.svg)

%2Bcopy.avif)

.svg)

.webp)

.jpg)

%20(1).jpeg)

.jpg)

Contents

- Introduction

- Online Orders & E-Commerce Demand

- Chart: Enterprise Percentage of Online Sales and Turnover in the EU

- Chart: Yulu Financials and Fleet Size

- Funds Raised

- Chart: Funds Raised by Leading Last Mile Delivery Companies

- Chart: Fleet Size of Leading Last Mile Delivery Companies

- Company Brief: Zoomo, Whizz, Yulu, Amazon, Cycle, JOCO and Zypp

- Gig Workers

- Chart: Rental Costs of E-Bikes for Gig Workers

- Payback Period on the Fleet Invested

- Fleet Outlook & Different Form Factors

- Battery Swapping or Fixed Battery

- Delivery Robots

- Conclusion

Micromobility’s rise in delivery is driven by both necessity and opportunity. Congestion in major cities has made traditional delivery routes slower and more expensive, while emissions regulations and low-traffic zones are pushing companies to rethink how they operate. The last mile represents more than half of the overall cost of logistics operations, a problem that has only intensified as e-commerce exploded in 2020.

Bikes, e-bikes, scooters, cargo trikes, and small autonomous delivery bots are proving far better suited to short-distance, high-frequency delivery tasks. In cities like London, New York, Seoul, and San Francisco, logistics operators, retailers, and gig-delivery platforms are increasingly integrating these lighter vehicles into their fleets. For instance, in London, with low average traffic speeds and congested streets, cargo bikes moved 6% faster than cars by bypassing traffic and eliminating parking-related problems.

Online Orders & E-Commerce Demand

E-commerce represents 14% of total retail in the US, with 77% of the population spending online. This $1.1T market is key for international merchants.

In the EU, between 2013 and 2023, the share of enterprises that had e-sales increased from 17.21% to 23.83%. The turnover generated from e-sales increased from 13.81% to 19.12%. However, turnover in 2023 was 0.71 percentage points lower than the highest share recorded in 2019.

The Indian e-retail market, valued at approximately $60B in Gross Merchandise Value (GMV) in 2024, has established itself as the world's second-largest online shopper base. Quick commerce, projected to grow more than 40% annually through 2030, and hyper-value commerce, which has scaled to more than 12% of e-retail GMV, are gaining traction in smaller cities.

