.svg)

%2Bcopy.avif)

.svg)

.jpg)

%20(1).jpeg)

.jpg)

.webp)

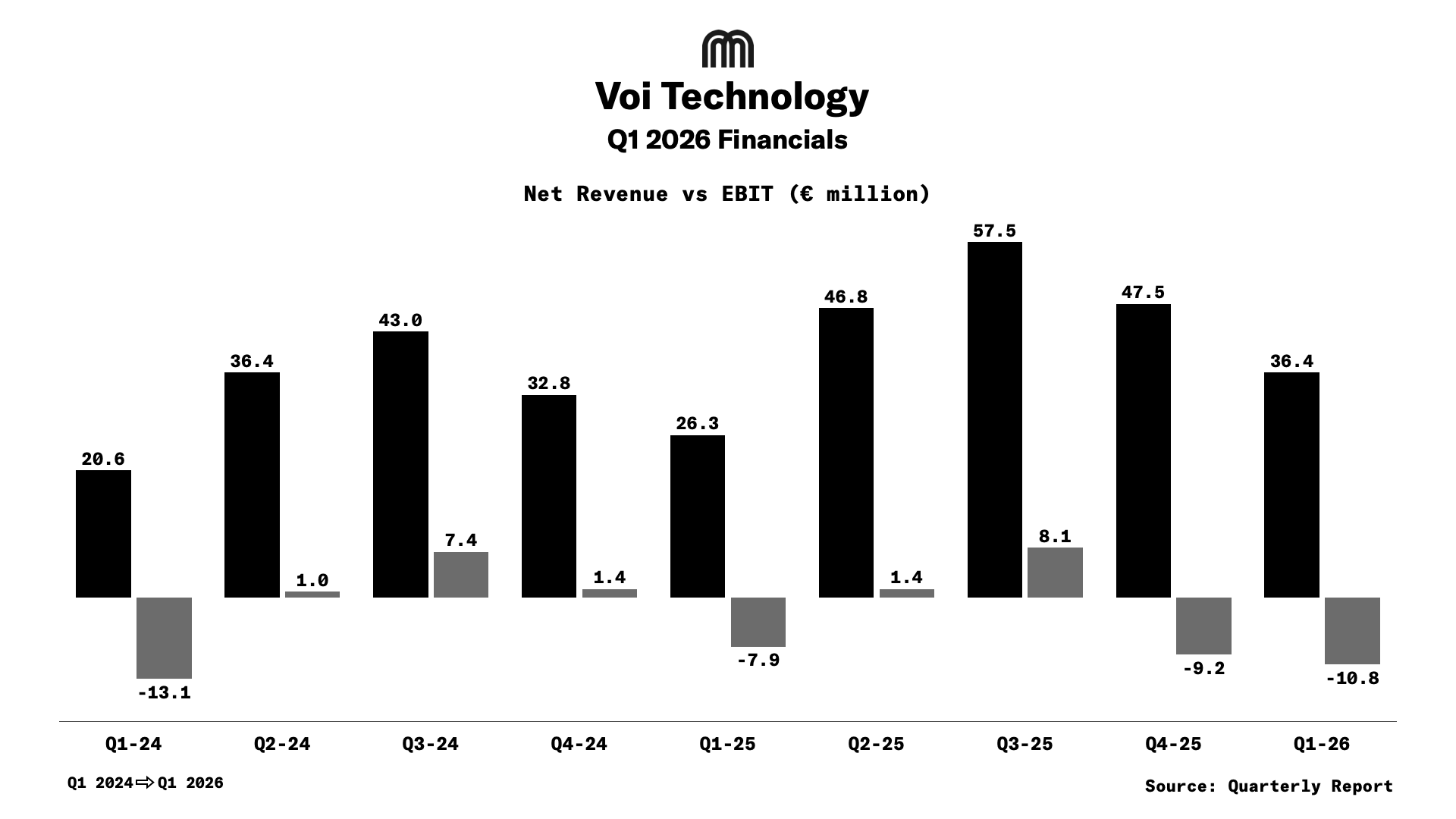

Voi Technology closed the first quarter of 2026 with net revenue of €36.4m, up 38% from €26.3m in Q1 2025. The growth came despite what the company described as the coldest winter season it has faced since launching operations across Europe.

