.svg)

%2Bcopy.avif)

.svg)

%20(1).jpg)

.webp)

.webp)

As of 2022, India had 263m two-wheeled vehicles on the road, making it the world’s largest two-wheeler market. In terms of annual sales, India has also leapfrogged China. However, the picture changes when we look at electric vehicle penetration in the two-wheeler segment. Annual electric two-wheeler sales in the two countries present a chalk-and-cheese contrast.

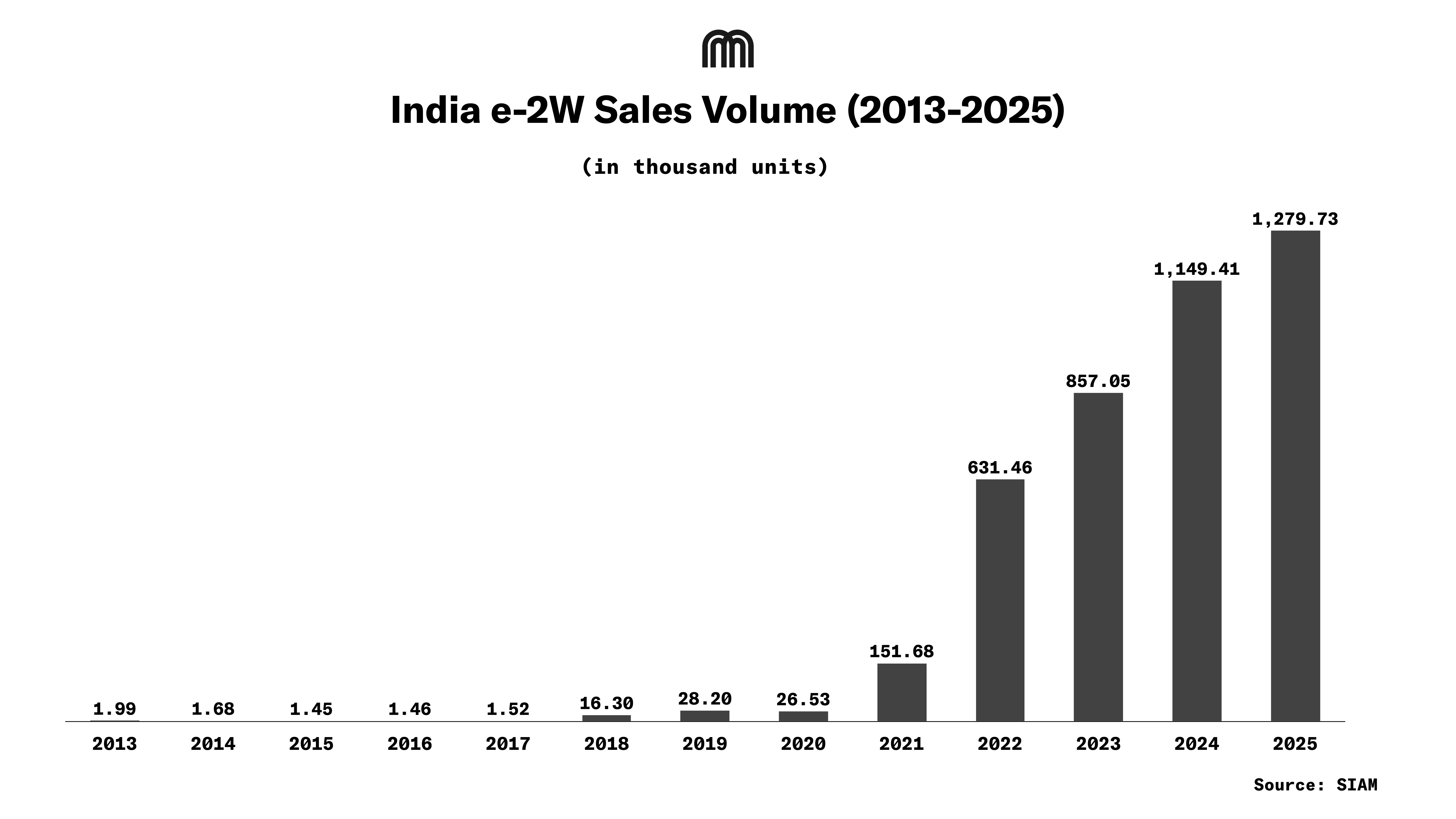

2022 - Watershed Year in India E-2W Market

India’s electric two-wheeler sales surged 305% YoY to ~632k units in 2022, driven by alignment of policy support and market forces. FAME-II subsidies, at times covered up to 40 % of ex-factory price ($150/kWh), were the single biggest catalyst, accounting for an estimated 60–70% of the growth by cutting effective scooter prices 15–20% (a $1.3k e-scooter dropping to ~$1.1k).

