.svg)

%2Bcopy.avif)

.svg)

.webp)

.jpg)

%20(1).jpeg)

.jpg)

Welcome to Micromobility Pro, a bi-weekly publication which is part of The Micromobility Newsletter, where we deep-dive into the financials of micromobility companies and share exclusive insights tailored for professionals and members.

Join the leaders in micromobility. Get an annual subscription today to access the members-only Slack, event ticket discounts, and the full Micromobility Pro content library.

Contents

- Introduction

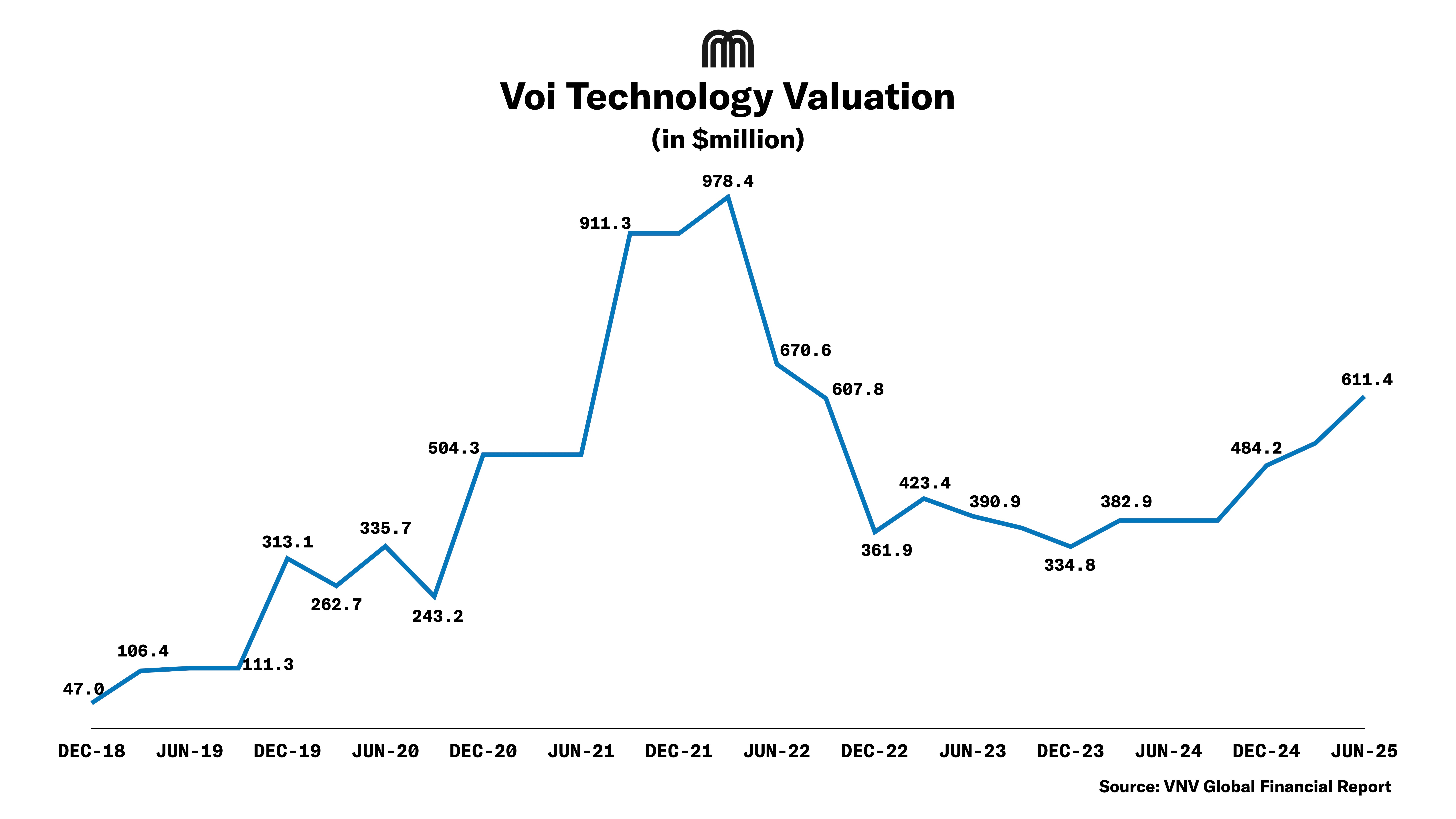

- Chart: Voi’s Quarterly Valuation Chart (2018 - 2025)