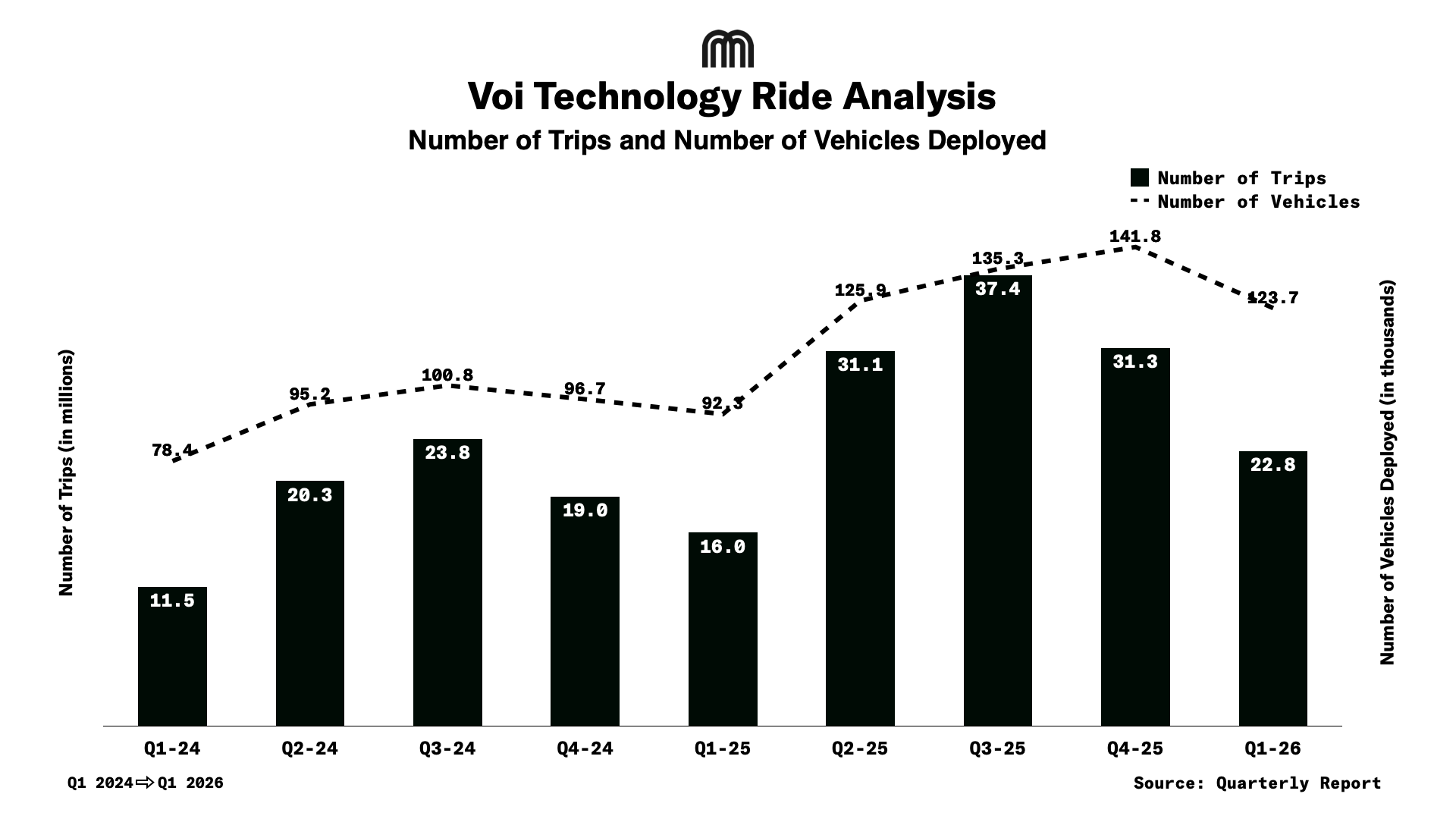

The quarter is seasonally the weakest for Voi, demand for shared micromobility drops sharply in winter, which makes the revenue record more notable. Monthly active riders grew 35% YoY, and total rides reached 22.8m, up from 16m in Q1 2025.

