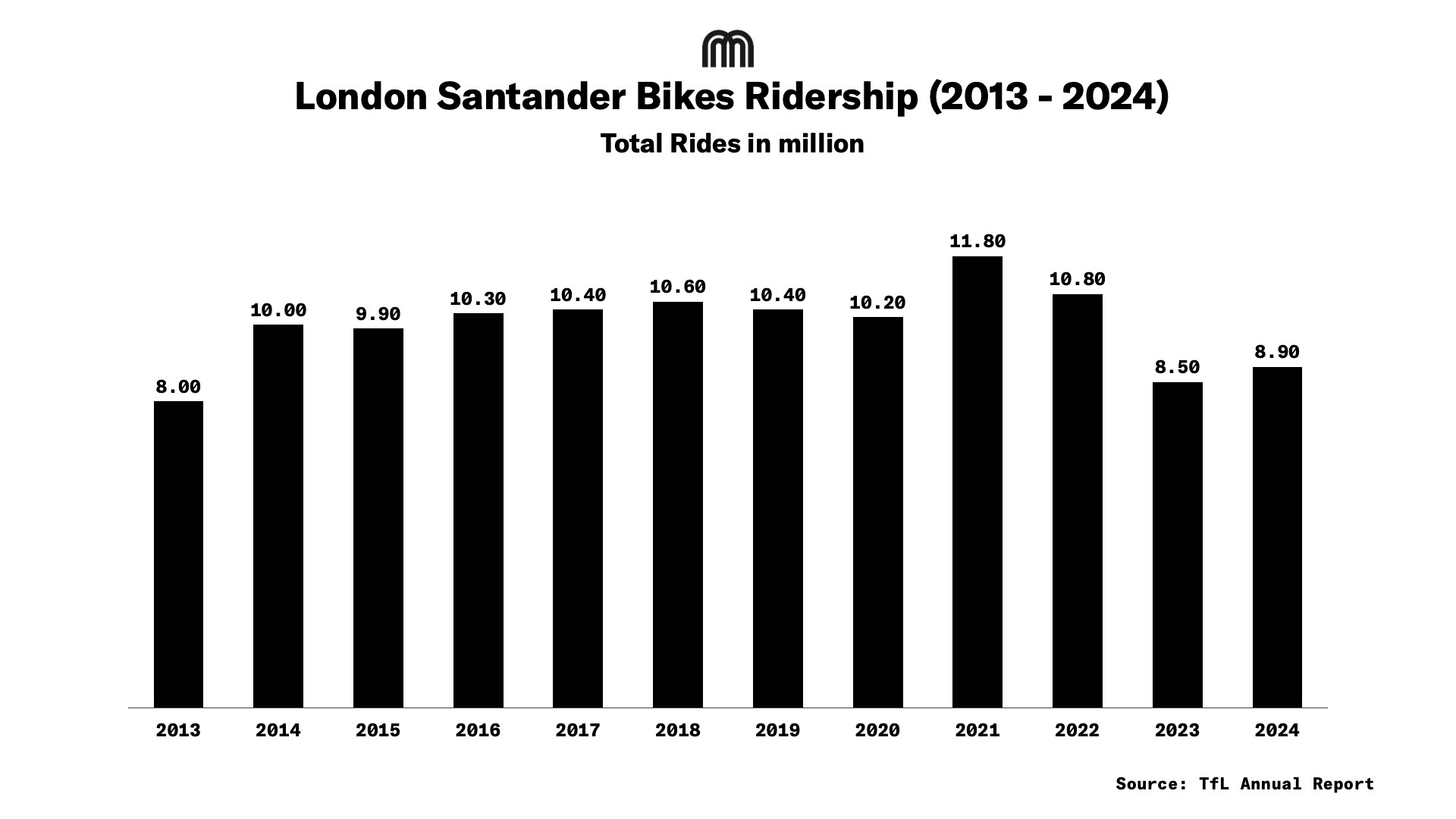

- Chart: Santander Ridership 2013-2024

- Lime

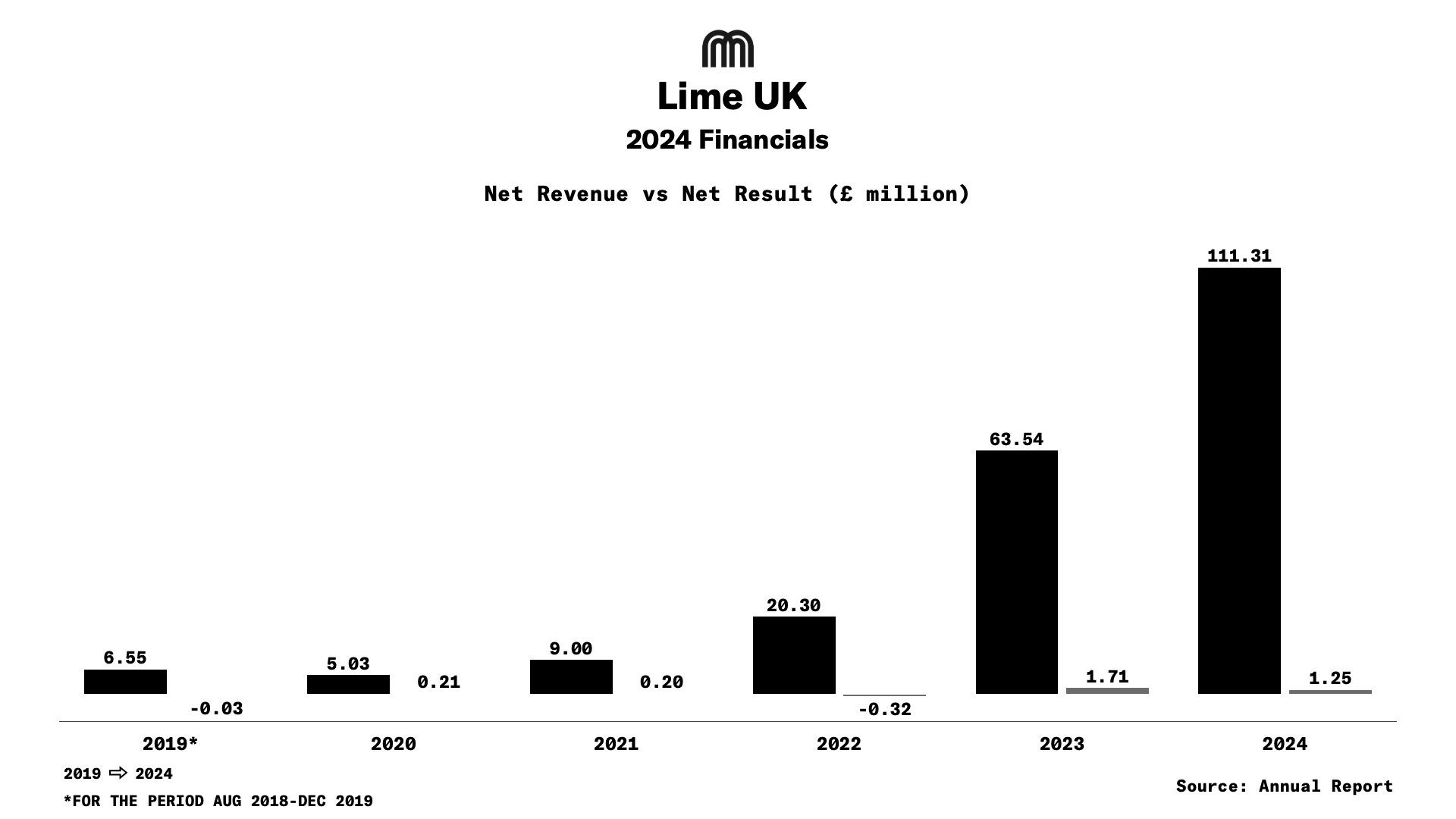

- Chart: Lime UK Revenue vs Net Result (2019-2024)

- Forest

- Voi

- Santander Cycles

- A unique market for a unique city

Recap on London Part 1

In the first part of our series about London’s micromobility scene, we looked at the history and future of the sector in the region. What we found was a city and a sector that shape one another; and this is a theme that also runs through today’s piece.

Throughout this article, we’re going to be focusing on the regulatory and competitor landscape in London. To put that a different way, while the first part of this series is about how the past influences the future of micromobility in England’s capital, today we’re taking a good hard look at precisely what’s going on.

So let’s get into it.