- Q2 2025 Financial Performance

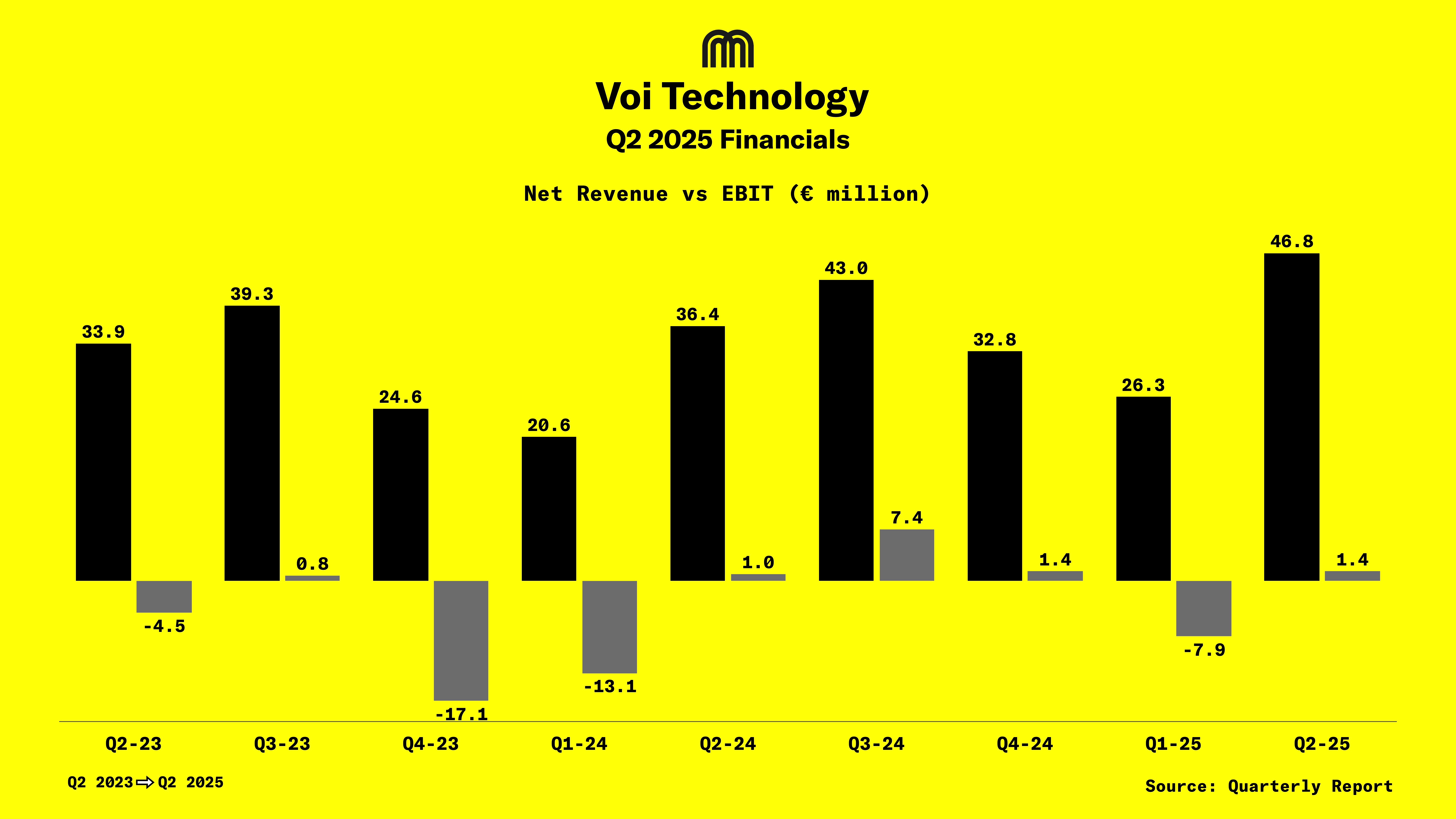

- Chart: Net Revenue vs EBIT ( Q2-2023 to Q2 2025)

