.svg)

%2Bcopy.avif)

-2%20(1)%20(1).webp)

.svg)

.webp)

.jpg)

%20(1).jpeg)

.jpg)

Welcome to Micromobility Pro, a bi-weekly publication which is part of The Micromobility Newsletter, where we deep-dive into the financials of micromobility companies and share exclusive insights tailored for professionals and members.

Introducing the First Wave of Early Partners and Sponsors at MME 2026🌟 🇩🇪

Micromobility Europe 2026 brings together the companies building and backing the future of urban mobility, from global leaders to the innovators shaping what comes next.

We’re proud to welcome an incredible group of early partners including McKinsey, Rivian’s ALSO, LYFT, RYDE, Dott, NextBike, POLIS, Urban Sharing, Navee, CityFi, Valeo, XYTE, Vmax, Microlino, Standab, Atom, alongside more companies joining us this year.

CALL FOR STARTUPS!

Building something bold in micromobility? This is your moment.

Pitch at the Startup Arena, compete for the Awards, and get seen by the people shaping the future of mobility at MME 2026.

[Sponsor/Exhibit] | [Speak at the Event] | [Get A Free Pass]

And to find all about Micromobility America | Nov 11-12 | Palace of Fine Arts, SFO - HERE!

Contents

- Introduction

- Where it Started

- Scaling Up

- The Merger

- The Painful Middle

- 2025 Financials

- Chart: Revenue vs EBIT and 2025 Quarterly Revenue

- Table: P&L Snapshot - 2025

- Cash Position, Debt, & Fleet

- Chart: Average Age of Dott’s Vehicles

- Table: Consolidated Balance Sheet - 2025

- Dott vs. Voi: Two Paths to the Same Milestone

- Chart: Voi vs Dott Comparison

- Where Dott Goes From Here

Introduction

When Dott launched in Brussels in January 2019, the micromobility industry was still in its gold rush phase. Companies were flooding cities with scooters, burning cash to grab market share, and treating profitability as a problem for later. Dott took a different view from the start.

“We had three first convictions: First, disciplined growth - starting small and launching in a few key cities to prove the model is useful, sustainable, and can be profitable. Second, Select scooter hardware built for shared usage - more resistant, shipped with spare parts. And third, doing it right and responsibly - having 100% in-house operations, no juicers, no gig economy from the first day.”

- Maxim Romain, CEO & Cofounder, Dott

6 years later, Dott posted €7.2m in Adjusted EBITDA for FY2025, its first profitable year ever. In an industry that spent years treating losses as a feature rather than a bug, Dott got there by doing almost everything the slow way.

Where It Started

Dott was founded in 2018 by Henri Moissinac and Maxim Romain, both of whom had already seen the first wave of micromobility up close. Both had worked at Ofo, the Chinese bike-sharing giant. They came back together with a shared belief that the industry was solving the right problem in the wrong way.

The initial seed round raised €20m. Within months of its January 2019 Brussels launch, Dott closed a €30m Series A led by EQT Ventures and Naspers to develop a more durable scooter and expand across European cities. What made Dott unusual early on wasn’t the funding or the hardware, it was the operations model. While competitors relied on contract workers (known as “juicers”) to charge and redistribute scooters, Dott built its own warehouses and repair teams from day one. The logic was simple - if you own your operations, you control your costs and your quality. It made the early years harder. It also made the company more resilient.

By 2020, Dott had expanded across France, Belgium, and Germany, and added bike-sharing to its portfolio. That same year came a win that would define the company for years, securing one of three operating licenses in Paris through a highly competitive city tender. Paris, one of the most important regulated micromobility markets in Europe, gave Dott both legitimacy and a stable base it could build around.

Scaling Up

In April 2021, Dott raised a €71m Series B led by Sofina. Trips more than doubled that year compared to 2020. By the end of 2021, the company had added 10k e-bikes alongside its fleet of 40k+ e-scooters.

Early 2022 brought another €62m extension to the Series B, led by a new investor abrdn alongside Sofina, bringing the total raised to roughly €133m. At that point, Dott operated across 36 cities in 9 European countries.

The story through this period looked like any other growth-stage micromobility company - raise capital, expand fleet, enter new markets, lose money, repeat. But underneath the surface, Dott was building toward regulated markets, cities that ran formal tenders and expected operators to commit to long-term partnerships rather than just show up and hope for the best.