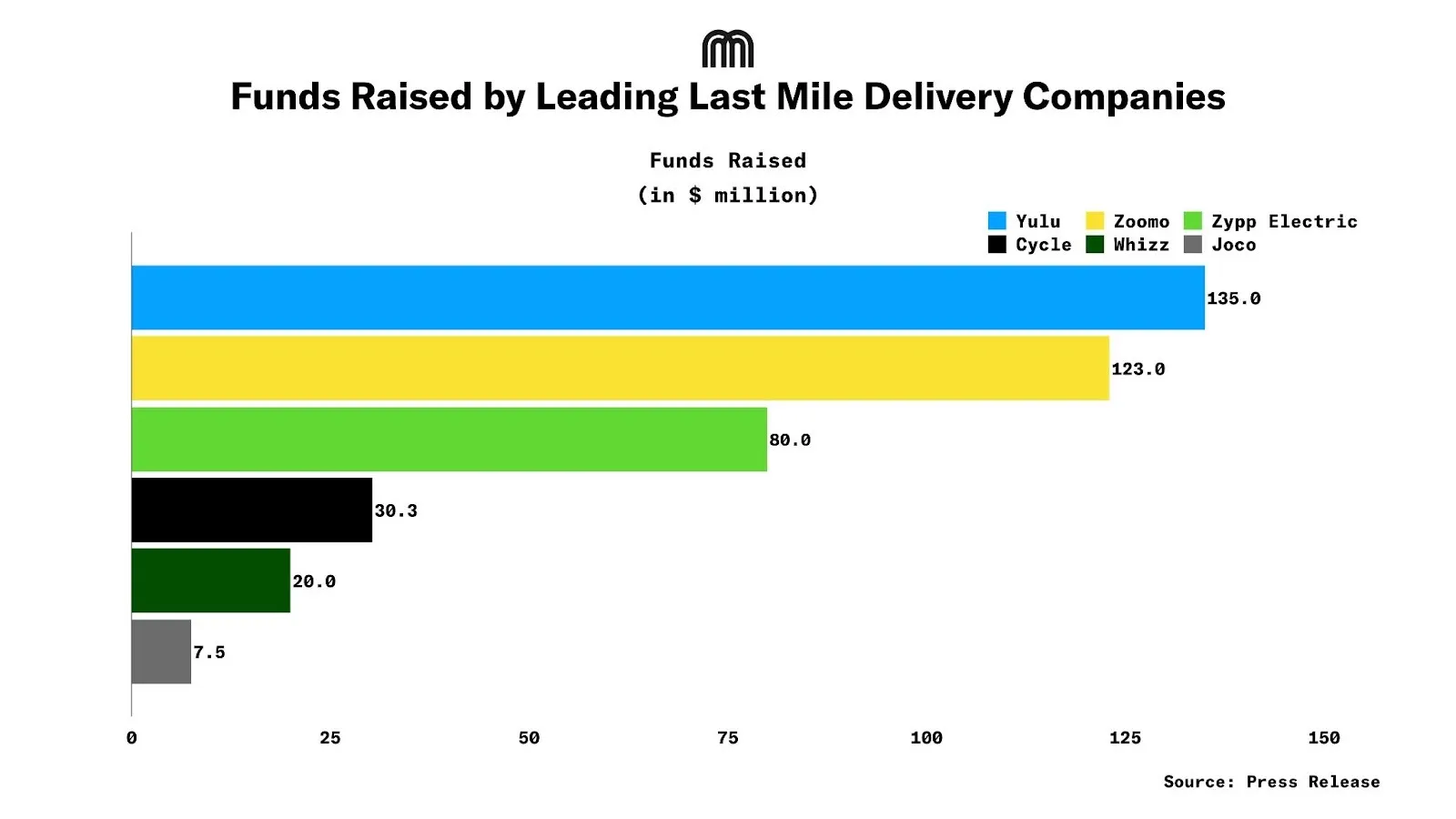

Funds Raised

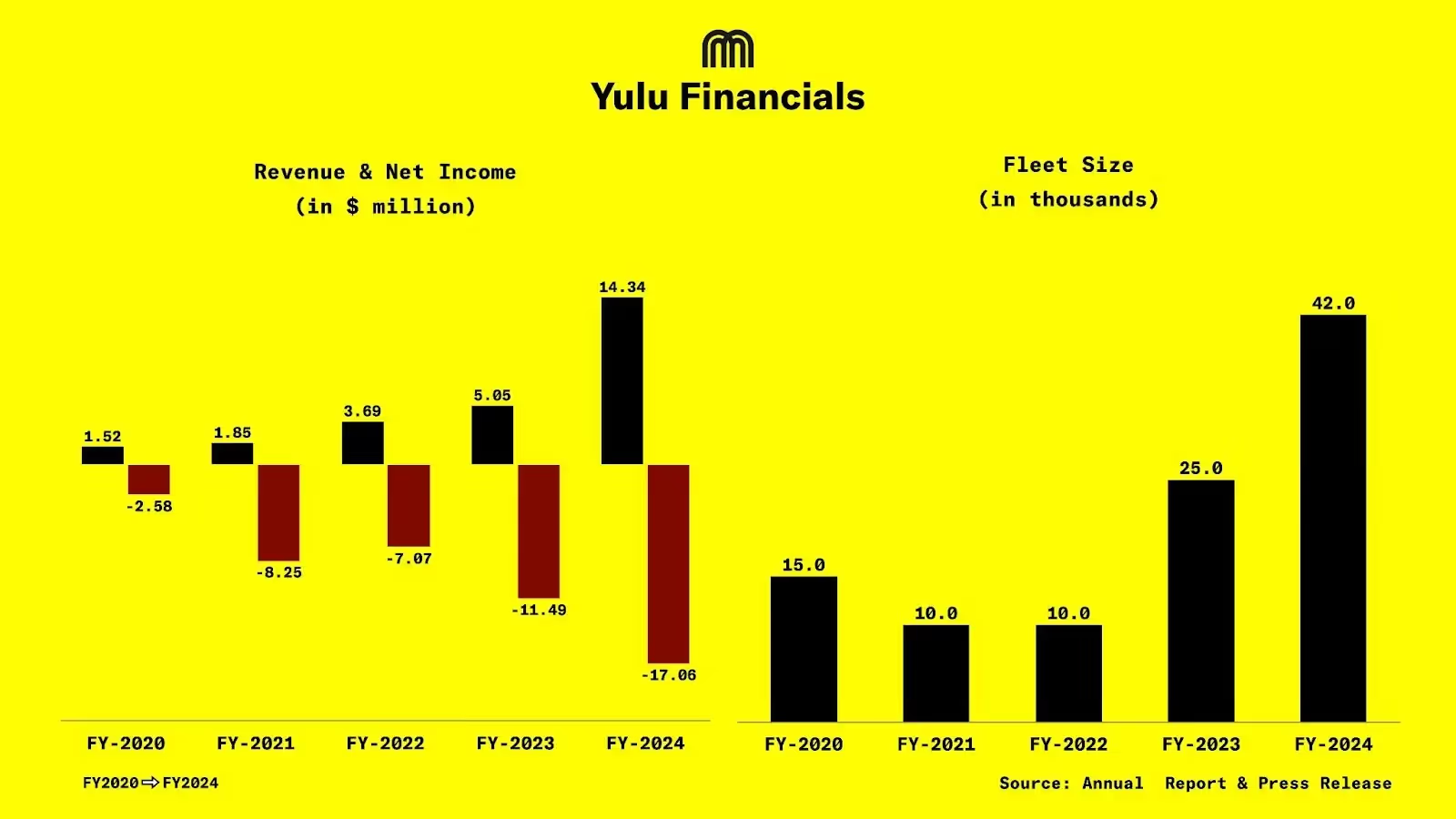

Yulu

As of September 2025, Yulu has raised $135m over 11 rounds. In June 2025, during its latest round, Yulu raised $11.3m. In its upcoming Series C round, the company plans to raise $100m, which will be a mix of equity and debt.