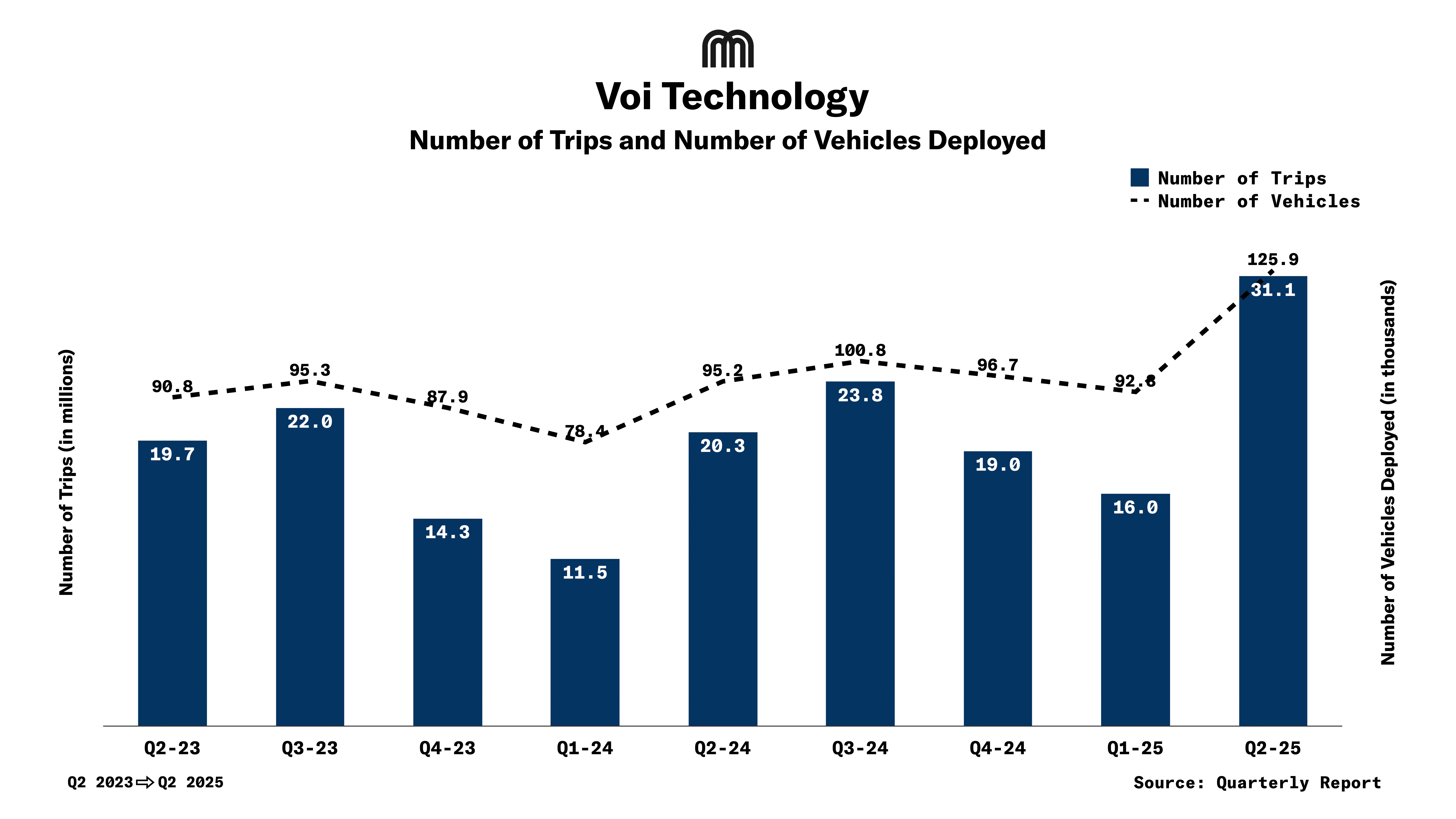

- Chart: Trips vs Vehicles Deployed ( Q2-2023 to Q2 2025)