“We already had ‘disciplined growth’ in our DNA. We were not really in a ‘growth-at-all-costs’ mindset.” - Maxim Romain

The Merger

By early 2024, Dott was operating around 50k scooters and bikes across roughly 50 cities in Europe and the Middle East. That was about to change dramatically.

On January 10, 2024, Dott and TIER announced a preliminary agreement to merge.

TIER was built very differently, founded in 2018 in Berlin by Lawrence Leuschner, Matthias Laug, and Julian Blessin; it had scaled aggressively to 400+ cities across 21 countries. It was the opposite of disciplined growth. But it had reach, and it had markets Dott didn’t. The merger closed in March 2024, backed by existing shareholders from both companies led by Mubadala Capital and Sofina, with a €60m equity injection. The combined entity had revenues of €250m and supported over 125m trips a year across more than 20 countries.

The next question was what to do with two brands, two technology stacks, and two operating models competing in the same cities.

“We had to merge two operating models into one: Dott’s ‘in-house only’ model with TIER’s ‘mix of in-house and third-party operating partners.’ Taking the advantages of both models, and implementing it in a very pragmatic way.” - Maxim Romain

On the brand and tech question, the decision was deliberate. After an internal audit, the team chose to keep the Dott technology stack and migrate everything, vehicles, brand, users, to Dott. It was tested in a few cities first, then rolled out across more than 300 cities in under a year, from May 2024 to March 2025. On October 1, 2024, the combined company officially became Dott. All TIER vehicles were rebranded, all TIER users redirected to the Dott app, and what had been two companies became one, with access to a fleet of 250k electric scooters and e-bikes across 427 cities.

The Painful Middle

The merger created something valuable, but it also created significant disruption. FY2025, the first full year of operating as a single entity, showed both sides of that.

Net revenue fell 16% YoY to €173.3m. Total rides dropped 13% to 76.9m.

But those numbers need context.

Two things drove the decline. First, Dott deliberately exited a number of unprofitable markets - Slovakia, Qatar, and Sweden, among others. These exits removed fleet and rides from the count, but they also removed costs and losses. Estimated revenue impact from exits: approximately €8m of the YoY decline.

Second, the migration from the TIER app to the Dott app caused a one-off drop in active users, particularly in regions that had been primarily TIER territory - Germany, Austria, Switzerland, Central and Eastern Europe, and the Nordics.

“2025 was a transformational year for Dott. With the migration, we simplified the organisation, cut costs significantly, and built a leaner, more scalable platform.” - Maxim Romain

By the second half of 2025, user numbers had stabilized. Markets less affected by the migration, France, Belgium, the Middle East, performed well throughout the year. Overall fleet utilization held steady at 1.30 rides per available vehicle per day across FY2025. More importantly, the underlying economics started improving. Rides per available vehicle (RpAV) were 6% higher in Q4 2025 compared to the prior year. Net revenue per vehicle per day (NRVD) rose 5% in Q4 to €2.73. The shift of roughly two-thirds of markets to a revenue-share operating model reduced seasonal exposure and gave Dott more flexibility to scale up and down efficiently.