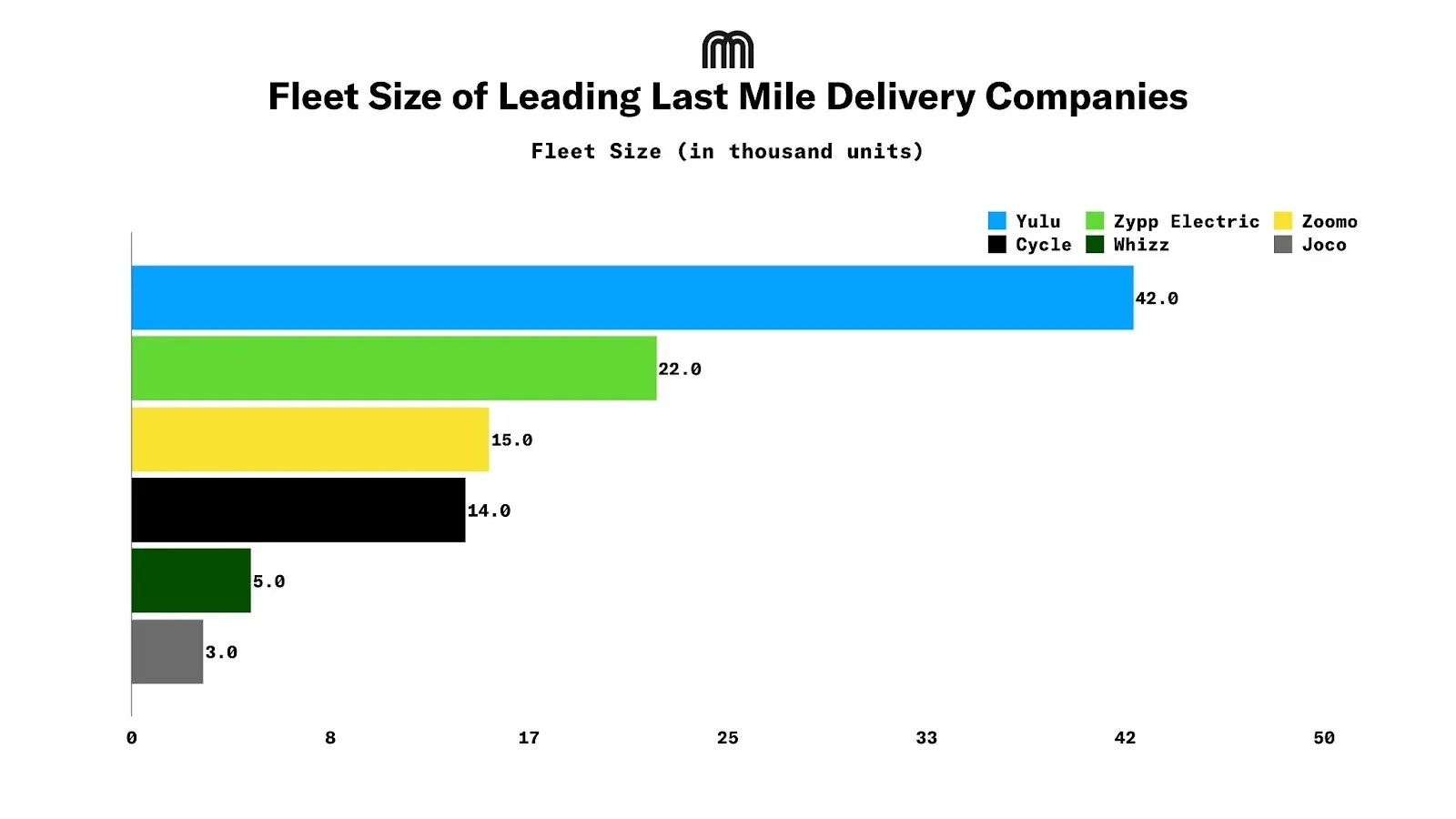

Yulu’s fleet comprises Miracle and Yulu DeX vehicles. Approximately 85% to 90% of revenue comes from the Yulu DeX EV fleet, which is used by gig workers across the country. Yulu is adding more than 4k DeX vehicles to its fleet each month.

Quick commerce is the fastest-growing segment, led by Blinkit, Zepto, Swiggy Instamart, and newer offerings like Flipkart Minutes and JioMart. As Yulu scales, it is adding mid-speed EVs to support multi-order e-commerce deliveries and additional logistics use cases.

Zoomo

Australia-based Zoomo has raised more than $123m in total funding. The company raised a $60m Series B in November 2021 and added $20m in February 2022 for European expansion, bringing the round total to $80m.

Zoomo operates in 16 cities across 7 countries. It maintains strong partnerships with Uber Eats, DoorDash, Just Eat Takeaway, and HungryPanda, offering exclusive rental discounts, servicing incentives, and promotional benefits. In some US markets, rental plans start as low as $15 per week or include servicing discounts up to 25%.

Whizz

Whizz has raised $20m to date. In June 2024, Whizz raised $12m in its Series A round, led by LETA Capital. At that time, Whizz reported annual recurring revenue of more than $8m, with year-over-year growth of 3.5x.