- Revenue Breakdown

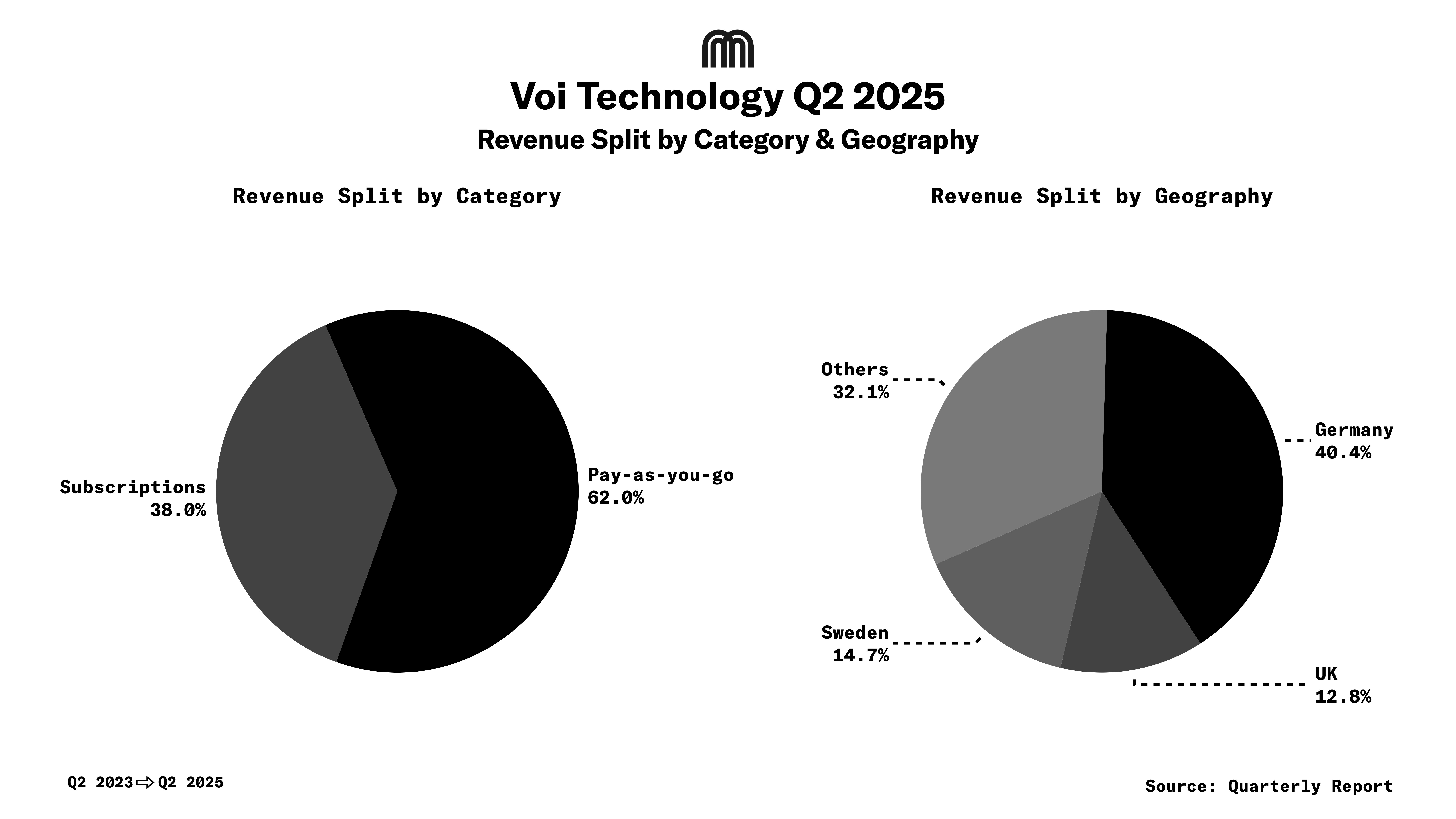

- Chart: Revenue Split by Geography and Category

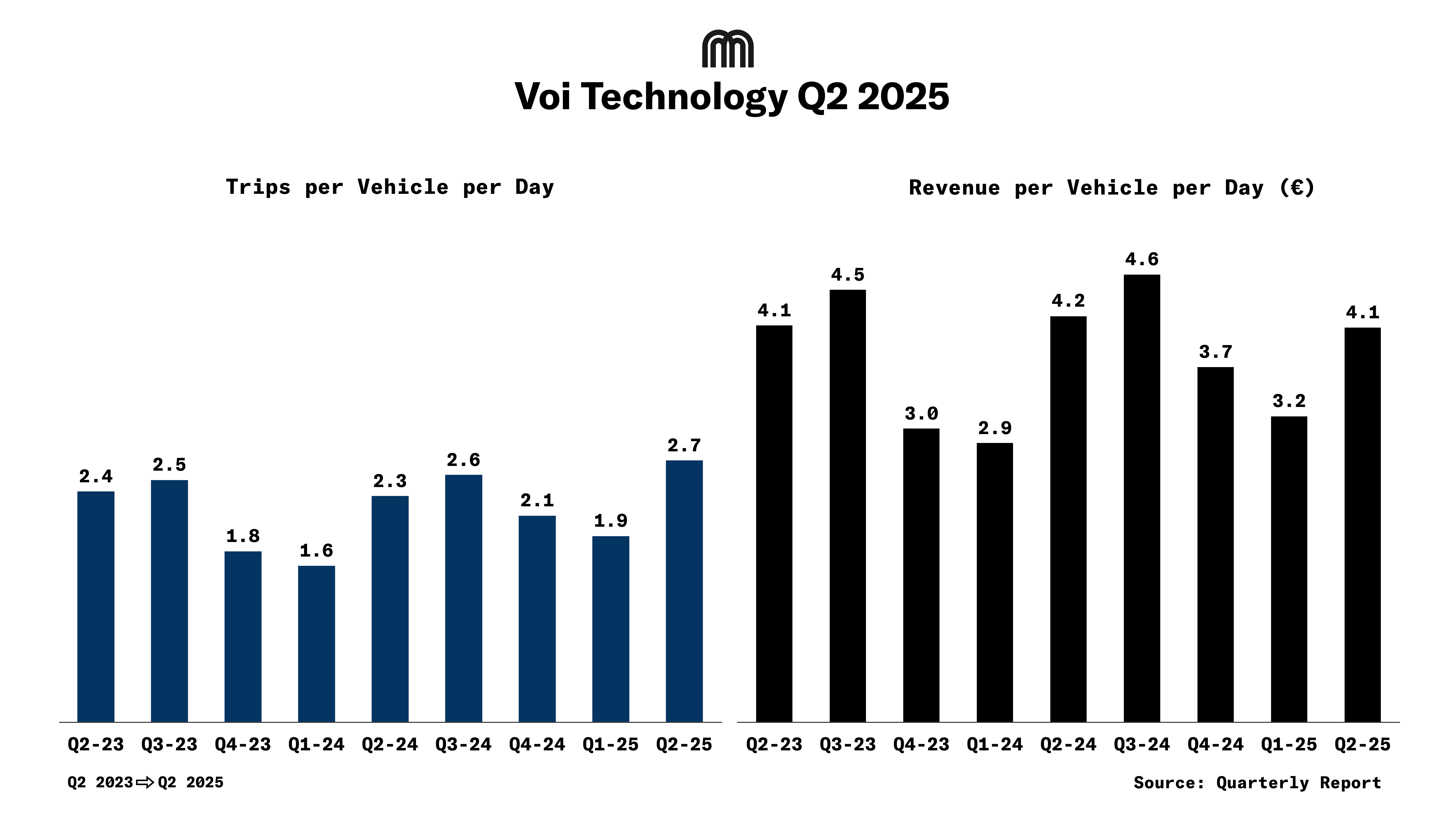

- Chart: TVD and RVD ( Q2-2023 to Q2 2025)