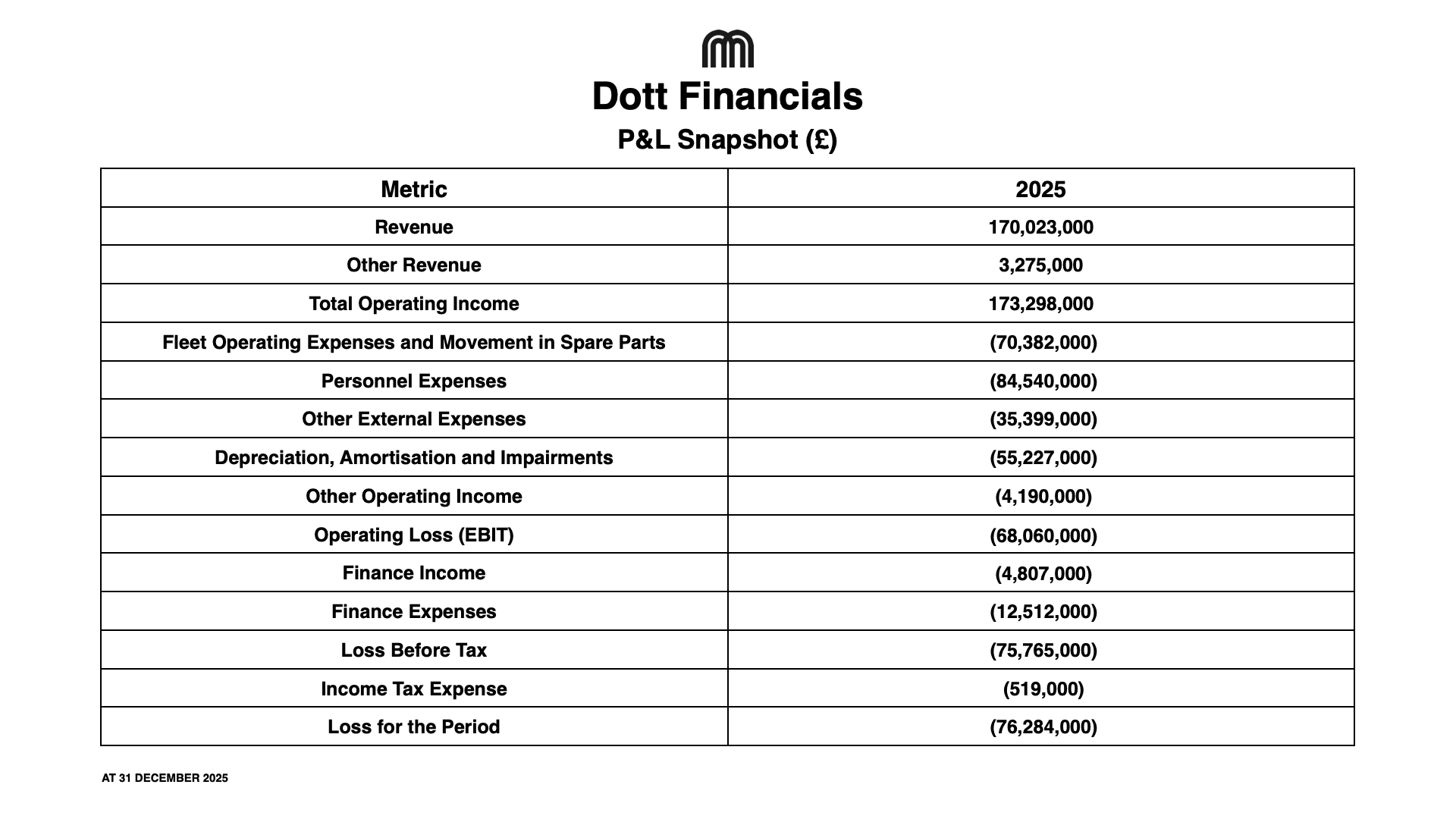

2025 Financials

Revenue declined 16% YoY to €173.3m, reflecting planned market exits and the one-off impact of the TIER user migration.

The headline for 2025 is the €7.2m Adjusted EBITDA. But the more telling number might be the Direct Market Contribution (DMC) margin: 27% for the full year, representing €47.1m. DMC is the money left over after all the costs of actually running the vehicles on the street, charging, repair, warehouse, city fees, insurance, payments. It’s the clearest measure of whether the underlying business works before you account for central overhead. At 27%, Dott’s street-level economics are solid.

The work on headquarters costs was equally significant. HQ costs fell to €39.8m in FY2025, driven by a bottom-up review of the cost base, the relocation of approximately 20% of HQ roles to a shared service centre in Wroclaw, and renegotiated supplier agreements. That cost discipline, together with the resilient DMC, closed the gap that had kept Dott unprofitable for 6 years.

Exceptional items of €10.4m in 2025 (primarily restructuring costs) meant EBITDA was still negative at -€3.2m. Adjusted EBITDA strips those out, and the €7.2m reflects the operating reality of the business going forward.

At the operating level, EBIT remained deeply negative at -€68.1m, largely due to €55.2m in depreciation and amortisation on the fleet. This is typical for asset-heavy micromobility businesses, where vehicles are depreciated over time even as underlying performance improves.

In Q4 specifically, historically the hardest quarter given winter conditions across Europe, Dott delivered €0.5m in Adjusted EBITDA.