Fleet expansion drove the numbers

The primary force behind the revenue jump was fleet size. Active Vehicles grew 42% YoY to 123.7k units.

Worth noting: this quarter, Voi also changed how it defines and counts its vehicle fleet. The old metric, called Deployed Vehicles, counted how many days a vehicle was available. The new definition, Active Vehicles measures availability within the day itself, making it a more precise reflection of the fleet actually accessible to riders at any given time. Comparative figures have been restated under the new definition.

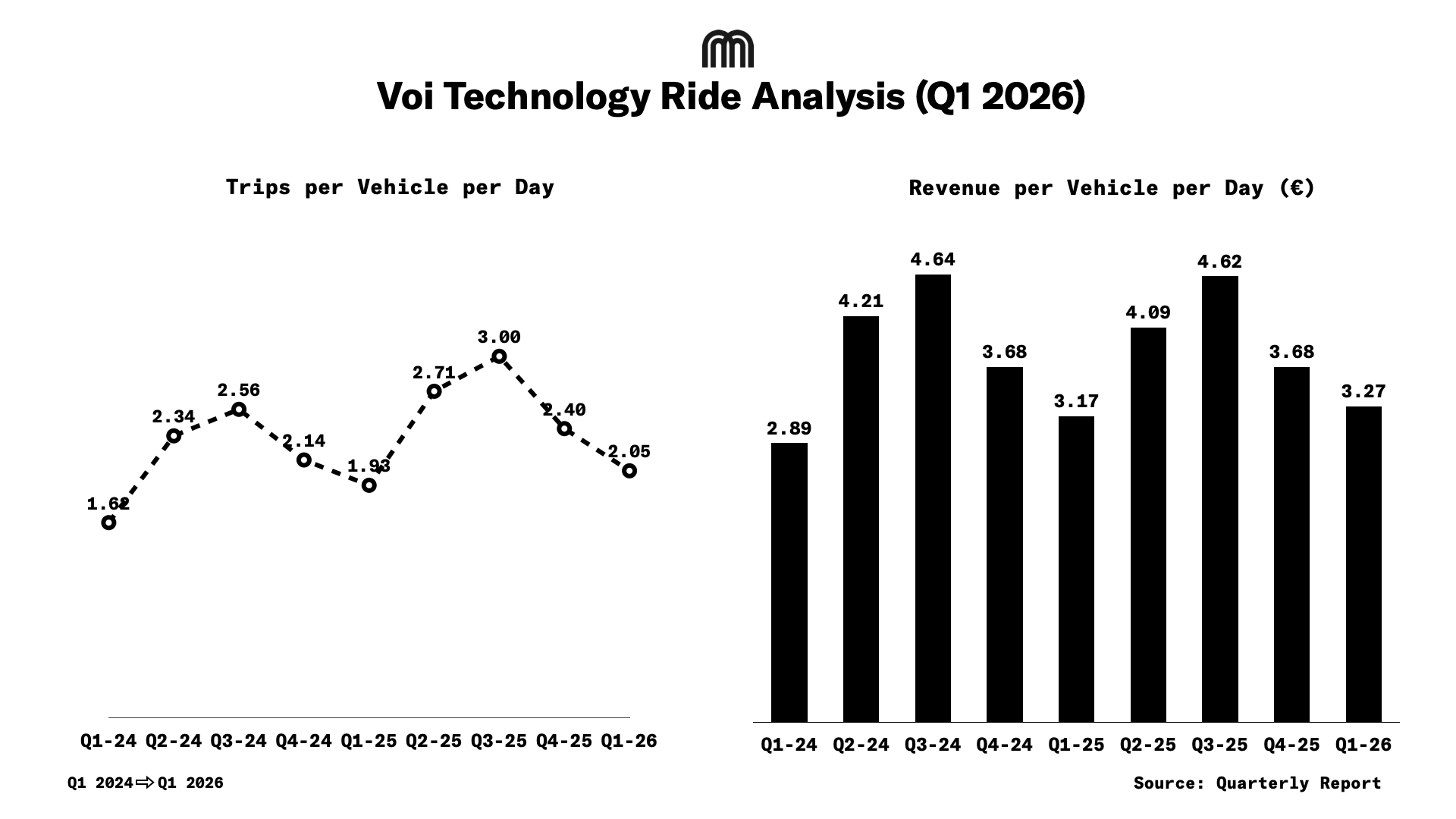

That expansion, however, also diluted per-vehicle metrics: Net Revenue per Vehicle and Day fell 2.8% to €3.27 from €3.36 as the enlarged fleet was deployed into markets still affected by harsh weather in January and February.