- Cost Structure

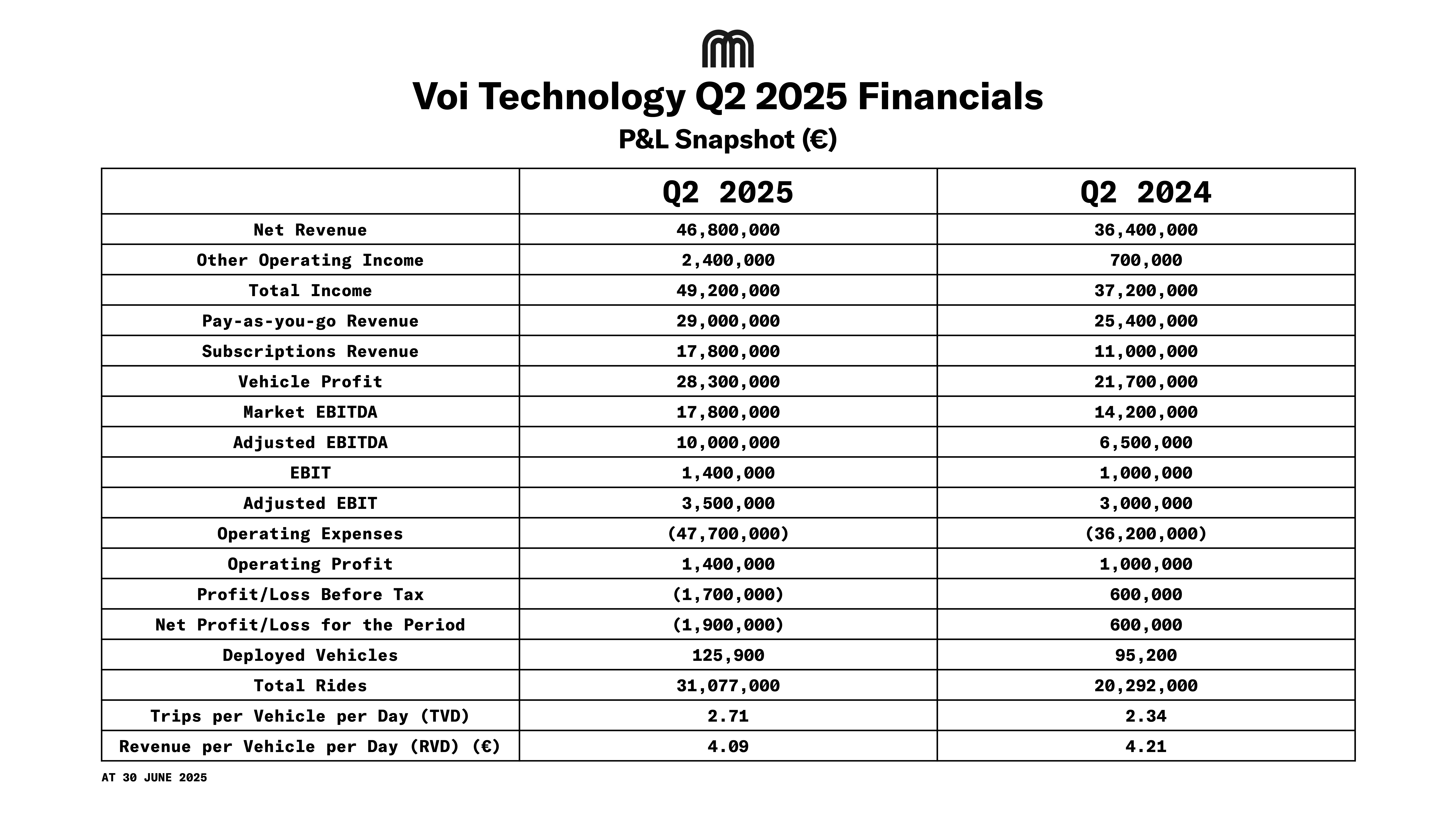

- Table: P&L Snapshot