The impact was amplified by greater model availability from multiple OEMs and improved product features like higher range and connected tech.

Breaching One Million Sales

India’s e-2W market surpassed the one million unit mark, with around 1.15m units sold, up about 33 % YoY from ~860k in 2023. Leading OEMs like Ola Electric, TVS Motor, Bajaj Auto, and Ather Energy reported their best-ever annual e-2W sales, underpinning the segment’s momentum.

Region-wise, Maharashtra held the highest share with 18%. Growth reflected maturing supply chains, falling battery prices, and strong urban demand despite FAME subsidy uncertainty.

New Heights in 2025

In calendar year 2025, India’s e-2W segment achieved a **record retail sales tally of approximately 1.28m units, marking an 11 % YoY increase despite shifts in GST and competitive ICE pricing. Electric two-wheelers accounted for about 56 % of total electric vehicle sales (around 2.27m EVs across segments).

This growth comes against the backdrop of a much larger total two-wheeler market of 20.29m units in 2025, where e-2Ws made up roughly 6.3 % of overall sales, a slight increase over the previous year.

Competitive Landscape

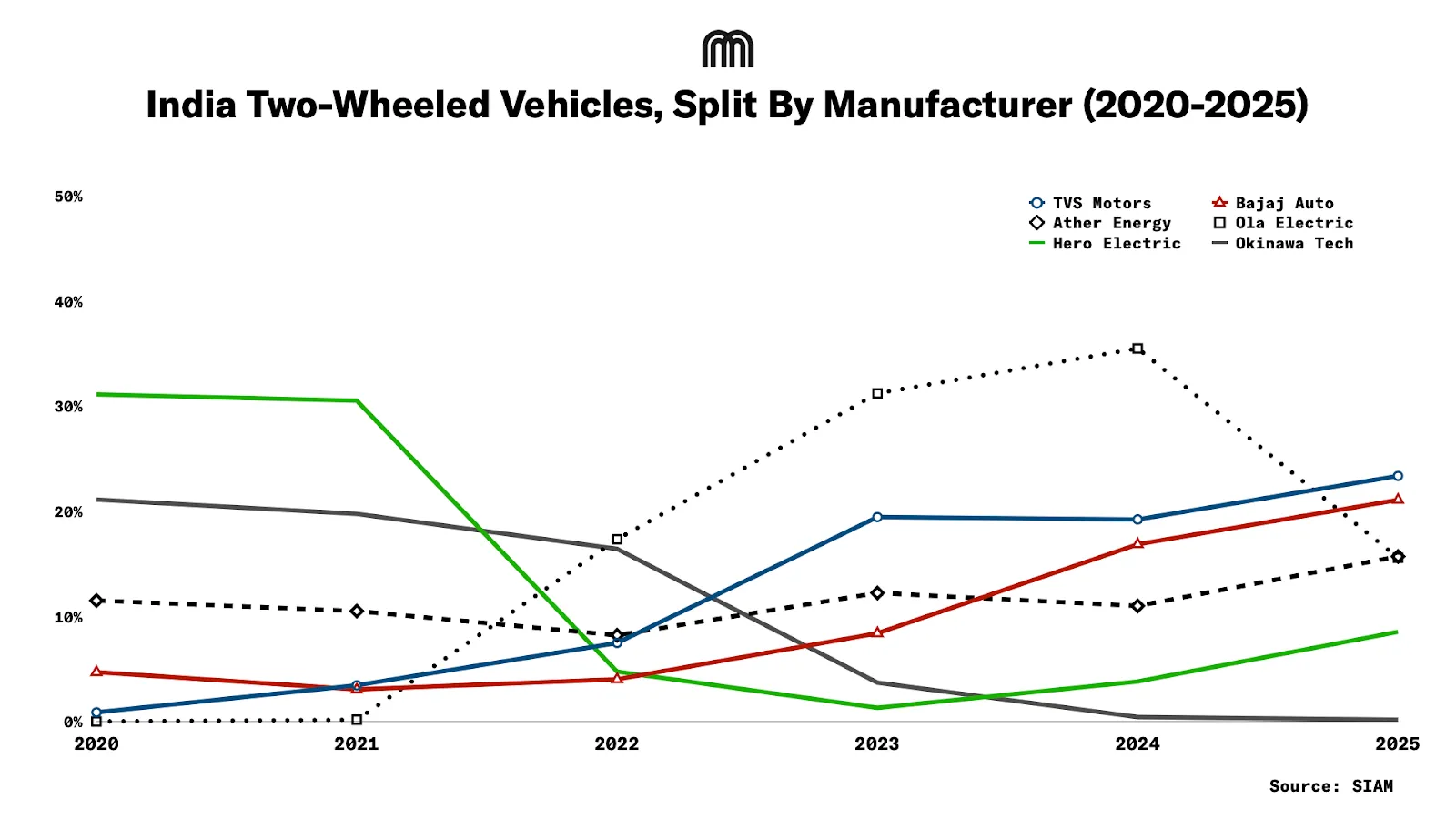

The competitive landscape has shifted too: TVS Motor Company emerged as the top seller with nearly 299k e-2Ws, surpassing Ola Electric (whose sales more than halved in 2025). Other legacy manufacturers like Bajaj Auto, Ather Energy, and Hero MotoCorp also posted record annual retail figures.

The path for current market leaders has not been a smooth ride. The Indian e-2W market in the pre-pandemic era was dominated by low-speed electric mopeds. These vehicles stood no chance against their gasoline counterparts in terms of performance. A slow shift in the market was witnessed when high-powered motor-equipped scooters like Ather 340 & 450 models went on sale in 2019, Bajaj & TVS brought their scooters in early 2020, which gained popularity.

Ola Electric Market Leader in 2022-2024 Period

Ola Electric dominated India’s electric two-wheeler market during 2022–2024, selling 140k units in 2022 on the back of FAME-II subsidies, scaling to 270k units in 2023, and peaking at 407k units in 2024, giving it a 35–50% market share and over 900k cumulative sales, driven by aggressive pricing of the S1 Pro, rapid capacity expansion, and vertical integration. However, the bubble burst in 2025, with sales plunging ~51% YoY to 200k units. The downturn was driven by quality issues, service and after-sales delays, vehicle fire incidents, supply-chain disruptions, inventory challenges, and widespread customer complaints on social media, while legacy OEMs leveraged stronger dealer and service networks to regain consumer trust, compounded by a sharp 70% post-IPO stock decline that further dented confidence.

