.svg)

%2Bcopy.avif)

.svg)

.webp)

.jpg)

%20(1).jpeg)

.jpg)

A few years ago, shared electric scooters and bikes were seen as the future of getting around in India’s crowded cities. Startups like Bounce, Vogo, and Yulu entered the market with plans to fix last-mile travel and cut down on pollution. Yet, the initial consumer-facing (B2C) hype has significantly cooled. The sector hasn’t failed, it’s undergoing a critical and necessary pivot. The real question is: what challenged the B2C model, and what’s the path forward?

Terminology Note (India Context)

- Scooter: Family-friendly two-wheelers; 110 cc & above, like Honda Activa or TVS Jupiter

- Moped: Lightweight, lower-speed vehicle, used for short trips; <100cc (e.g., TVS XL).

- E-scooter (shared): Low-speed, electric two-wheelers from startups like Yulu, Bounce.

- Bike: Refers to bicycles (including e-bikes like Yulu Miracle), not motorcycles.

- Motorcycle: Geared two-wheeler with manual or semi-manual transmission; higher engine capacity (100cc and above), larger wheels; intended for more than intra-city commuting.

The Initial Players and the Market Shift

The market was initially characterized by high investment and rapid expansion.

- Bounce was an early leader, scaling aggressively to operate a fleet of 25k scooters and facilitating up to 120k rides daily in Bangalore and Hyderabad pre-pandemic.

- Vogo focused on key transit hubs, partnering with metro stations to provide last-mile connectivity.

- Yulu differentiated itself with purpose-built, lower-speed electric bikes (like the Miracle) and a stronger focus on forging partnerships with city authorities.

The COVID-19 pandemic was a major blow. As the ITDP report noted, the pandemic "caused many of the micromobility companies across the world to shrink or shut down their operations". During this period, Bounce’s revenue contracted by 83%. While services have recovered, the initial consumer-facing (B2C) hype has not fully returned. Many players have since pivoted or drastically scaled down their ambitions.

Competing with the Family Scooter

The single biggest challenge for shared micromobility was the deep-rooted culture of personal vehicle ownership.

Presence of Scooters and Motorcycles: India is a nation of two-wheelers. There are over 260 million of them on the road. As the vehicle ownership report states, more than half of all Indian households own a motorcycle or scooter.

Dominant Mode Share: Two-wheelers are not a niche product; they are the backbone of urban mobility. In cities like Pune, Bengaluru, and Chennai, they constitute a significant majority of motorized transport.

Rising Sales: The preference for personal ownership is only growing. For a typical Indian family, owning a reliable scooter offers unmatched convenience, status, and cost-effectiveness for daily trips, making a rented shared vehicle seem less necessary.

Infrastructure and Operational Challenges

Poor Infrastructure: Indian cities lack dedicated cycling or micro-vehicle lanes. As the ITDP report highlights, this forces these small, slow vehicles to compete for space with cars, buses, and trucks, creating dangerous situations. There is also a lack of dedicated, organized parking, leading to cluttered sidewalks and public annoyance.

Operational Challenges: The "free-floating" model, where users can leave vehicles anywhere, led to rampant misuse. Scooters were dumped in lakes, thrown off bridges, and left blocking footpaths. This indiscipline, similar to what led Paris to ban 15k e-scooters, eroded public and government goodwill. While companies like Yulu implemented more organized docking zones, managing public behavior remained a significant operational hurdle.

The Result: A Safety Crisis

The combination of high-speed traffic, no dedicated lanes, and often-inexperienced riders led to accidents. While data from cities like Portland and Baltimore showed that severe injuries were relatively rare, the perception of risk was high. A study in Austin, Texas, found that one-third of e-scooter injuries involved first-time users, a likely scenario in India as well. The fear of accidents, for both riders and pedestrians, became a significant barrier to wider adoption.

The B2B Pivot

While the B2C segment struggled, a new opportunity emerged: business-to-business (B2B) logistics for quick commerce and delivery.