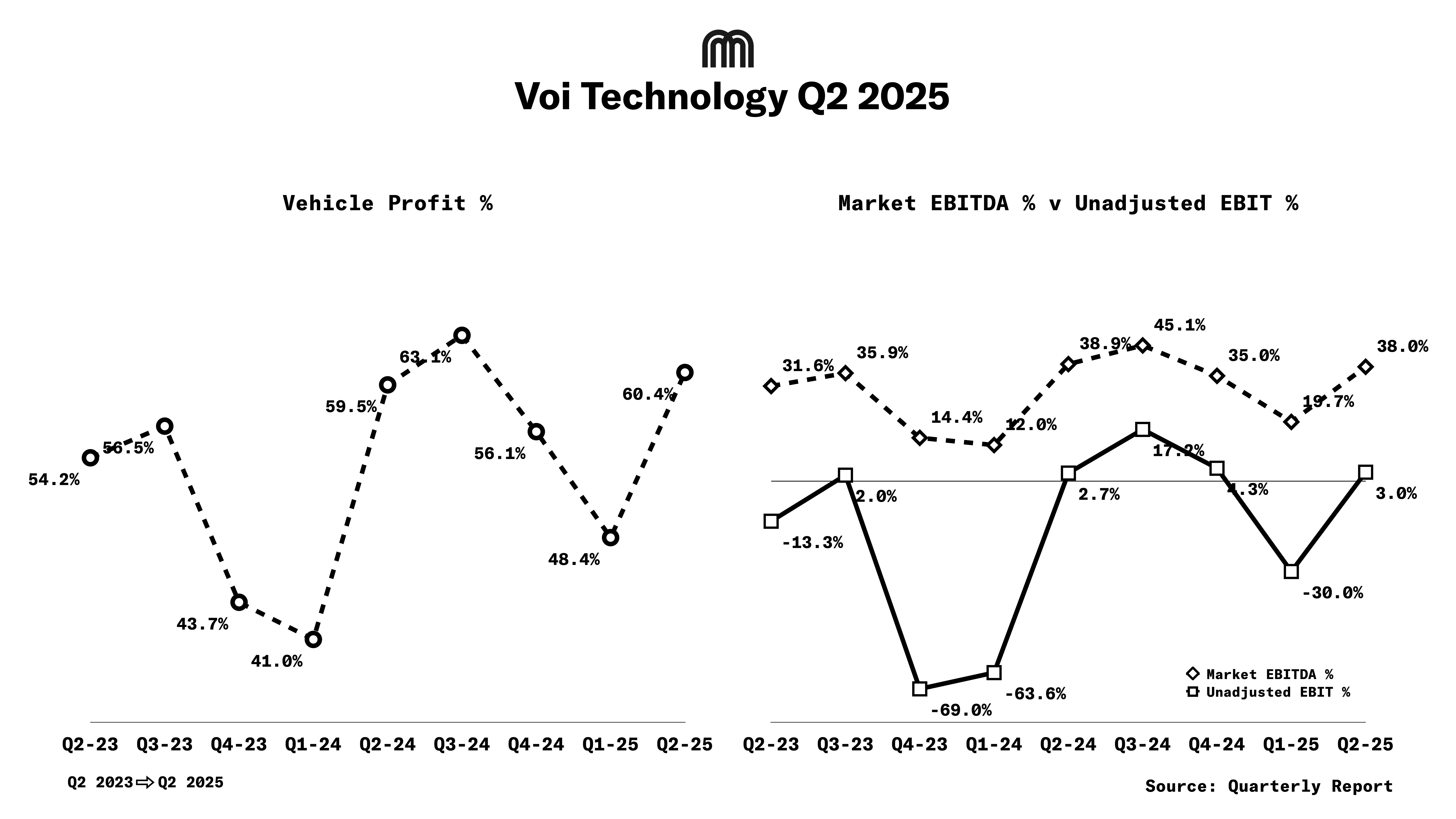

- Chart: Vehicle Profit %, EBITDA vs EBIT ( Q2-2023 to Q2 2025)

