.svg)

%2Bcopy.avif)

.svg)

%20(1).jpg)

.webp)

.webp)

Germany sold 2.05m e-bikes in 2024. Most people who bought one never thought about where the parts came from. The e-bike was assembled in Europe, probably in Portugal or Romania, the two biggest bicycle-producing countries on the continent. The frame may have come from Asia. The battery cells almost certainly did. The drivetrain components likely passed through Taiwan or China before reaching the factory floor.

Europe has built one of the largest and fastest-growing micromobility markets in the world, but maybe it hasn't yet built its supply chain to match.

The European micromobility market generated $8.75B in revenue in 2025, accounting for roughly 19% of the global market. It is also the fastest-growing region, expanding at 18.1% annually. McKinsey projects the global value pool for private and shared micromobility could reach $340B by 2030, with Europe leading at $140B, ahead of China at $80B and the United States at $35B.

But market size and manufacturing capability are different things. The growth in demand has largely been met by existing global supply chains, chains that run, for the most part, through Asia.

What Goes Into a Bike, and Where It Comes From

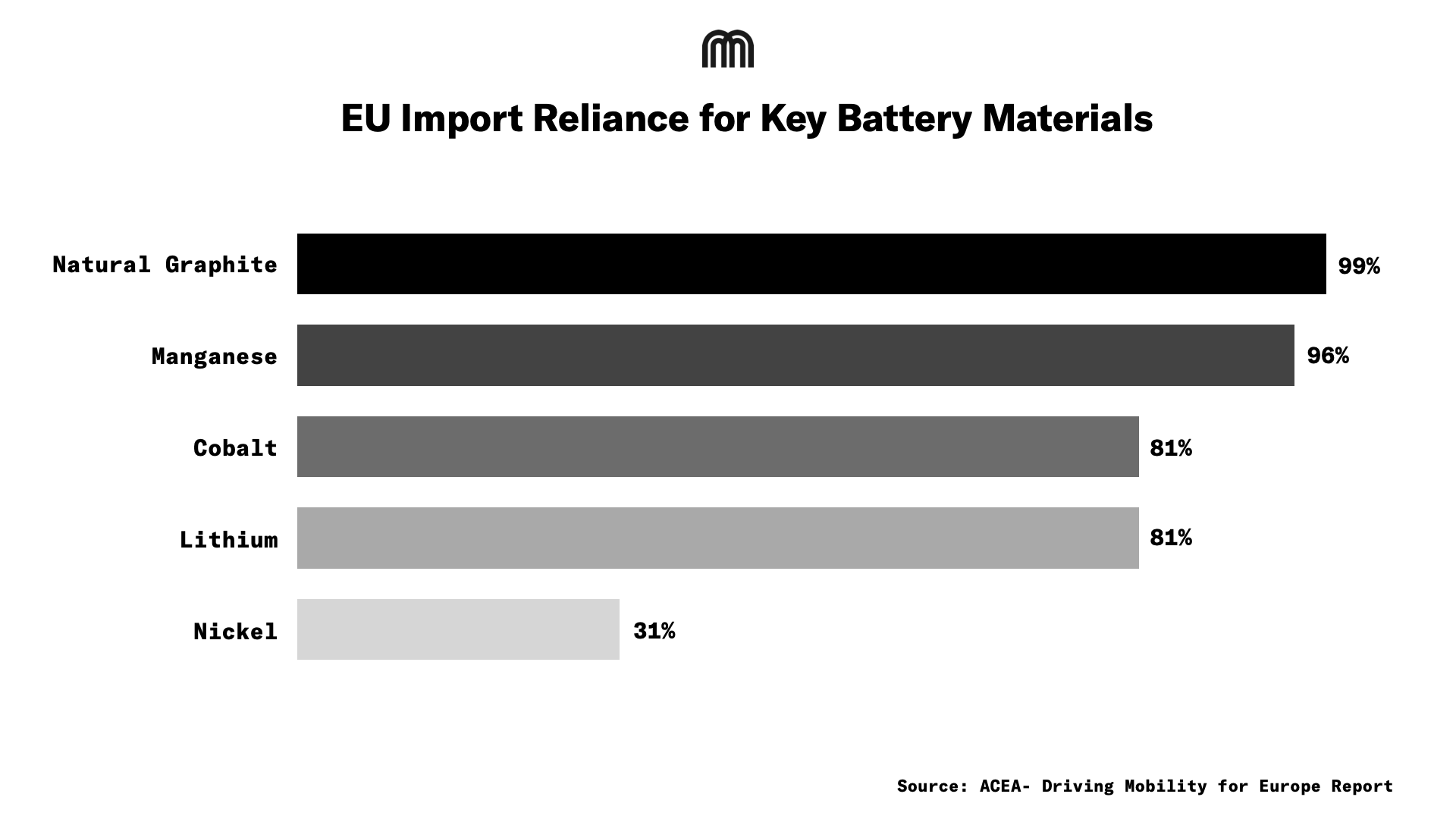

Start with the battery. The majority of battery cells used in Europe come from Asia. The EU imports 99% of its natural graphite, 96% of its manganese, 81% of its cobalt, and 81% of its lithium. These are the core materials in lithium-ion batteries, the same batteries in every e-bike, e-scooter, and cargo bike on European streets.