For a company in a deeply seasonal business, a profitable Q4 is a meaningful signal.

“Q4 2025 was a strong finish to the year as the impact of this work started to show in our results.” - Maxim Romain

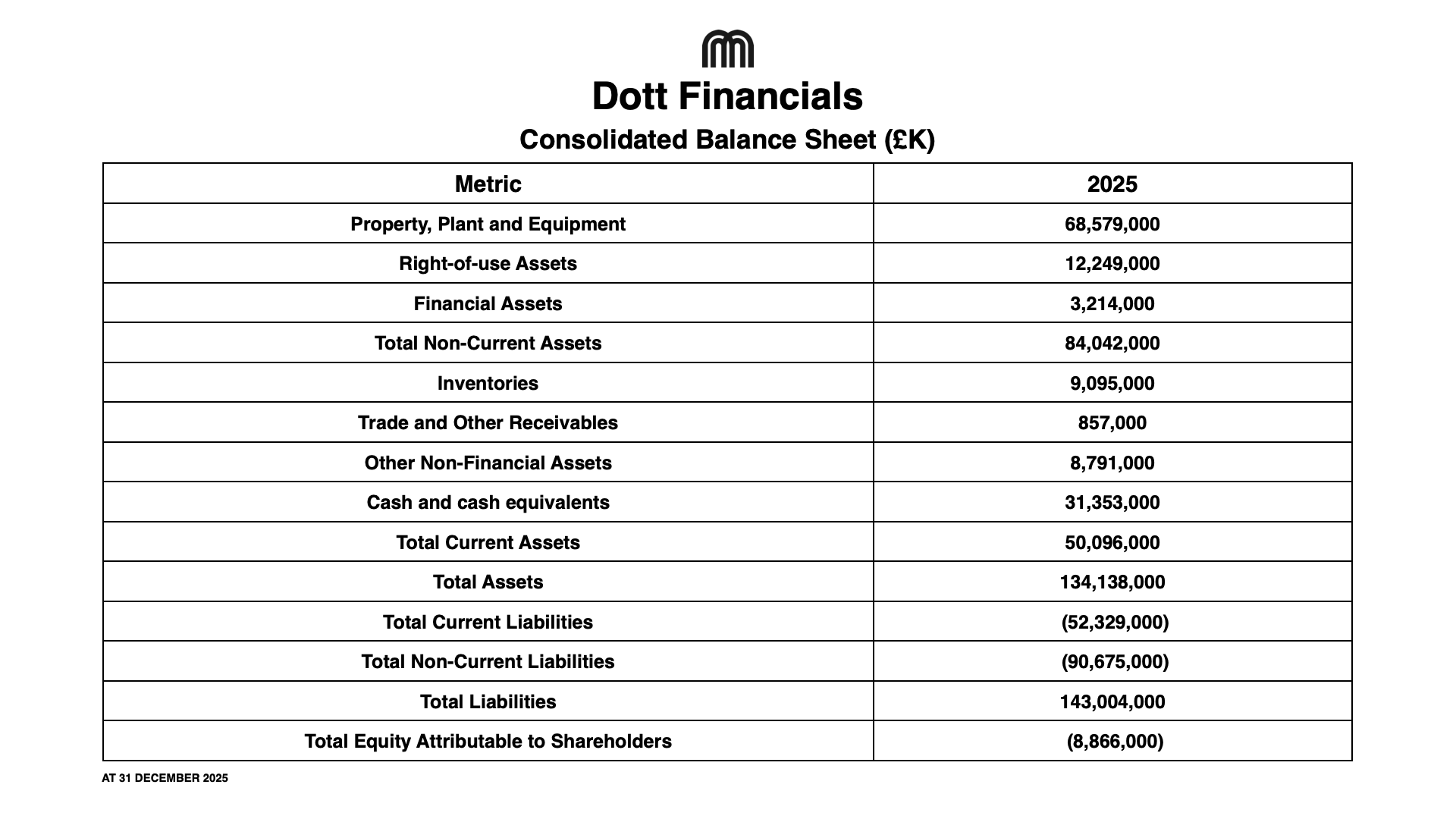

Cash Position, Debt, & Fleet

Dott ended FY2025 with €31.4m in cash against Net Interest Bearing Debt of €53.4m. The company recorded an operating cash outflow of -€20.4m, which reflects a transition year driven by restructuring costs, user migration disruption, and upfront investments into the fleet.