- Cash Position & Balance Sheet

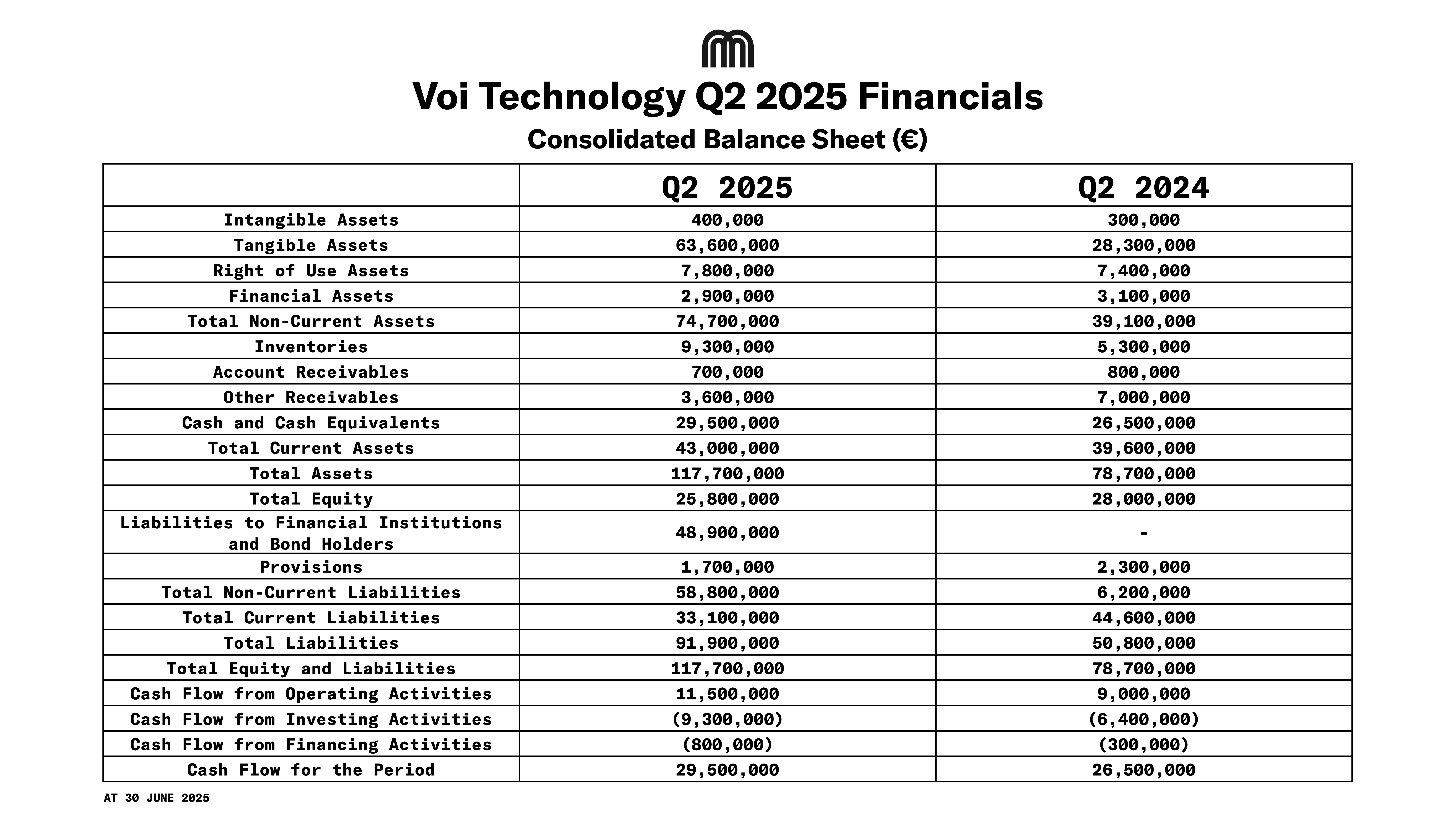

- Balance Sheet Snapshot

- 2025 Outlook

- Conclusion

Introduction

Voi’s Q1 2025 results showed a rebound: 28% YoY revenue growth, narrowing losses, and improved fleet use, but also highlighted issues like low revenue per trip and limited cash. Q2 2025 builds on that recovery and marks a key shift toward larger-scale operations and better financial performance.

What more? Voi’s investor VNV Global has marked up their valuation to $611.4m, up by 26% from December 2024. Voi breached the $600m valuation mark for the first time since September 2022 and VNV has been marking up Voi’s valuation for 5 quarters straight.

Just in case you missed, check this fireside chat with Voi’s Co-Founder & CEO Fredrik Hjelm at Micromobility Europe 2025

Q2 2025 Financial Performance

Voi reported strong growth in Q2 2025, with net revenue rising 29% year-over-year (YoY) to €46.8m, driven by a bigger fleet and more efficient use of vehicles.

The average fleet size grew 32% YoY, while rides rose even faster, up 55% to 31.1 million, signaling strong demand for Voi’s e-scooters and e-bikes. Despite this, revenue per vehicle per day (RVD) dipped slightly by 3% YoY to €4.09, from €4.21 last year. The growth in rides kept pace with the fleet expansion, helping maintain revenue per vehicle.

Profitability also improved:

- Vehicle-level profit margins rose 0.9 percentage points YoY to 60.4%, showing better operational efficiency.

- Adjusted EBITDA jumped 54% to €10.0m, with a margin of 21.3% (vs. 17.9% in Q2 2024).

- Adjusted EBIT increased to €3.5m (vs. €3.0m YoY), though reported EBIT was €1.4m, impacted by higher depreciation from new vehicle investments.

- Operating cash flow grew to €11.5m (up €2.4m YoY), highlighting the company’s ability to generate cash from its core business.

Revenue Breakdown

Revenue grew across all markets and product lines:

By Geography:

- Germany remained Voi’s largest market: €18.9m (+28% YoY).