The layout of London: An invisible influence

One of the most important elements to consider when thinking about micromobility in London is the sheer scale of the city and how it’s divided. London consists of 32 local boroughs and the City of London Corporation, with each of these areas having a separate local highway authority. Effectively, London is not that joined up.

There is some oversight, with the Mayor of London, Transport for London (TfL), and the Greater London Authority (GLA) having a range of strategic powers that can influence how people move around the city, but it’s the boroughs that look after the local highways, as well as parking arrangements — both of which are of vital importance for micromobility.

What this amounts to is there’s no single, London-wide statutory licensing regime for dockless or shared bikes. Sure, TfL issues guidance (such as the Dockless Bike Share Code of Practice), but, typically, boroughs enter commercial concession agreements with operators to set local rules, such as the number of vehicles allowed, parking requirements, and service standards. This is most commonly done on an individual basis, not as a broad policy that sweeps across the entire city.

This disparity is the lens through which London’s micromobility scene is read through, and is a vital key in understanding how the city operates. In some senses, micromobility in London isn’t the story of one city, it’s the story of 32 boroughs.

London’s parking crisis

If there’s one element that dominates London’s issue with shared micromobility, it’s parking. It doesn’t take long to find complaints about e-scooters or e-bikes littering the streets of the capital — but things have improved, and will continue to do so.

The issue with parking dates back to around 2018, when dockless operators like Ofo and Mobike arrived in London. At the time, there was no specific legal framework to license or control these schemes. Change came quickly though. Transport for London responded by issuing a Dockless Bike Share Code of Practice that same year.

What’s most important to note is that this wasn’t legally binding, instead it merely complemented existing law. Still, operators had to comply with normal regulations, such as obstruction and highway safety rules. But it’s an imperfect solution.

A 2019 analysis by Steer showed the limits of this loose approach, as neither the boroughs nor TfL could actually technically license dockless bike sharing. Instead, they used memorandums of understanding (MoUs) and voluntary agreements combined with general powers (such as obstruction laws) to manage the schemes.

This light-touch approach enabled rapid growth, but it also laid the groundwork for inconsistency and weak enforcement across the boroughs — something anyone in London could see was an issue.

Thankfully, this has been confronted. From around 2024, central London authorities began moving decisively toward what’s known as “hybrid” or “virtual docked” systems. In November of 2024, TfL announced a new enforcement policy for dockless e-bike parking. Operators can now be fined when bikes are left blocking pavements on TfL-managed land, including red routes and station forecourts.

The policy explicitly aims to align e-bike parking with rental e-scooters, which already must use designated bays. TfL also committed £1 million to help boroughs deliver around 7,500 dedicated micromobility bays.

The shift is underway — and it’s spreading. This means in London’s boroughs, the aforementioned voluntary arrangements are being replaced by formal concession contracts. For example, Hounslow’s first regulated contracts with Forest and Voi include elements such as stricter parking controls. Expect to see much more of this in the coming years.

It’s important to note that the game isn’t over though, far from it. The existence of London’s 32 boroughs means there’s little unity, and, because of this visible borders have occurred, with some bikes crossing boundaries and stopping working because of geofencing, leading to pile-ups.

There’s much more to do.

Thankfully, operators are throwing their weight behind making parking shared bikes in London a problem of the past. Some are currently expanding street patrols, investing in rebalancing and deploying geofencing, delivering in-app parking penalties, and incorporating AI-based enforcement. Together, these changes mark a clear shift away from pure dockless freedom toward a managed, bay-based micromobility system.

Regulatory systems will catch up eventually, but that’s the state we find ourselves in. This is an ideal moment, then, to reflect on the operators.

The operators

As we’ve said, a lot of the London regulation of shared micromobility is influenced by the fact there are 32 boroughs with different rules. This approach to regulation is reflected in the fact there are several strong players in the scene.

This part of the article is going to sum up some of those key players, and how they fit into London’s puzzle.

Santander Cycles

Santander Cycles is London’s longest running docked bike-hire scheme. It’s the OG, in other words. The scheme is owned by Transport for London and sponsored by Santander UK.

What separates it from many of the other operators is it’s a fully docked system and does not operate e-scooters, which are handled separately under TfL trials. Santander has more than 12,000 bikes in service and around 800 docking stations across inner and central London, making it one of the largest docked networks in Europe.