Fredrik Hjelm, Co-Founder and CEO, put it plainly:

"Q1 showed what Voi is made of. We grew through the toughest winter we have seen as a company, built on years of work to make our user experience better and our operations leaner. This spring, we're deploying over 50,000 new e-scooters and e-bikes across European cities, our biggest and most diverse fleet ever. We're heading into the summer season in the strongest position we've ever been in."

Margins held steady

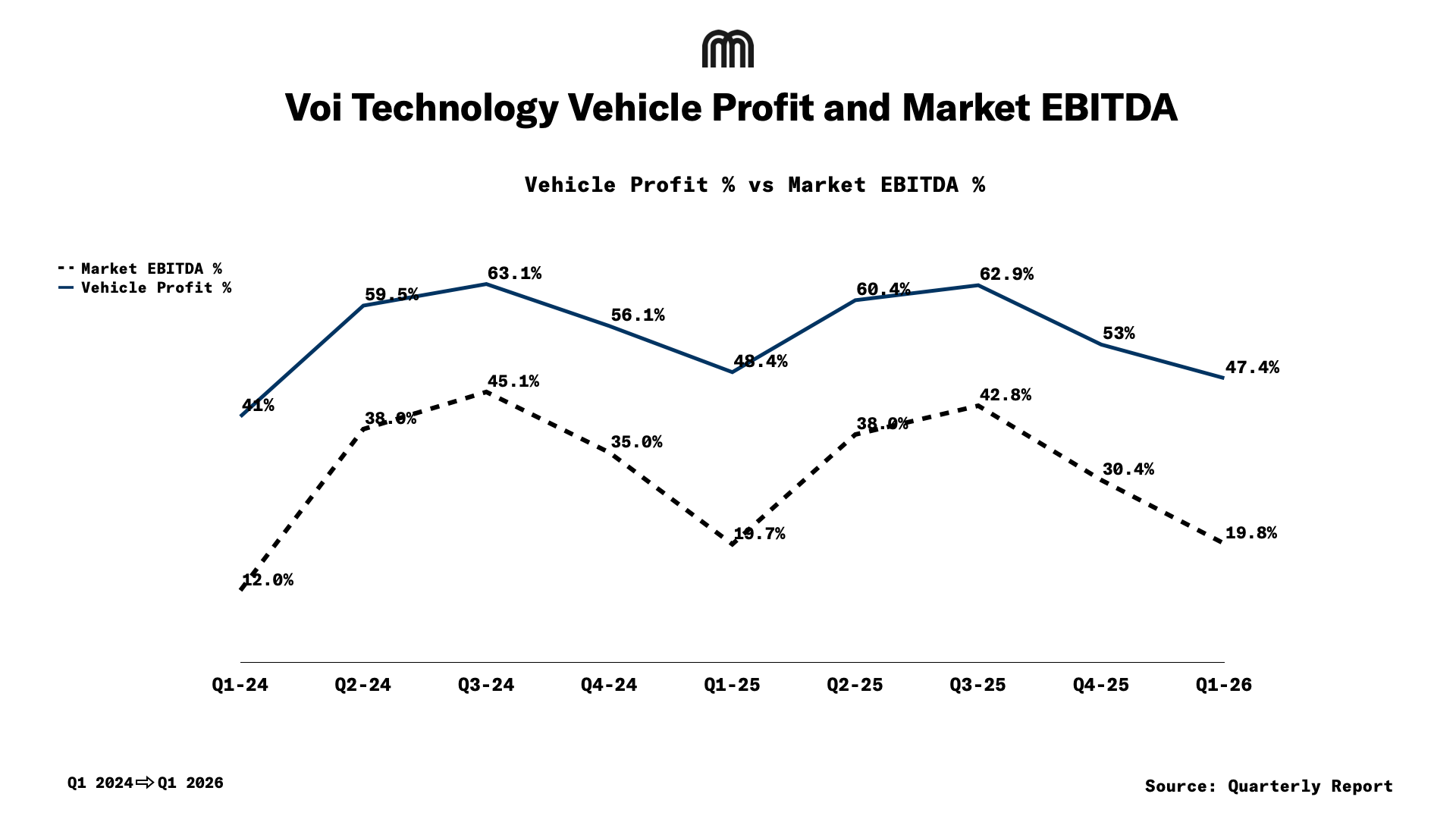

Vehicle profit, the revenue left after direct fleet and maintenance costs, rose 35% to €17.2m. The vehicle profit margin came in at 47.4%, roughly flat compared to 48.4% in Q1 2025, which the company attributed to continued investment in expansion markets and the cold start to the year.

Market EBITDA, which layers in city-level costs like insurance, marketing, and local staff, grew 39% to €7.2m, with a stable margin of 19.8% versus 19.7% a year ago.

Adjusted EBITDA improved by €0.4m to -€1.8m, with the margin tightening from -8.3% to -5.0%. On a last-twelve-months basis, Adjusted EBITDA reached €29.7m.

Mathias Hermansson, CFO and Deputy CEO, commented:

"We have continued to execute on the plan we set out, and our first quarter reflects the continued strong demand for our service as well as the investments we are making to set us up for the rest of the year. We reported both all-time high revenues and Adjusted EBITDA in a first quarter and continued to grow our last-twelve-months Adjusted EBITDA to EUR 30m. Our strong unit economics and solid financial position allow us to keep investing in long-term value creation, while remaining fully committed to profitable growth."