- UK revenue rose 35% YoY, helped by e-bike expansion in London.

- Sweden: €6.9m (+19% YoY).

- Other countries: €15.0m (+33% YoY), including France, which grew 125% YoY (from a small base) due to recent wins like the Grenoble tender and other European launches.

By Product:

- Pay-as-you-go rides: €29.0m (62% of revenue).

- Voi Pass subscriptions: €17.8m (38% of revenue), up 62% YoY, reflecting stronger user loyalty.

Efficiency:

- Trips per vehicle per day increased to 2.71, up from 2.34 last year, showing Voi is making better use of its growing fleet.

Cost Structure

Even with its larger fleet, Voi improved margins:

- Vehicle profit rose 30% YoY to €28.3m, and margins expanded 0.8 percentage points to 60.4%.

- Maintenance and spare parts costs rose 41% YoY to €10.4m, driven by wear on the existing fleet and the rollout of new vehicles.

- Personnel costs fell 6% YoY to €16.6m, thanks to improved efficiency despite a 32% increase in fleet size.

- Depreciation rose 83% YoY to €6.4m due to heavy investment in 45,000 new e-scooters and e-bikes.

Voi also improved performance at the city and market level. Market EBITDA reached €17.8m, a 38% margin, up 25% YoY. One-time costs, mostly staff incentives, dropped to €2.1m from €4.8m in H1 2024.

However, financial expenses worsened to -€3.1m (vs. -€0.4m YoY), mostly due to €1.7m in unrealized losses from currency swings (SEK/EUR) affecting bond debt.

Cash Position & Balance Sheet

Voi strengthened its cash flow while continuing to invest in growth:

- Operating cash flow was €11.5m, up 28% YoY, showing improving business fundamentals.

- Cash reserves rose slightly to €29.5m, from €28.6m in Q1, but remained well below the €60.1m at the end of 2024, reflecting continued spending on expansion.

- Net debt fell to €27.1m, from €28.4m in Q1, thanks to improved cash flow.

The balance sheet remained stable:

- Equity held at €25.8m, vs. €26.6m in Q1.

- Non-current liabilities were flat at €58.8m, mostly long-term debt (€48.9m).

- Current liabilities rose to €33.1m, from €30.2m, due to higher accrued expenses.

- Voi still has access to a €4.5m unused credit line, offering some financial flexibility as growth continues.

Voi’s improving margins and ride volumes show it can scale profitably. However, high depreciation from fleet investments still weighs on earnings. Strong cash flow helps ease balance sheet pressure, but with cash down 51% YoY, tighter spending in the second half of the year will be key. The unused credit facility adds a useful financial cushion as Voi prepares to launch operations in Paris.

2025 Outlook

Voi heads into H2 with solid growth momentum.

- Fleet goal: Grow to around 150,000 vehicles by year-end, up 19% from Q2.

- Profitability: Q2 marked adjusted EBITDA breakeven. Full-year profitability is now within reach.

Key developments ahead:

- Paris launch: 6,000 e-bikes go live in autumn 2025, with potential to generate "double-digit millions" annually.

- E-bike focus: 45,000 new vehicles added in Q2, with a strategy to lead in both bikes and scooters.

Risks: Despite better margins, cash constraints persist. Voi’s reserves are down 51% YoY, now at €29.5m compared to €60.1m at the end of 2024. Net debt remains high at €27.1m.

Conclusion

Voi’s Q2 2025 results offer compelling evidence that shared micromobility can be profitable at scale. The company reported €1.4m in EBIT, 29% YoY revenue growth to €46.8m, and a 55% increase in rides to over 31m. Utilization hit a record 2.71 trips per vehicle per day, while vehicle-level margins remained solid at 60.4%, despite an 83% increase in depreciation.

What stands out is not just the return to EBIT profitability, but how it was achieved. Performance was driven by operational execution, improved fleet efficiency, and higher user engagement, not by promotional pricing or one-time gains. Operating cash flow reached €11.5m for the quarter, a clear signal that the business is beginning to generate real financial momentum.

The valuation mark-up by VNV Global, covered earlier, underscores growing investor conviction in this shift. But the path to full-year EBIT profitability is still uncertain. With the Paris contract expected to begin in Q4, its contribution this year will be limited. Delivering a profitable 2025 now depends on consistent execution across existing markets through Q3 and Q4. Liquidity remains tight, with €29.5m in cash and €27.1m in net debt.

In short, Voi has shown it can operate profitably at scale. The next test is whether it can sustain that performance over a full year, without relying on new capital or headline-grabbing expansion. If it does, it will have achieved what few believed possible in this category: a micromobility business that works, both on the street and on the balance sheet.

"We now operate with ample liquidity and a solid balance sheet, positioning Voi better than ever for long-term growth."

— Fredrik Hjelm, CEO

Read the full Q2 report here.

%20(1)%201.avif)

.png)