.svg)

%2Bcopy.avif)

.svg)

.webp)

.webp)

Shared bike and scooter services in Italy have firmly established themselves in people’s daily mobility habits, despite a reduction in vehicle fleets and operators since 2023. The sector has entered a consolidation phase, moving from rapid expansion to stable, mature usage. While free-floating carsharing declines sharply, bike and scooter sharing maintain steady demand, concentrated in larger cities.

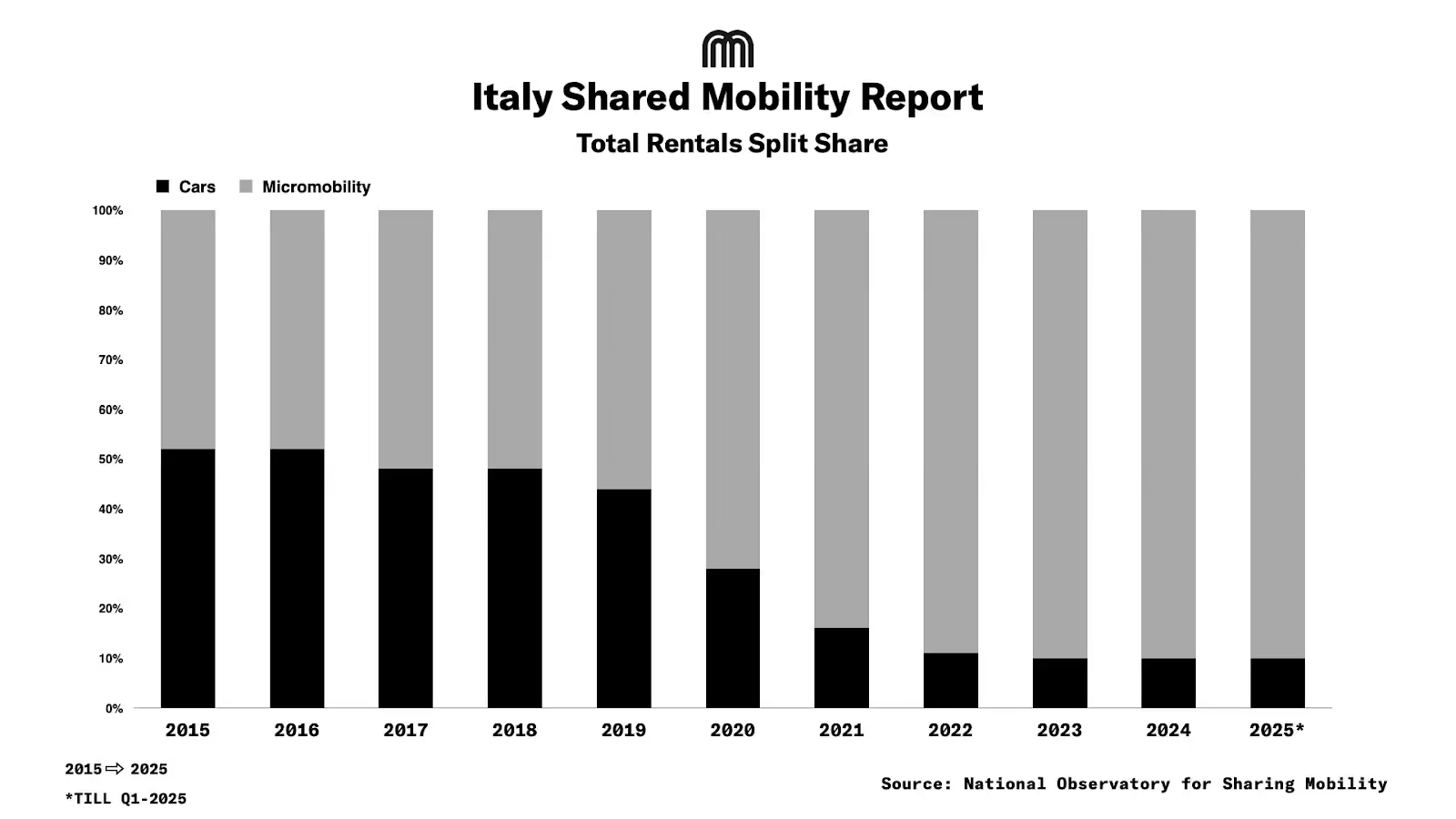

As of 2025, Shared Micromobility accounts for 90% of the mobility rentals in the country.