To fund the next chapter and clean up the balance sheet, Dott raised €85m in Q4 2025, €70m through a Nordic bond and €15m through a Series D extension. The bond carries a floating rate of 3-month EURIBOR plus 8% and matures in October 2029. Proceeds were used partly to repay approximately €42.5m in existing asset-backed debt, cleaning up the balance sheet considerably. In March 2026, Dott received the full €15m in Series D Extension subscriptions and secured an additional €10m Super Senior Revolving Credit Facility with Rabobank, a working capital line that completes the capital structure without adding long-term debt.

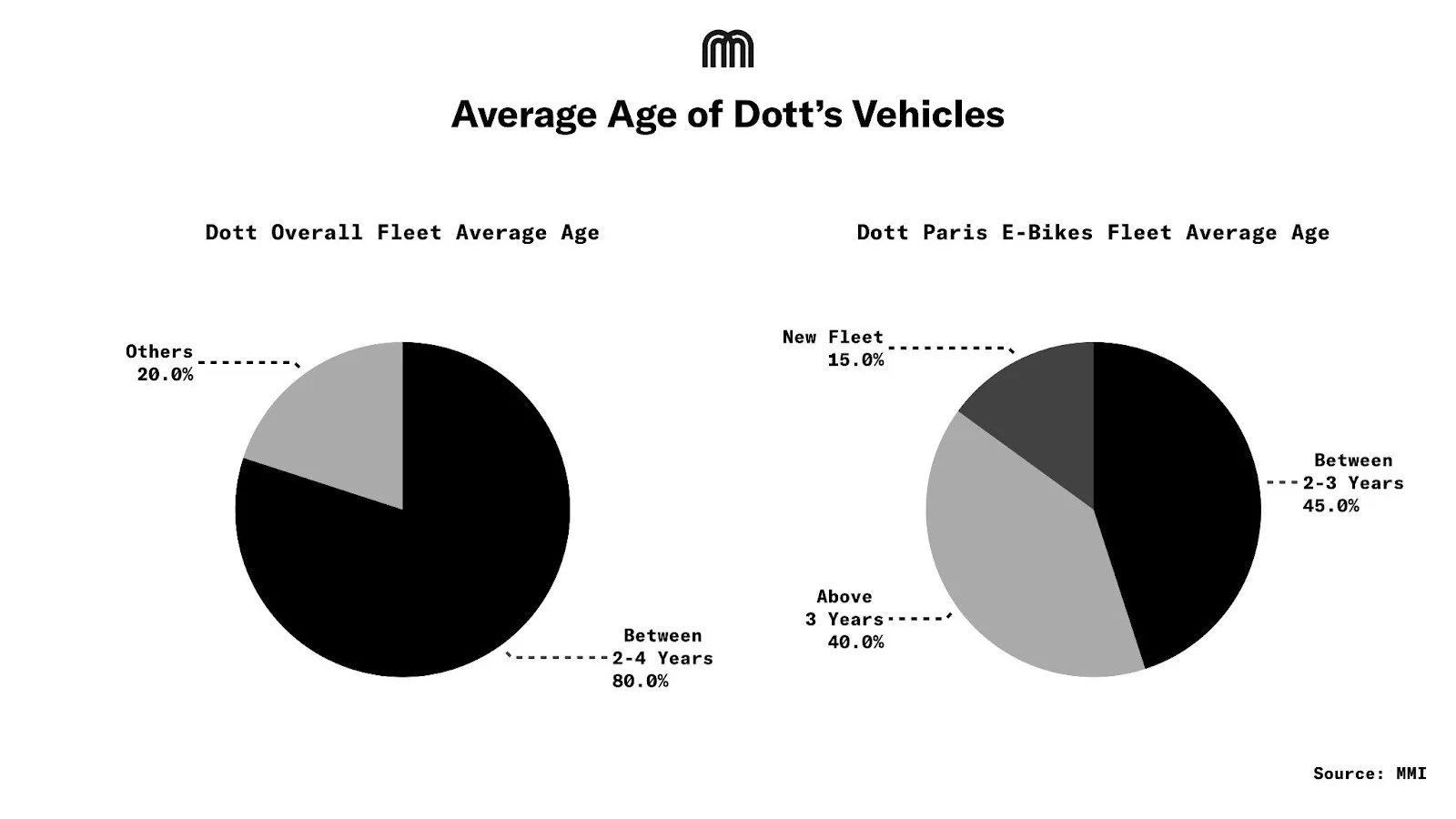

The funding is financing a major fleet refresh: 45k new vehicles, 13k e-bikes and 32k e-scooters, ordered and on track for deployment in Q2 2026. The new hardware will be depreciated over 8 years, reflecting the longer durability of the latest vehicle generation. Paris gave a preview of what the new fleet can do. When Dott launched its newest e-bike model under the new Paris tender in October 2025, utilization went up even though the deployed fleet was smaller than before. Higher utilization on fewer vehicles is exactly the economic outcome the company has been building toward.

Dott also says that over 80% of its fleet is between 2 and 4 years old. In Paris, the picture is similar, only 15% of the e-bike fleet is new, with most vehicles already in the 2-3 year range.