2026 and Beyond

The PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE) is India’s flagship central EV incentive program, launched on 1 October 2024 with a total outlay of allocating $197m for 2.47m e-2Ws (commercial/private registered, advanced battery only) to accelerate EV adoption, support EV manufacturing, and build charging infrastructure.

The scheme is scheduled to end in March 2026 for e-2ws. As a result of this, the effective price of many e-2Ws may increase unless OEMs adjust pricing or state incentives continue to fill the gap. Many state governments (e.g., Delhi, Maharashtra) are preparing enhanced local subsidies and benefits to support e-2W adoption.

With e-2Ws accounting for just 6% of overall two-wheeler sales in India, there is still significant ground to cover. Currently, e-2W sales are largely driven by tier-1 cities, as charging and service infrastructure needs to expand beyond urban areas to instill greater customer confidence. Electric two-wheelers remain harder to substitute for petrol-driven vehicles, especially motorcycles in rural and semi-urban markets.

A McKinsey study from 2023 projects electric two-wheelers to account for 60–70% of new sales in India by 2030, based on a survey of 1.2k EV consumers that emphasizes brand, safety, and sustainability.

Consumer buying behavior indicates a strong focus on battery life, charging infrastructure (with 35% citing gaps), and premium features such as 100+ km range. Around 86% of consumers are open to E-2Ws over ICE models, while omnichannel purchasing (with 85% starting online) and flexible ownership models, particularly financing, are emerging trends.

How Does Other Countries Fare in E-2W Sales?

China, India & Vietnam account for >95% e-2 wheelers sold worldwide.

About 55% of all 2-wheeled vehicles sold in China are electric. The next best region is Vietnam with 21% penetration.

The global average e2W sales share reached 15% over the first 10 months of 2025, slightly higher than the 14% sales share in 2024.

India’s electric two-wheeler story has moved from subsidy-led acceleration to a more competitive, market-driven phase. While growth has moderated since the post-FAME-II surge, record sales in 2025 underline that e-2Ws are firmly embedded in the mobility mix. The next leg of expansion will depend less on incentives and more on product reliability, pricing discipline, and the depth of charging and service networks beyond tier-1 cities. With e-2Ws still at just ~6% penetration, India’s transition is far from complete, but the foundations for sustained, long-term adoption are now in place.