Total Mobility Rentals

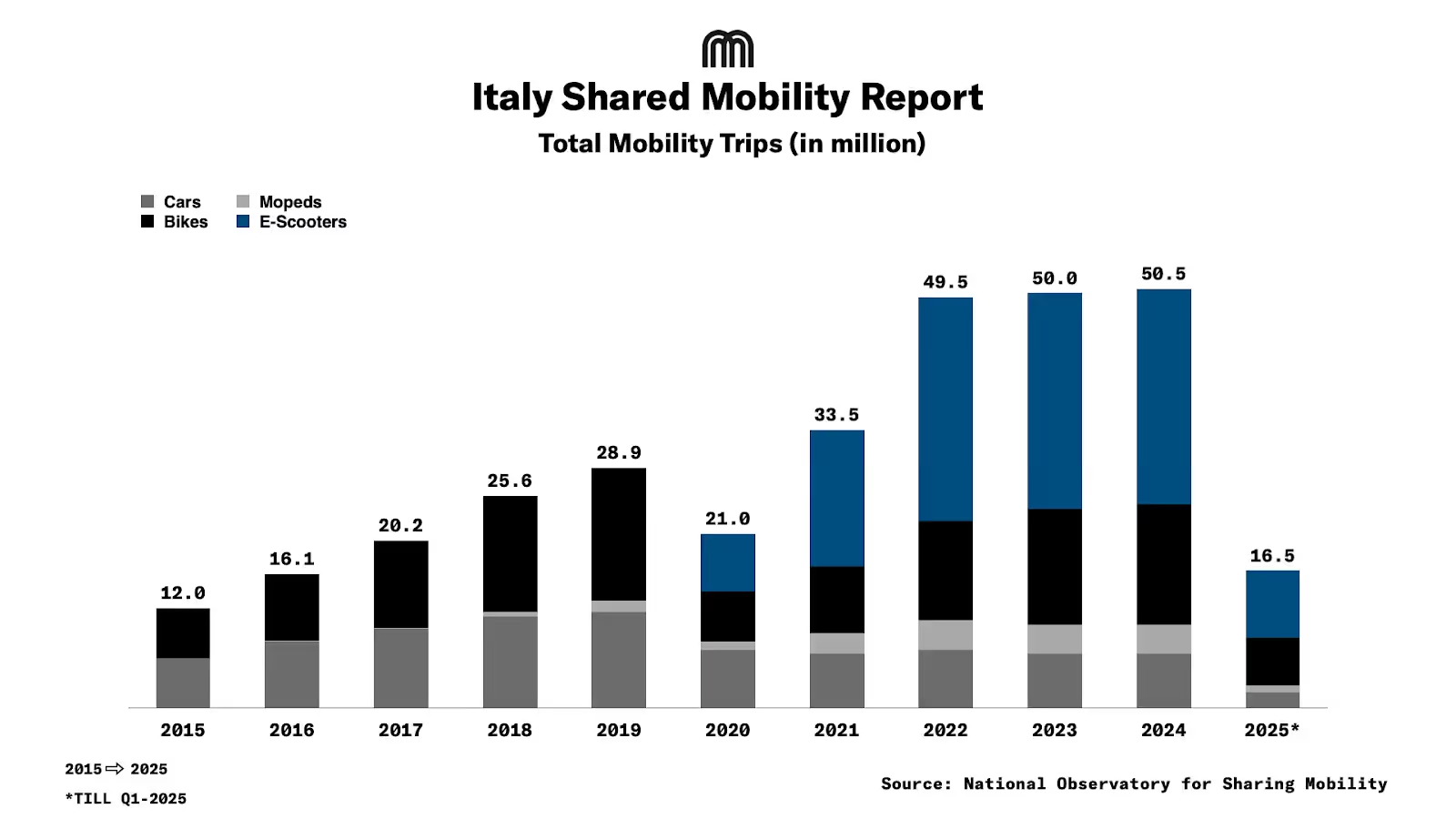

By 2025, Italy’s shared mobility sector is expected to reach nearly 60m rentals, marking a 20% rise from 2024. Within this, e-scooter sharing leads the market, representing 50% of total rentals, while bike sharing continues to grow, now accounting for 32%, up by 4% since 2022.

Total mileage is steadily increasing, projected to hit 200m kms by 2025. In 2024, the average trip distance stands at around 2 kms for shared bikes, 4.5 kms for e-scooters.

How did the Cities Fare?

Rome leads Italy’s shared mobility market with 13.2m total rentals (including car rentals), followed by Milan and Turin, while Bologna and Florence recorded the strongest growth in 2024. Milan tops the list for the highest number of vehicles available per inhabitant, ahead of Florence and Pisa.

Notably, Milan, Rome, Florence, Bergamo, and Turin remain the only cities that offer all four shared mobility services simultaneously.

Accident rates in shared mobility remain remarkably low, with an average of one accident reported every 300k kms travelled. In 2024, all vehicle types saw further improvements: accidents dropped by 7% for e-scooters, 54% for mopeds, and 67% for bicycles. Both e-scooters and mopeds maintained similar safety levels, recording 0.6 and 0.4 accidents per 100k kms, respectively.