Coverage includes most central boroughs, from Camden and Westminster to Southwark, Hackney, and the City of London. Since its launch in 2010, the scheme has recorded well over 100 million journeys, cementing its position as a core part of London’s transport system.

Aside from its launch (which is one of the defining moments in London’s micromobility journey), one of the biggest shifts for Santander Cycles occured in September 2022, when electric-assisted bikes were introduced. Following this, TfL expanded this fleet rapidly, going from roughly 600 to 2,000 e-bikes during 2024. Uptake with these vehicles has been strong, with TfL saying that e-bikes are hired at about twice the rate of classic bikes.

Santander Cycles aren’t resting on their laurels though. In December 2025, TfL announced a major upgrade programme under a new contract with operator Serco, running to at least 2031. Planned improvements include in-dock e-bike charging, a redesigned app with QR-code unlock, and modernised terminals.

Despite rising competition from dockless e-bikes, record monthly usage in late 2025 suggests Santander Cycles remains the cornerstone of London’s cycling network. The OGs of London’s micromobility scene won’t be going anywhere soon.

Lime

Lime is one of the dominant private operators on London’s streets — and is arguably the first company that springs to mind when they think about the city’s micromobility sector.

The company launched its shared e-bikes in London around 2018 and has expanded rapidly since, becoming a central player in the city’s e-bike boom.

In 2021, Lime was selected by Transport for London as an authorised operator for London’s e-scooter trial, and two years later, it secured a place again in the second phase of the trial. Since then, Lime has grown both fleet size and usage, reporting sharp year-on-year increases in trips and peak demand rising by around 90%.

Lime now operates across roughly 16 London boroughs under TfL and borough agreements, including Camden, Hackney, Southwark, Islington, and Hammersmith & Fulham. After a record global growth year in 2023, the company pledged about £25 million of investment in London in 2024. That expansion, however, has brought closer scrutiny over parking, regulation, and battery safety, especially as boroughs tighten controls on dockless bikes.

Whatever happens next in London’s micromobility scene, Lime will be part of it.

Forest

Forest (formerly HumanForest) is a London-based dockless e-bike operator that positions itself as a lower-cost and more sustainable alternative for shared micromobility. Its ad-supported model offers riders free daily trips (often between 10 and 30 minutes), which is helping attract a dedicated audience.

Forest launched in London in 2020 as HumanForest, rebranding to Forest in 2023. Growth accelerated in 2024 and 2025, supported by high-profile marketing, the rollout of its bright blue “River” e-bike fleet, and increased visibility across central and west London.

In January 2025, Forest raised €15.3 million to fund further fleet expansion and international ambitions. Later that year it introduced tiered pricing and, in December 2025, announced a partnership with Octopus Energy By late 2025, Forest declared it had operating around 20,000 e-bikes in London.

Basically, keep an eye out for Forest. They’re coming to upset the status quo.

Voi

Voi, the Swedish micromobility operator, has a smaller stake in London than the other businesses we’ve analysed, but it still has massive ambition.

The company entered the UK market in 2021 after hiring a former Bird UK chief to lead its expansion. Between 2022 and 2023, Voi focused on consolidation and compliance, rolling out a wide variety of schemes, including a pilot of its computer-vision parking validation.

However, Voi has been openly critical of the UK regulatory environment. Its leadership has blamed Brexit and national law for delaying legalisation of shared e-scooters and has described London’s trial as overly restrictive, arguing scooters are over-regulated compared with largely unregulated dockless e-bikes.

Today, Voi operates around 4,000 e-bikes in London. The company argues the city could sustain far larger fleets, but says the absence of a formal tender process or fleet caps allows dominant players to crowd the market.

Fundamentally, Voi wants a more unified policy across the city.

A unique market for a unique city

What makes London a tough place to operate is also what makes it so special: the sheer scale of the place. The 32 boroughs, in some senses, make it tough for a single company to dominate entirely, allowing a range of different businesses to operate within its borders.

Of course, London isn’t perfect; there are plenty of problems that need ironing out, but we have faith these will be fixed in the years to come. In its current state, though, London is a micromobility environment that encourages collaboration and experimentation.

England’s capital is a unique place — and the micromobility scene reflects that.

Got your micromobility moment to share? Email us at press@micromobility.io

Loving the vibe? Hop on and ride with us! Subscribe!

.png)