China controls between 70% and 90% of the global refining capacity for these materials and holds 85% of global battery production capacity. The EU accounts for just 7% of upstream battery supply chain capacity. China and the US together hold 87%.

Move up the supply chain to the bike itself. EU manufacturers produce real volume - Portugal (1.8m units in 2023), Romania (1.5m), Italy (1.2m), Poland (0.8m). But the frames and components feeding that production are heavily sourced from China, despite the anti-dumping duties on complete bicycles and e-bikes that have been in place since 2019.

The component picture sharpens the point. Shimano, the world's largest manufacturer of bike parts, produces in Singapore, Malaysia, China, and Japan. SRAM runs its largest sites in Taiwan and China. Only two derailleur systems are actually manufactured in Europe. Carbon fibre, aluminum tubes, cable holders, bearings, derailleur hangers, most come from outside the EU. Frame manufacturing follows the same pattern. UNNO moved production of its latest frame generation from Barcelona to Asia on price grounds. Liteville, Kavenz, RAAW, and Thömus are European brands, their frames are built in Asia.

How the Gap Formed

None of this reflects a failure of European industry. It reflects how global manufacturing specialisation developed over decades. China's supply chain ecosystem is the most large-scale and established in the world, the result of sustained investment, accumulated expertise, and sheer production capacity built over many years.

The exposure is set to deepen. EU demand for lithium is expected to increase twelve-fold by 2030. For rare earth metals, six-fold. Meeting that demand requires either securing supply from elsewhere or building domestic capacity, neither of which happens quickly. The pandemic made the fragility concrete, when shipping routes from Asia to Europe saw extraordinary cost increases and exposed how little buffer existed in just-in-time supply chains.

What Europe Is Building

Anti-dumping duties on Chinese e-bikes, ranging from 10.3% to 70.1%, with countervailing duties of 3.9% to 17.2%, have been in place since 2019. They've helped stabilise the market for EU producers in the entry-level and mid-range segments, allowed new European companies to enter, and encouraged investment in technology development and sustainable production. They are not a supply chain solution, but they create the commercial conditions in which one can develop.

The European Battery Alliance, launched in 2017, targets a complete domestic battery value chain, from raw material processing through to cell production and recycling, with an estimated annual market value of €250B from 2025 onwards. The Critical Minerals Act sets binding benchmarks: at least 10% of annual consumption extracted domestically, 40% processed within Europe, 25% recycled, and no more than 65% sourced from a single third country.

Capital is moving. In 2020, the European Investment Bank signed a $350m loan to support Northvolt's first lithium-ion gigafactory in Sweden, Europe's first domestically grown battery cell facility. In 2024, French battery startup Verkor secured over €1.3B in green financing for its gigafactory in Dunkirk.

What Localisation Would Mean

The case for building domestic capacity isn't just strategic, it's economic and environmental. Micromobility in Europe has the potential to create 1m jobs across the EU and reduce emissions by 30m tonnes of CO₂ equivalent by 2030. That positions it as one of the more significant levers in the decarbonisation of European transport.

On quality, proximity matters. Manufacturing in-house gives producers direct control over standards and consistency, something that becomes harder to maintain across long and fragmented global supply chains. The Microlino, which sources over 80% of its parts from Europe, mostly Italy, shows what that can look like in practice.

Looking further forward, battery lifecycle management is becoming a priority. Certified battery repair already delivers a 30% cost reduction compared to purchasing new OEM units. Battery passport systems that track lifecycle, repair history, and compliance will help operators manage fleets while meeting EU requirements under the Battery Directive and Extended Producer Responsibility obligations.

Where the Work Is

Labour costs in Europe are structurally higher than in Asia. Environmental standards, while necessary, add to manufacturing costs. Raw material constraints aren't solved by policy alone, processing infrastructure takes years to build. Battery disposal is already becoming a practical concern. In Germany, lithium batteries in circulation grew from 3k tonnes in 2009 to over 10k tonnes by 2017, and waste processing capacity hasn't kept pace.

Europe has the demand, the regulatory intent, and the early industrial investment. It doesn't yet have the full supply chain. The distance between riding a bike and building one - from lithium in the ground to battery cell to frame to final assembly, is long. Europe handles the final stretch well. The earlier stages remain a work in progress.

Cover image credits: Pexels