As of November 2025, Whizz operates about 5k vehicles and plans to scale its fleet to 70k vehicles by 2030, including the addition of electric mopeds.

Amazon

Amazon has been running micromobility pilots and hubs since at least 2022 in the UK and expanded from 2023 to 2025 across multiple European and North American cities. Amazon operates more than 70 micromobility hubs across the US and Europe, with deployments in Berlin, Manchester, London, Paris, Lyon, Munich, Antwerp, and several UK cities.

Partnerships & Fleet Additions

- Berlin. Amazon opened a micromobility hub near Alexanderplatz in July 2024 as part of a €400m investment to electrify and decarbonise Amazon’s German transport network.

- New York City. Amazon plans to scale its NYC micromobility fleet by more than 250 new e-cargo bikes in 2025, supplied partly by Mubea.

- Rest of Europe. Amazon continues to expand micromobility hubs in Antwerp, Berlin, Lyon, Manchester, and other cities.

- ALSO partnership. In October 2025, Amazon agreed to purchase thousands of pedal-assist cargo vehicles from ALSO, a Rivian spinoff, expanding into quad-style delivery vehicles designed for heavier loads. Deployment is set for 2026 across the US and Europe.

GetHenry (Cycle)

GetHenry, now rebranded as Cycle, raised €16.5m in seed funding in 2022 and €10.3m in a 2023 growth round, bringing its total publicly disclosed funding to about €26.8m. The company positions itself as a full-service e-bike subscription provider for delivery couriers and reports operating a fleet of more than 14k bikes across 90 European cities.

JOCO

JOCO pivoted from a public bike-share model to a courier-first model after early regulatory challenges. It built a docked e-bike network for delivery riders that includes battery-swap and charging cabinets, staffed rest stops, and app-based access control. JOCO operates dozens of stations across Manhattan, Brooklyn, and Queens, and expanded to Chicago in May 2025.

JOCO has raised about $7.5m in venture funding. The founders have said the limited funding forced a disciplined focus on unit economics and service quality, helping the company move toward profitability.

JOCO operates 1,000 e-bikes and approximately 120 stations across NYC.

Zypp Electric

Zypp Electric, an EV-as-a-Service platform for last-mile logistics, has raised more than $80m to date. The most recent funding was a $15m equity raise in its Series C1 round led by ENEOS, part of an ongoing $50m round. Zypp has also been in advanced discussions to raise an additional $25m to $30m as part of this round.

The company has scaled its fleet from ~6k vehicles in FY22 to more than 20k to 22k electric two- and three-wheelers today. Revenue increased from ~$34.29m in FY24 to ~$50.63m in FY25.