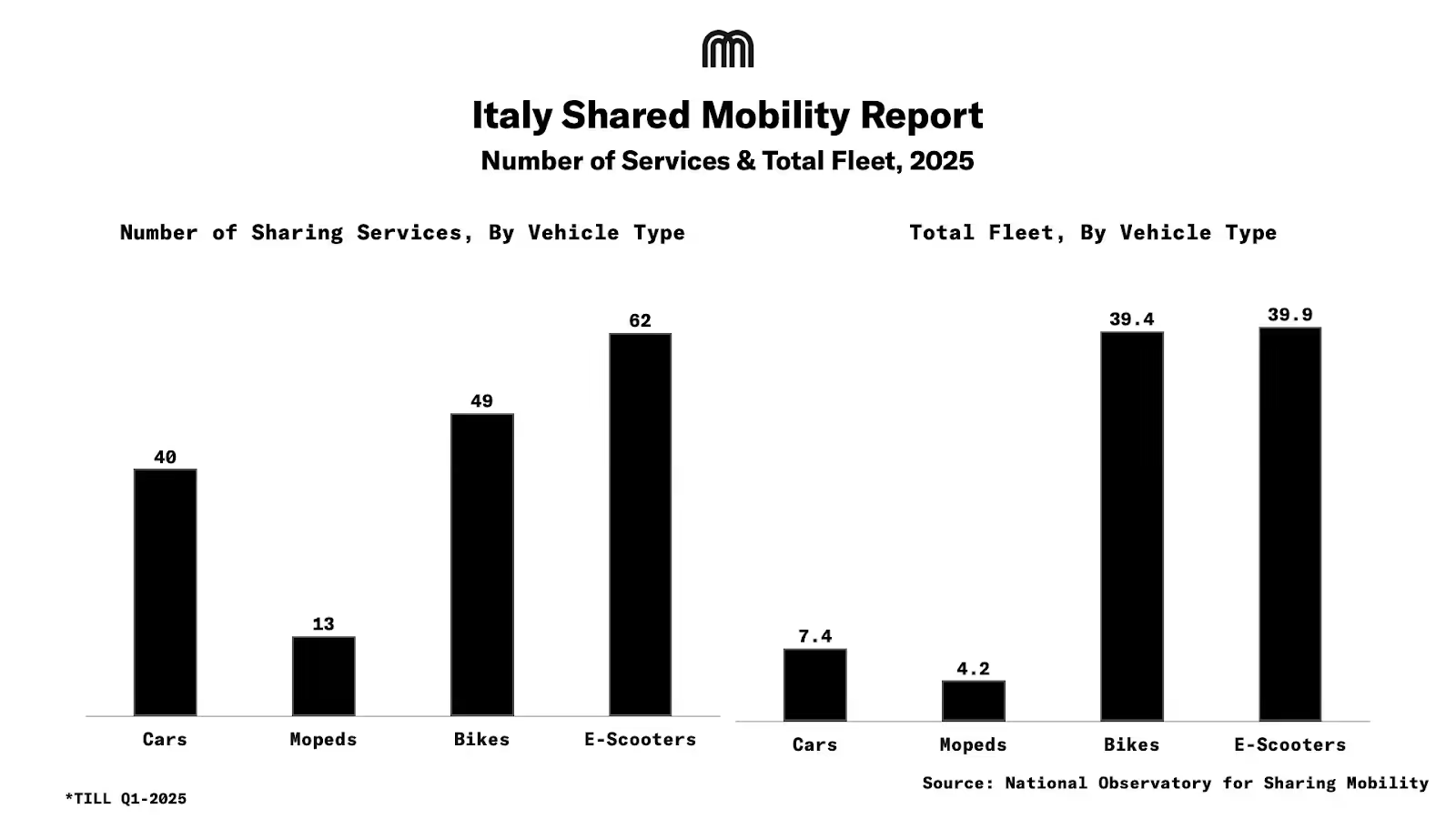

Fleet & Services

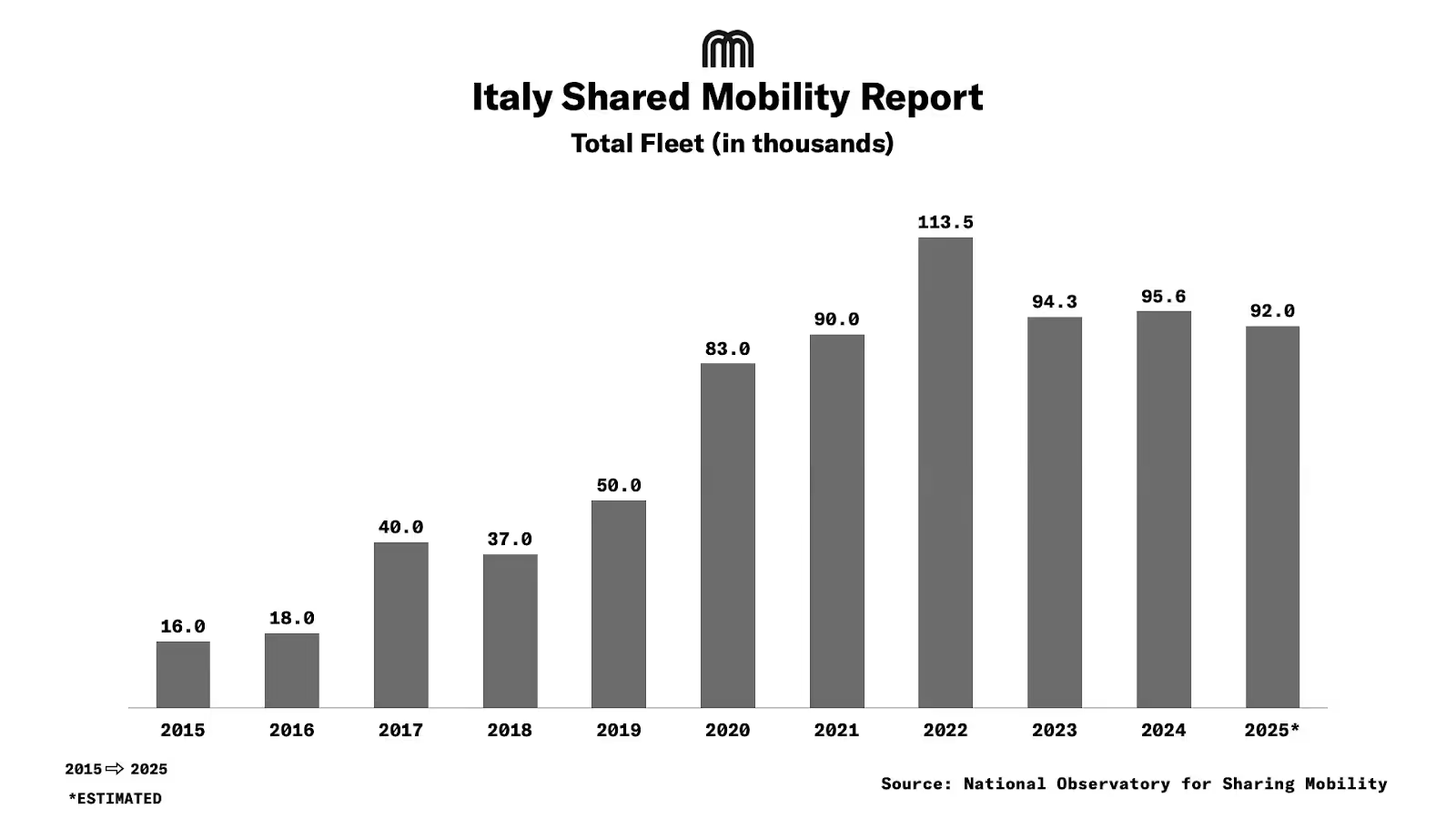

In 2024, Italy is expected to have around 95.4k shared vehicles, marking a 15% decline from 2022. Although fleets of e-scooters, carsharing, and bikesharing saw a temporary rise during 2024, projections for 2025 indicate a further reduction of over 4k vehicles. This decline is mainly driven by a 6% decrease in e-scooters and a 17% drop in shared cars.

In 2024, Italian cities had around 170 shared mobility services in operation, representing a 26% drop from 2022. By April 2025, this number declined further to 166 services, largely due to the contraction of e-scooter-sharing, which has reduced by 37 services since 2022.

Meanwhile, total number of active sharing operators will also fall, with nine fewer in 2024, bringing the total to 37.

Electrified Fleet

Italy’s shared mobility fleet remained largely electrified, though trends varied across service types. Bikes, in particular, saw a strong shift toward electric models, e-bikes accounted for 31% of the fleet, up from 26% in 2023, and returning to 2022 levels. Meanwhile, traditional bicycles declined to 11%, marking a 3% drop from 2023, and 8% drop from 2022.

