.svg)

%2Bcopy.avif)

.svg)

.jpg)

.webp)

.webp)

Welcome to Micromobility Pro, a bi-weekly publication which is part of The Micromobility Newsletter, where we deep-dive into the financials of micromobility companies and share exclusive insights tailored for professionals and members.

Last Chance to Save on Micromobility Europe 2026!

Micromobility Europe 2026 brings the global micromobility community to Berlin for 2 days of ideas, products, and conversations that move the industry forward. Join us on June 2-3, 2026 at Arena Berlin. Grab your General Admission ticket at €599 before prices go up tomorrow. Tickets are limited and selling fast!

Join McKinsey, Rivian’s ALSO, Lyft Urban Solutions, RYDE, Voi, Lime, Dott, NextBike, POLIS, Urban Sharing, Navee, CityFi, VMAX, Minimal, Microlino, and many others!

Everything you need to know about Micromobility America | Nov 11-12 | Palace of Fine Arts, SFO - CHECK HERE!

Bosch has a seat reserved for you at MME26!

Bosch is showcasing the latest capabilities of their Connected Biking platform at MME26 and offering selected partners a free pass plus exclusive early access to an upcoming innovation. Interested? Submit your details and their team will reach out if you qualify.

Contents

- Introduction

- The Bicycle Kingdom

- The Shift

- Hangzhou’s Quiet Start

- The Campus that Started Everything

- The Rainbow War

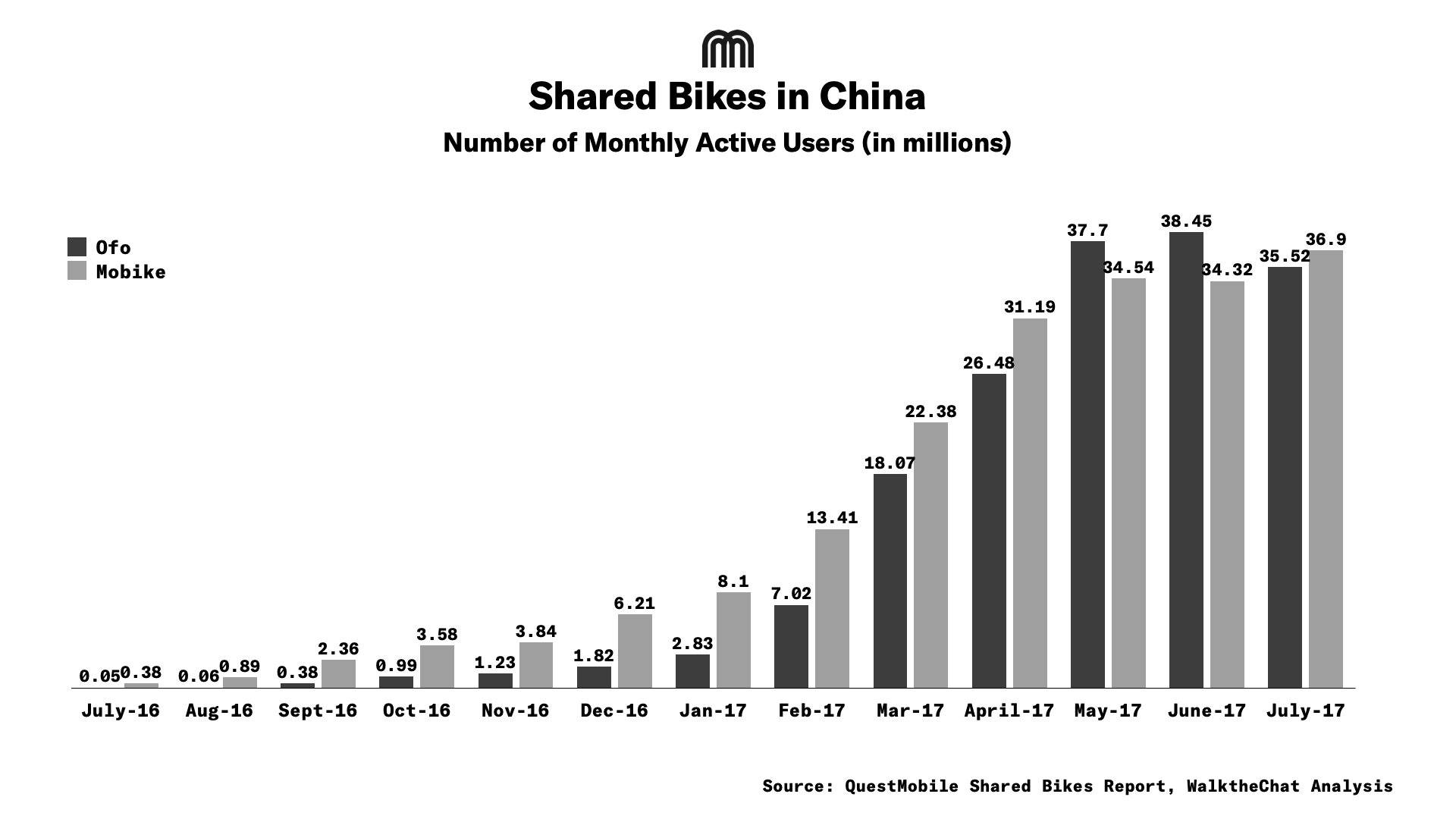

- Chart: Shared Bikes in China

- What Followed

Introduction

By November 2023, Beijing’s shared bicycles had carried riders on more than 1B trips in a single year. On an average day, 3.12m rides were being taken across the city. The number was a record. It was also, in many ways, the end of a very long and turbulent road.