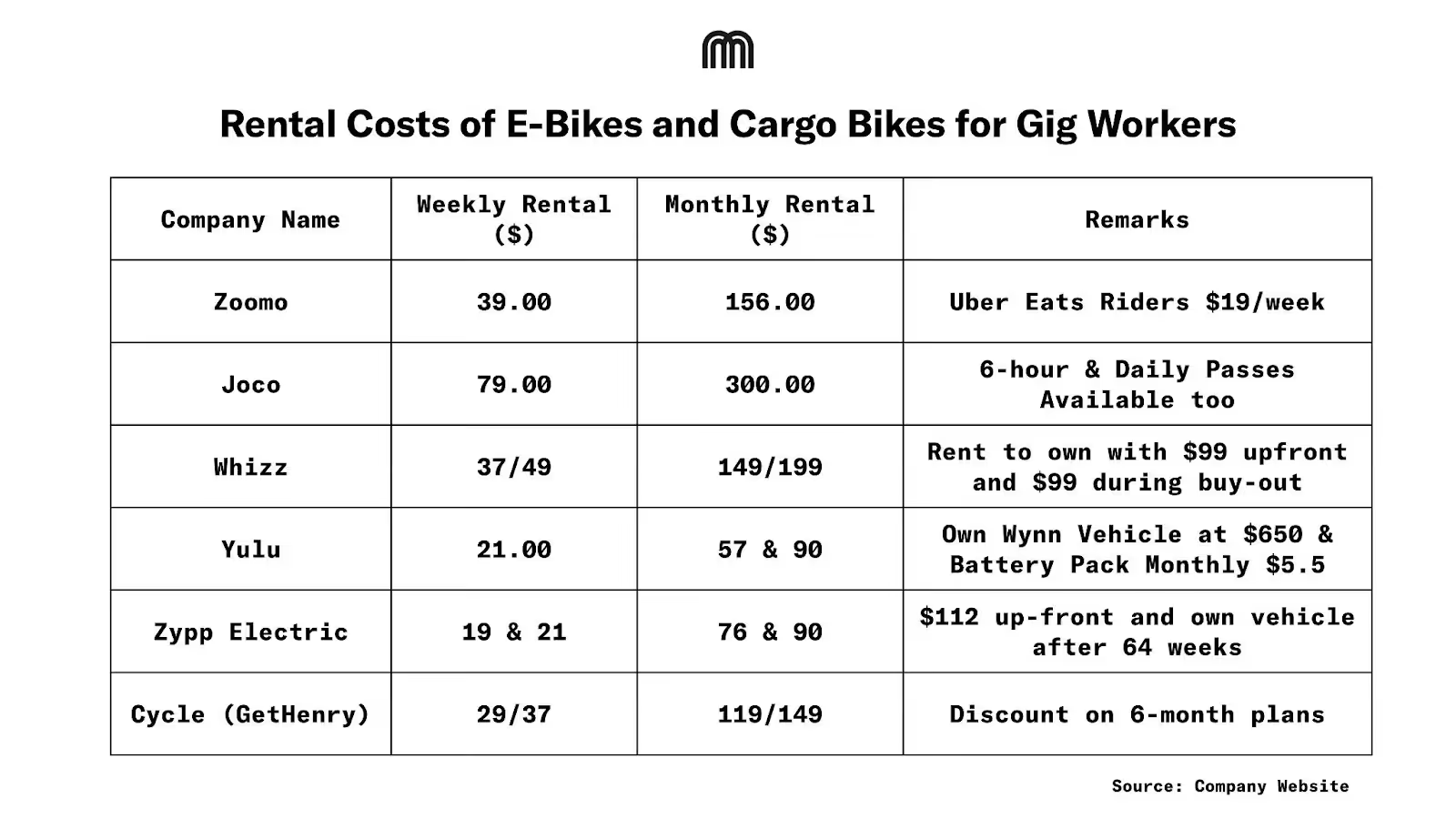

Gig Workers

As of 2025, the global gig workforce reached 1.1B people. Of this group, 72% work part-time alongside a primary job, and 28% rely entirely on platform-based income.

In India, quick commerce creates about 62 to 64 jobs for every ₹1 Cr ($120k) of sales, which is almost the same as general trade (63 to 66 jobs). It generates far more jobs than supermarkets (41 to 42 jobs) and regular e-commerce (25 to 29 jobs).

Within the quick commerce model, last-mile logistics is the largest employer, requiring more than 46 people per ₹1 Cr of monthly GMV. This dense labor footprint is essential for maintaining the required speed, proximity, and agility.

Zoomo noted that no single go-to-market model dominates across markets. Preferences vary by region, earnings levels, and job tenure expectations. In Australia, a workforce composed mostly of short-term backpackers tends to prefer weekly rentals. In Canada, longer-term riders with higher earnings tend to prefer ownership. In countries where gig workers are increasingly formally employed due to regulatory shifts, subscription models are the most popular because they are subsidized by employers and offer complete peace of mind.

Payback Period on the Fleet Invested

Zoomo reports that the payback period for its e-bikes is now under 12 months, an improvement driven by better hardware reliability, operational efficiencies, and economies of scale.