Where losses widened

Adjusted EBIT fell to -€8.9m from -€7.2m a year ago, driven by a 43% increase in depreciation charges, from €5.0m to €7.1m, which mirrors the 42% growth in average fleet size.

Notably, Voi revised the estimated useful life of vehicles acquired in 2024 or later to 10 years, up from a previous estimate of 5-7 years. The company attributed this to improvements enabled by its refurbishment centre in Poznań, Poland, launched in Q4 2025, as well as strong real-world performance of its fleet, with its oldest vehicles now entering their seventh year of operation. The change extends the depreciation period for newer vehicles, affecting how costs are distributed over time.

EBIT fell to -€10.8m from -€7.9m. Net financial items swung sharply negative, to -€4.1m from a positive €1.4m in Q1 2025. Bond interest costs rose to €2.1m, up from €0.3m, following the October 2025 bond tap that raised the outstanding bond to €90m. Currency movements, particularly EUR/SEK and USD/SEK, added further pressure of €1.9m combined.

The net loss for the period was €15.1m versus €6.9m in Q1 2025.

Cash and balance sheet

Cash and cash equivalents ended the quarter at €29.3m, down from €56.1m at the start of the year. The €26.8m draw-down reflects vehicle purchases ahead of the spring deployment. Cash flow from investing activities was -€14.7m for the quarter.

Net Interest Bearing Debt rose to €71.4m from €44.6m at year-end 2025, an increase of €26.8m. The €25m revolving credit facility remains undrawn.

Total equity declined to €10.8m from €24.7m at the end of 2025, driven by the quarterly net loss of €15.1m, partially offset by €1.0m in share-based payments.