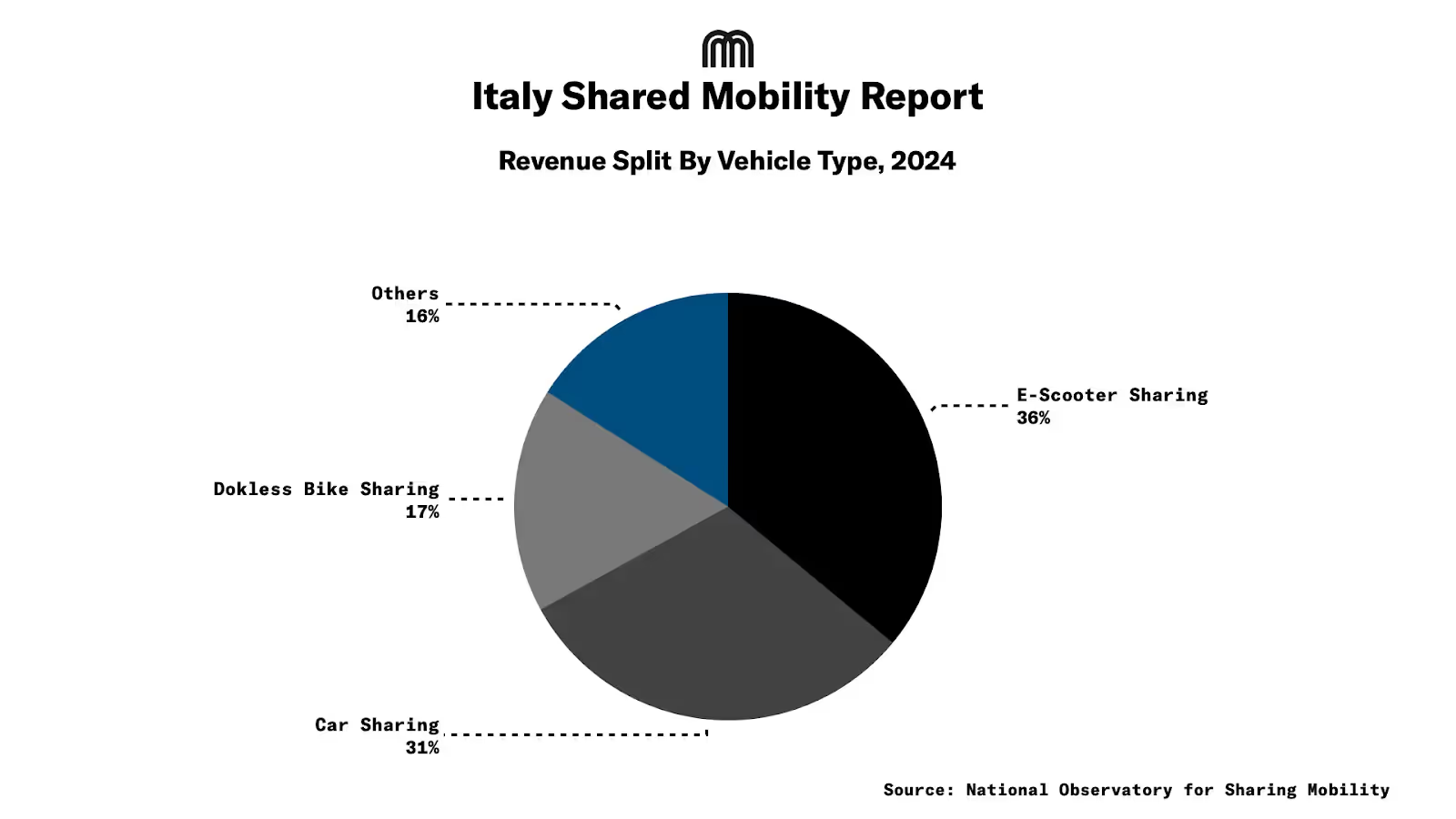

Revenue Generated from Italy Shared Mobility

In 2024, Italy’s shared mobility sector generated just over €200m in revenue, up 4% from the previous year but dropped by 11% compared to 2022. e-Scooter sharing and free-floating carsharing continued to lead the market, contributing 36% and 31% of total turnover, respectively. Free-floating bikesharing also grew, rising from 15% in 2023 to 17% in 2024.

Conclusion

Italy’s shared mobility sector has transitioned from rapid expansion to a phase of stable, mature growth. Despite smaller fleets and fewer operators, usage remains strong, with e-scooters and e-bikes leading urban travel. Major cities continue to drive adoption, supported by improving safety and increasing electrification.

With over 90% of mobility rentals now coming from shared micromobility, Italy stands as one of Europe’s most dynamic markets, helping to redefine urban movement.

Image credit/dott