To understand how a billion rides became routine, we have to go back to a time when China was burying its bicycles.

The Bicycle Kingdom

China’s relationship with the bicycle is older and more complicated than the sharing economy story suggests.

The bicycle arrived in Shanghai in 1868, treated as a curiosity, an expensive Western import that ordinary people could not afford and had little reason to want. That perception held for decades. It was not until 1950 that China produced its first homegrown bicycle brand, Flying Pigeon, launched in Tianjin with government backing. Even then, through the 1950s, owning a bicycle marked you as relatively prosperous. The machines were still beyond the reach of most households.

The 1970s changed that. Bicycle manufacturing scaled up steadily through the decade, and by the late 1980s, over 60 national bicycle manufacturers were operating across the country, supported by thousands of parts and accessory producers. In Beijing alone, the bicycle population was growing by more than 500k units per year. By the time the 1990s arrived, an estimated 500m bicycles were in circulation across China. Peak urban ownership hit 197 bicycles per hundred households in 1996. The “Bicycle Kingdom” label was not a metaphor, half a billion bicycles were in circulation across the country.

Then the government made a decision that would reshape the country’s streets entirely.

The Shift

China’s economic reform, launched under Deng Xiaoping, China’s paramount leader, in 1978, had been building momentum for nearly two decades when, in the mid-1990s, Beijing threw its policy weight behind the automobile industry. The logic was clear, car manufacturing meant jobs, industrial growth, and a modernising image.

The results were immediate and dramatic. Average bicycle ownership in Chinese cities fell from 197 per hundred households in 1996 to 113 by 2007. In Beijing, bicycles went from carrying 41% of all daily trips in 1995 to under 28% a decade later. The infrastructure followed the policy, roads widened for cars, cycle lanes disappeared or narrowed, and the urban environment became progressively less hospitable to anyone on two wheels.

Cycling did not disappear, but it changed its meaning. It became something people did for leisure or fitness, a weekend activity, a lifestyle choice, a nostalgic nod to an earlier era. As a serious, practical way to move through a city, it largely stopped being taken seriously.

Meanwhile, the cities that had been designed around the bicycle were now filling with cars, and the consequences were arriving fast. Traffic congestion in Chinese mega-cities became severe enough that on gridlocked roads, cycling was measurably faster than driving. Air quality deteriorated. And a structural problem was quietly building: in a country rapidly expanding its subway and bus networks, nobody had solved how to connect those transit hubs to the places where people actually lived and worked. The last kilometre was a gap that buses could not fill and taxis were too expensive to plug for daily use.

The bicycle, it turned out, had left a problem behind when it retreated.

Hangzhou’s Quiet Start

In 2008, the city of Hangzhou launched China’s first serious public bike-sharing programme, deploying 2.8k bicycles across a network of fixed docking stations. The model was familiar to anyone who had seen similar systems in European cities, users registered for membership, collected bikes from designated stations, and returned them to any other station in the network. The city government managed the whole operation.

It worked. Not spectacularly, but reliably. Hangzhou’s programme demonstrated that Chinese urban residents would use shared bicycles when the system was convenient and the price was low. A company called Yonganxing built a business around operating station-based systems on behalf of municipal governments, eventually serving over 200 cities, mostly small and medium-sized ones where a finite number of docking stations could adequately cover the urban area.

The model had a hard ceiling, though. In large, sprawling cities like Beijing or Shanghai, building enough docking stations to offer genuine coverage was financially impossible. A station-based system in a mega-city served the areas around its stations well, and everywhere else not at all. Users had to plan their trips around where the stations happened to be. The membership process was cumbersome - smart cards, municipal registration and prepaid fees. It was useful infrastructure, but it was not transformative.

The gap between what station-based sharing could do and what Chinese cities actually needed was large. Filling it required a different kind of thinking entirely.

The Campus That Started Everything

In August 2014, a Peking University student named Dai Wei co-founded a company called ofo. The idea was simple to the point of being obvious in retrospect: universities were full of bicycles that sat locked and idle most of the day. What if students could share them instead?

The first deployment stayed entirely on campus. No docking stations. No government permits. Just GPS-equipped bikes, a smartphone app, a QR code lock, and a deposit of around 99 yuan, roughly $15, to get started. A single ride costs less than 1 yuan. The barriers to use were close to zero.