Yulu stated that its vehicles offer a strong payback period, with capital costs recovered well before the end of each EV’s lifecycle.

Fleet Outlook & Different Form Factors

Regarding future vehicle formats for last-mile delivery, e-bikes are expected to remain dominant among gig workers. Electric mopeds are projected to gain importance, especially in Europe, where platforms are moving away from petrol mopeds.

In fleet-based micromobility, regulatory uncertainty remains a major barrier to predicting long-term winners. However, vehicles offering van-like utility, such as e-quads equipped with seats, roofs, stability features, and reverse gear, are considered strong contenders to replace vans in dense cities.

Although the segment is dominated by two-wheeled vehicles, operators are evolving their fleets to support bulk or high-volume deliveries. This has led to the rise of three-wheeled and quad-style vehicles.

Honda launched its Fastport delivery vehicle in New York in June 2025. There are two variants. The larger model can handle up to 650 lbs of payload, and the smaller model can handle up to 320 lbs.

ALSO’s commercial quad bike, the TM-Q, is due in 2026 and targets logistics operators seeking low-cost, low-emission last-mile delivery solutions. ALSO has partnered with Amazon on a customized version of the quad that will join Amazon’s delivery fleet in Europe and the United States.

In India and Southeast Asia, the market has already embraced three-wheeled cargo vehicles. As cities become denser and delivery needs diversify, a mix of formats, ranging from mid-speed two-wheeler EVs to larger electric three-wheelers, will continue to operate side by side.

Battery Swapping or Fixed Battery

Operators prefer swappable batteries over fixed batteries due to charging time considerations. Fixed-battery vehicles reduce productive hours for gig workers.

Zoomo noted that the choice between swappable and fixed batteries depends on regulation, infrastructure, and market standards. Restrictions on home charging in some cities favor swapping. However, swapping infrastructure is capital intensive, which has historically led automotive players to favor fast charging. The absence of a dominant standard in Europe and North America complicates adoption.

Zoomo is pursuing both approaches, piloting swapping through partnerships with Swobbee and Silence, while also testing fast-charging capabilities with VMoto for electric mopeds.

Yulu stated that although both charging methods have advantages, swappable batteries are clearly superior for delivery use because riders do not lose time waiting for fixed batteries to charge. Swapping enables quick battery replacement, higher uptime, and increased rider earnings.

Delivery Robots

Delivery robots, once seen as a novelty, have matured into a viable component of modern urban logistics. Initially emerging in 2014 with prototypes from Starship Technologies, these autonomous vehicles have moved from pilot programs to commercial fleets operating in more than 80 cities globally by 2025.

Key Players and Market Growth

- Starship Technologies. More than 9m deliveries across more than 270 locations, more than $280m in funding.

- Serve Robotics. Backed by Uber and NVIDIA, operating semi-autonomous fleets in major US cities and partnering with Uber Eats to deploy 2k robots.

- Coco Robotics. Focused on local commerce, recently raised $80m to scale operations with partners such as DoorDash.

- Kiwibot. More than 250k deliveries, operating primarily on campuses.

- DoorDash. Recently introduced its own robot model, Dot.

Combined funding for the leading players exceeds $1B.

Conclusion

The rapid rise of micromobility has made it a central pillar of the global last-mile delivery ecosystem. As e-commerce, quick commerce, and hyperlocal retail continue to expand, lighter vehicles are proving not only environmentally preferable but also economically superior.

Vehicle formats will diversify, ranging from dominant e-bikes to specialized e-quads and three-wheeled cargo vehicles for heavier loads. Micromobility is no longer an alternative. It is now the primary mode for sustainable, profitable, and agile urban delivery.

Micromobility is deeply interconnected with the gig economy, which relies on efficient, low-cost vehicles. The varied preferences of the global gig workforce, from weekly rentals in short-duration markets to employer-subsidized subscriptions in regulated markets, are being met through increasingly flexible fleet and pricing models.

%20(1)%201.avif)

.png)