Dott vs. Voi: Two Paths to the Same Milestone

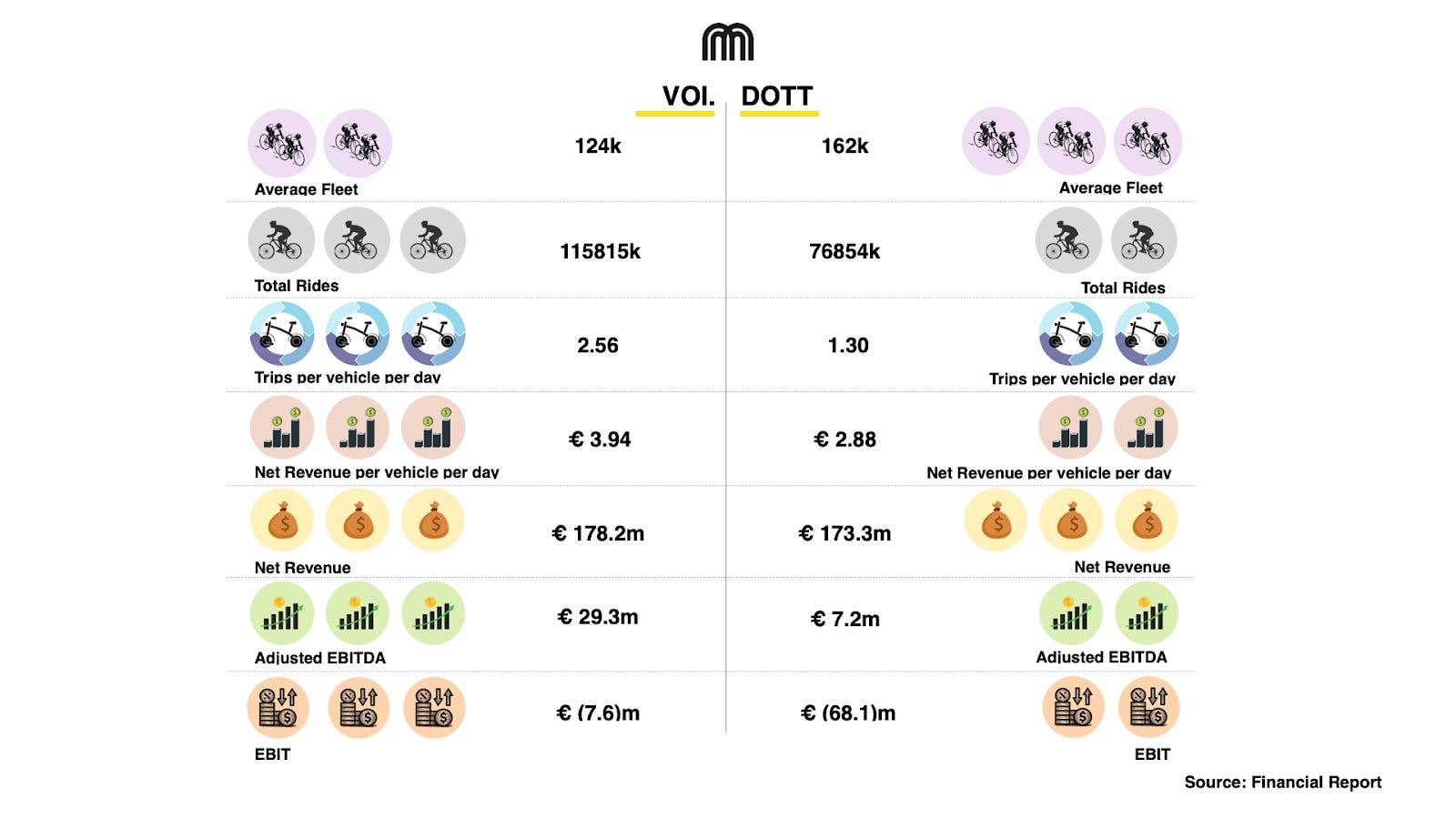

Dott wasn’t the only European operator to cross into profitability in 2025. Voi, the Swedish micromobility company, did too, and putting the two side by side is genuinely useful, not because one is winning and one is losing, but because they took almost opposite routes to get to the same place. It says something about what paths actually exist in this industry.

Dott deliberately shrank. It exited markets, shed revenue, and absorbed the disruption of a full user migration, all in service of building a leaner, more profitable base. Voi did the opposite. Voi, grew its way to profitability. Net revenue rose 34% YoY to €178.2m. Fleet expanded 34% to an average of 124k deployed vehicles. Rides jumped 55% to 116m. Adjusted EBITDA came in at €29.3m with a 16.4% margin.

Voi’s vehicle economics are stronger on almost every per-unit metric. Trips per vehicle per day at 2.56 versus Dott’s 1.30. Revenue per vehicle per day at €3.94 versus €2.88. But the comparison needs context.

Dott’s average fleet of 162k vehicles is actually larger than Voi’s 124k, partly because Dott’s post-merger portfolio still includes markets at different stages of optimization.

Voi’s growth in 2025 came from both new market launches and continued scaling in existing cities. This included a 6k e-bike launch in Paris, expansion across London, and strengthening its position in capitals like Berlin and Stockholm.

On cash, Voi finished the year with €56.1m against Dott’s €31.4m. Voi’s operating cash flow of €24.2m for the year reflects a business generating real cash. Dott’s operating cash outflow of -€20.4m reflects a transition year - restructuring costs, user migration disruption, and the upfront investment in the fleet refresh.

The more interesting question is 2026. Voi is investing aggressively, €63.5m in tangible assets in FY2025, primarily fleet. Dott has ordered 45k new vehicles for Q2 deployment and is targeting €30-40m in Adjusted EBITDA for the full year. If Dott hits that range, it would represent roughly 5x growth in Adjusted EBITDA in a single year, driven by cost reductions annualizing fully and a refreshed fleet operating in its strongest markets.