Within a year, over 2k ofo bicycles were moving around the Peking University campus. The model spread quickly to other Beijing universities. It was fast, cheap, and it worked because it did not try to do too much, it solved a real, specific problem for a dense population of smartphone-carrying young people in a contained geographic area.

Mobike launched in January 2015, but with a fundamentally different ambition. Where ofo began small and campus-focused, Mobike aimed at city-wide deployment from the start. Its bicycles were more expensive to build - heavier, fitted with keyless digital locks and GPS, designed to be harder to steal or damage. In April 2016, Mobike launched in Shanghai, then moved into Beijing, Shenzhen, and Guangzhou in quick succession.

By the end of 2016, 5 stationless bike-sharing companies were operating in China.

What came next, nobody had planned for.

The Rainbow War

The venture capital industry saw what was happening on Chinese city streets in 2016 and moved fast. In the second half of that year alone, more than 30 investors injected capital into 11 bike-sharing companies, pushing total industry funding past RMB 3B in 6 months. Between 2016 and 2017, the sector raised close to $5B. Mobike collected around $1.2B. ofo raised $.45B. HelloBike, a relative newcomer backed by Alibaba, pulled in $350m.

Each brand staked its territory with colour, yellow for ofo, orange for Mobike, green for Didibike, and blue for Xiaomingbike. Observers started calling it the Rainbow War. The name captured something real: this was not competition in any conventional sense. It was an all-out land grab, measured in bicycles deployed rather than revenue earned.

By the end of 2016, ofo had placed over 800k yellow bicycles across more than 30 cities, holding 51% of the market. Mobike’s 500k orange bikes had captured 40%. By April 2017, over 40 dockless bike-sharing startups had launched their own apps. By mid-2017, 77 companies were operating 23m shared bicycles across the country. Registered users reached 209m. The market was valued at RMB 10.28B.

The scale of adoption was genuine. Bike-sharing had touched something real in Chinese urban life. In 2016, the number of shared bicycle users was approximately 8 times what it had been in 2015. The integration with public transit was working, people were cycling to subway stations in the morning, locking up outside metro exits, and cycling the final stretch home in the evening. Studies showed that around 31% of all bike-sharing trips in cities with major rail networks happened in the immediate vicinity of transit stations during rush hours. The first and last mile problem that had quietly built up as car culture displaced cycling was being solved, and solved at scale.

But the economics underneath the growth were not sustainable, and the companies knew it. Every ride was being priced below cost. The strategy was market share first, profit later, a bet that whoever captured enough users would eventually be able to raise prices, or monetise the data, or get acquired. The competition to win that bet pushed companies to keep deploying bicycles regardless of whether demand justified it.

What Followed

The system could not hold the weight of what had been piled onto it.

In July 2017, Wukong bike-sharing became the first company to collapse. Three more followed in August. Companies that had been subsidising rides and handing out free memberships reversed course, cutting incentives in an attempt to stop the financial bleeding. The shift came too late for many. By March 2018, the number of operating companies had fallen from 77 to 17.

What the failing companies left behind was visible to anyone who drove to the outskirts of Chinese cities. Open lots and empty land on the periphery of Beijing, Shanghai, Hangzhou, and dozens of other cities had filled with discarded bicycles, hundreds of thousands of them, heaped in enormous piles. Yellow ones, orange ones, blue ones, stacked and tangled together. These were the bike graveyards, and the images of them circulated widely, becoming one of the defining photographs of the era.

The human cost was less visible but more lasting. ofo had collected deposits of 99 to 299 yuan from millions of users. When the company effectively stopped functioning, those deposits did not come back. As of 2024, at least 16m people are still waiting for a refund. Mobike’s users eventually recovered their deposits, but only in late 2023, 6 years after the company’s collapse as an independent entity. The ripple effects hit manufacturing too. Shanghai Phoenix, one of China’s oldest bicycle producers, recorded a 46.68% drop in income in 2018, including over RMB 60m in unrecovered debt from ofo alone. Total shared bicycle production that year was 5m units, a quarter of what the industry had made the year before.

In Hangzhou, a city-wide cleanup reduced operational hire bikes from 88m at the start of 2018 to 390k by the end of the year. Guangzhou reduced its shared bicycle quota by 150k in a single tender round. Cities across the country that had watched the boom without intervening were now actively managing the fallout.

The Rainbow War had produced something the world had never quite seen before: a mobility experiment run at national scale, with billions of dollars of capital, that had simultaneously transformed how tens of millions of people moved through cities and generated enough discarded bicycles to fill a small country.

The graveyard photographs made for a clean ending. But they were not the end of the story.

Part 2 : How China rebuilt its bike-sharing industry, what the government did next, and how a billion rides became an ordinary day in Beijing - coming soon.

Got your micromobility moment to share? Email us at press@micromobility.io

Loving the vibe? Hop on and ride with us! Subscribe!

.png)