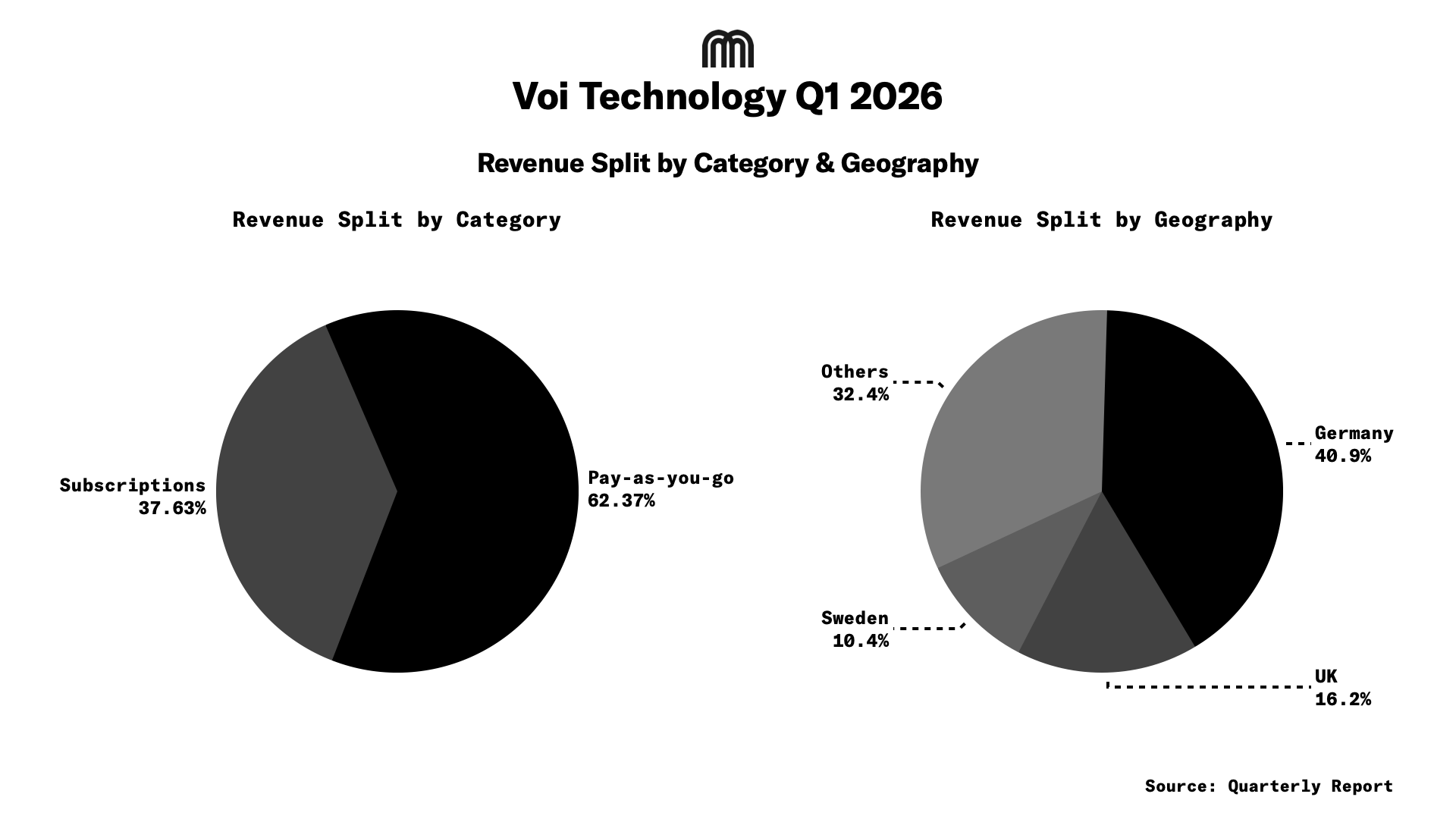

Revenue breakdown: Geography and Product

Of the €36.4m in net revenue, €22.7m came from pay-as-you-go rides, where a customer unlocks a vehicle, pays an unlock fee plus a per-minute charge, and the transaction settles immediately. The remaining €13.6m came from subscriptions, Voi's daily and monthly passes known as Voi Pass, where revenue is recognised across the subscription period. Both streams grew YoY, up from €17.1m and €9.2m respectively in Q1 2025, reflecting the larger rider base and increased subscription uptake.

Geographically, Germany remained the largest market at €14.9m, followed by the UK at €5.9m and Sweden at €3.8m. The rest of the markets combined contributed €11.8m, nearly double the €6.4m they generated in Q1 2025, driven by expansion into southern Europe where milder weather conditions supported stronger demand through the winter. France stood out within that group, growing 260% YoY to become Voi's third largest country by revenue in Q1.