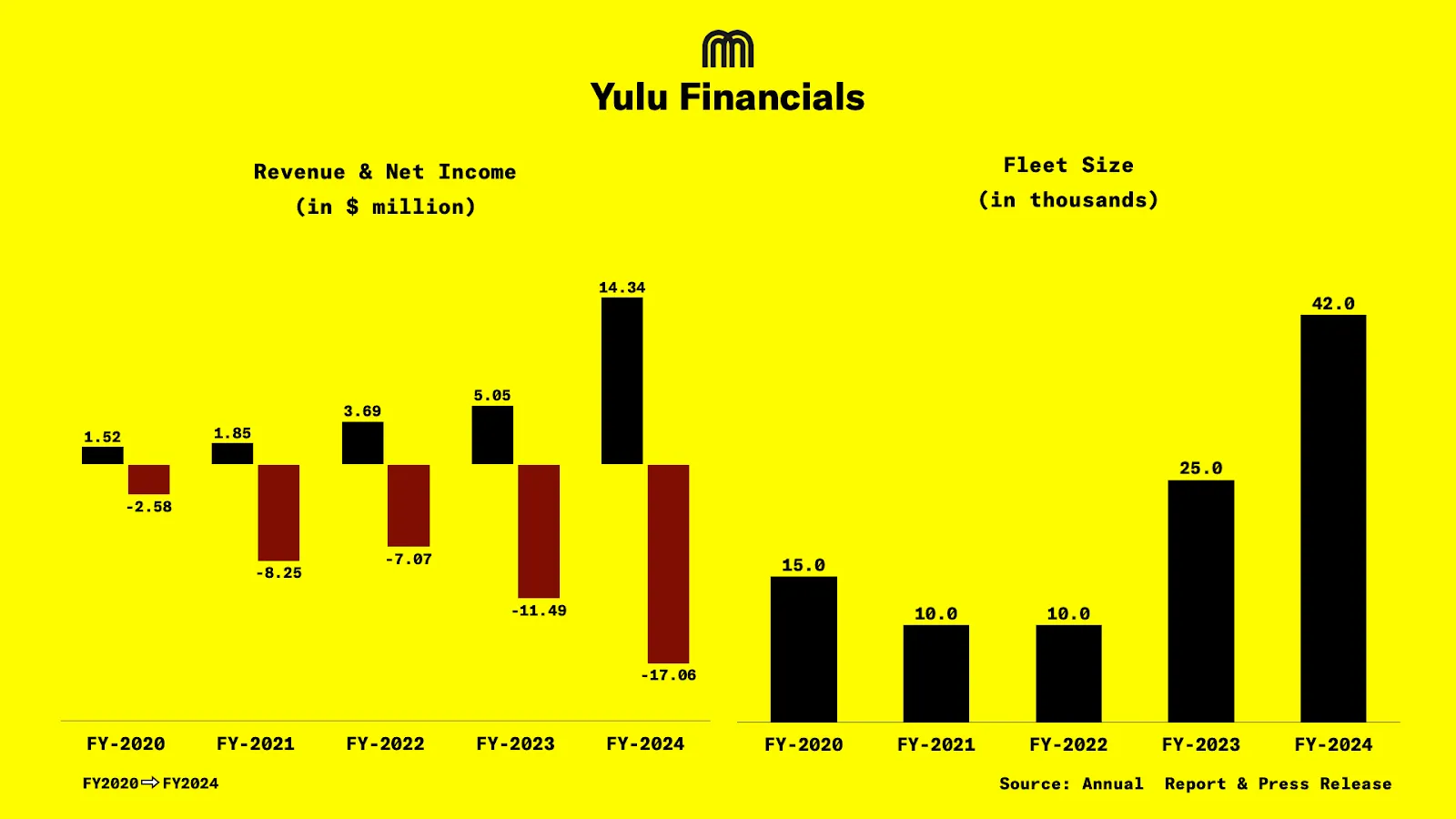

Yulu is the clearest example of this shift. Once positioned as a commuter-focused shared mobility startup, over 85-90% of Yulu’s revenue now comes from gig and delivery workers who rent its purpose-built e-bikes for platforms like Blinkit, Swiggy Instamart, Zepto, and Zomato. The company has introduced flexible rental plans (daily, weekly, monthly) for delivery riders, and tripled its revenue from $3.69m in FY22 to $14.34m in FY24.

As of September 2025, Yulu has raised $135m over 11 rounds. In June 2025, during its latest round, Yulu raised $11.3m. Further in its Series-C round, the company plans to raise $100m, which will be a mix of equity and debt.

Yulu’s fleet comprises Miracle & Yulu DeX vehicles. Approximately 85-90% of the revenue is generated from the Yulu DeX EV Fleet, which is utilized by gig workers across the country. Yulu is adding more than 4k DeX vehicles to its fleet each month.

Yulu is planning to expand its fleet to 100k vehicles by November 2025.

Zypp Electric has also built a strong presence by providing end-to-end fleet services: electric scooters, trained riders, battery swapping, and maintenance. With a fleet of 22k+ EVs and partnerships across e-commerce and grocery delivery, Zypp is fulfilling millions of shipments monthly. By handling charging and maintenance, it removes operational headaches for delivery platforms while helping them meet sustainability targets (source).

Bounce Infinity is another case of reinvention. After its dockless scooter-sharing model collapsed during the pandemic, Bounce pivoted to EV manufacturing and leasing.

Bounce saw its revenue drop from about $11m in FY23 to $4.3m in FY24, a 60% decline, with losses of around $5.3m. The slump was driven by phase-2 battery compliance, which stalled production for six months. In FY23, Bounce had reported revenues of $11m and losses of $23.9m, with a portion coming from bespoke manufacturing for Belrise. FY24 audited results are yet to be filed.

In FY2025, the company is targeting ₹100 crore revenue in FY25. Its plug-and-play EV leasing model offers scooters on long-term contracts (with maintenance, insurance, and battery-swapping access) at up to 30% lower cost than alternatives. In the last quarter alone, Bounce added 3k scooters for logistics partners, with lease-to-own options designed to retain gig workers. This positions Bounce firmly as a B2B-first player in the delivery ecosystem source.

The economics of the B2B model are compelling: delivery executives keep vehicles in constant use, which drives higher utilization rates, predictable revenue, and faster payback cycles for operators. Quick commerce’s explosive growth, India’s Gross Merchandise Value (GMV) in this sector jumped from $500m in FY22 to $3.3B in FY24, with projections to reach nearly $10 billion by 2029, ensuring steady demand for low-cost, zero-emission delivery vehicles (India Briefing, 2025).

Conclusion

India's shared micromobility dream isn't dead, but has fundamentally changed. It failed to replace the family scooter because ownership is too deeply ingrained and convenient. It was hampered by a lack of safe infrastructure and user indiscipline.

However, its future may not be with the average commuter, but with the delivery executive. The rapid rise of quick commerce has paved the way for a viable, economically sustainable B2B model that leverages the strength of electric micromobility, low cost, and zero emissions, for a practical, commercial purpose.