Voi’s profitability in 2025 was driven by a combination of revenue growth and improving unit economics. Dott is still coming out of a merger and restructuring phase, with profitability emerging as those changes begin to settle. The paths are different, but both point to a maturing industry.

Where Dott Goes From Here

7 years of building, one merger, hundreds of millions raised, a painful user migration, deliberate market exits, a restructuring, and then €7.2m in Adjusted EBITDA.

For an industry that spent most of its existence being told profitability was impossible at scale, that number matters more than its size suggests. It proves the model works. It gives Dott the credibility to raise capital on better terms, win tenders against competitors, and invest in the fleet refresh with real confidence that the economics will hold.

On leadership, January 2026 brought a change that signals intent: Maxim Romain moved from COO to CEO, with Henri Moissinac transitioning to Executive Chairman. Maxim, who co-founded the company and has run operations throughout its history, taking the top seat points toward a focus on execution rather than fundraising or strategy.

“For now, we’re 200% focused on existing cities and the deployment of our new e-bikes and new e-scooters. To keep delivering on three core promises for riders and cities: availability of vehicles, reliability of the service, and close collaboration with cities. On top of this, we will look at expanding in a few selected new markets as per tender results. We strongly believe we have the right platform to deliver a strong year ahead.” - Maxim Romain

Got your micromobility moment to share? Email us at press@micromobility.io

Loving the vibe? Hop on and ride with us! Subscribe!

Twitter | YouTube | LinkedIn | Instagram | Blog | Podcast

Cover image credit: Dott

%20(1)%201.avif)

.png)