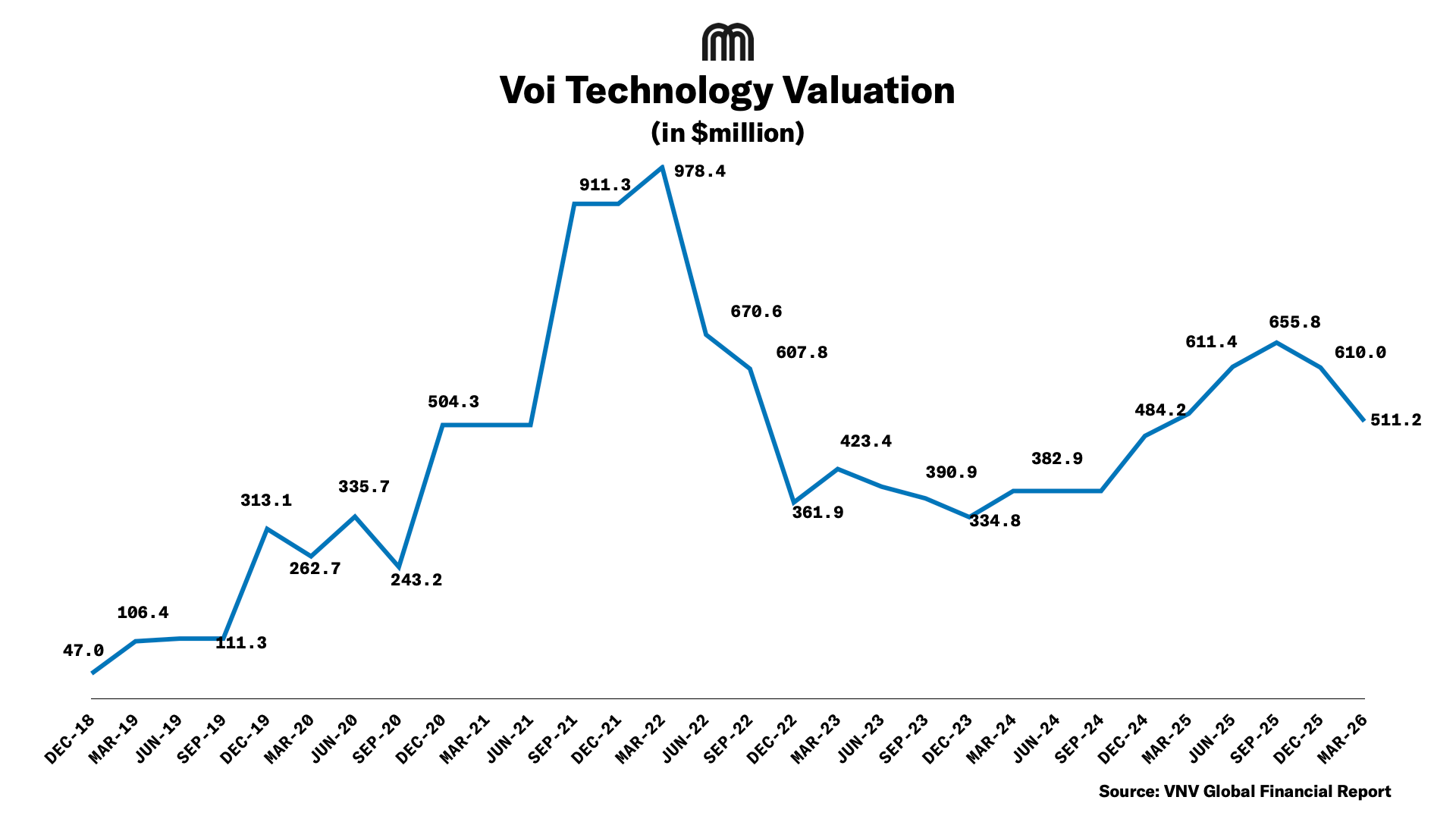

Valuation Update

VNV Global marked Voi’s valuation at $511.2m by the end of March 2026, declining from $610.0m at the end of 2025 and $655.8m in mid-2025, while remaining above its $484.2m end-2024 level.

Strategic highlights

In London, Voi now operates across 10 boroughs covering a combined population of 2.7m. Paris has reached top-five status among Voi cities by both revenue and utilisation. During the quarter, Voi also entered the Netherlands, its 13th country, with e-bike operations.

This is the first year Voi plans to deploy more e-bikes than e-scooters as part of its stated strategy to build a multi-modal platform.

Cover image credits: Voi