.svg)

%2Bcopy.avif)

.svg)

.webp)

.webp)

Contents

- About Bolt

- Ownership Structure

- 2024 Financial Performance

- Chart: Net Revenue vs Net Result ( 2013 to 2024)

- Chart: Revenue Split by Service Type

- Cost Structure Breakdown

- Chart: Revenue and Cost Breakdown

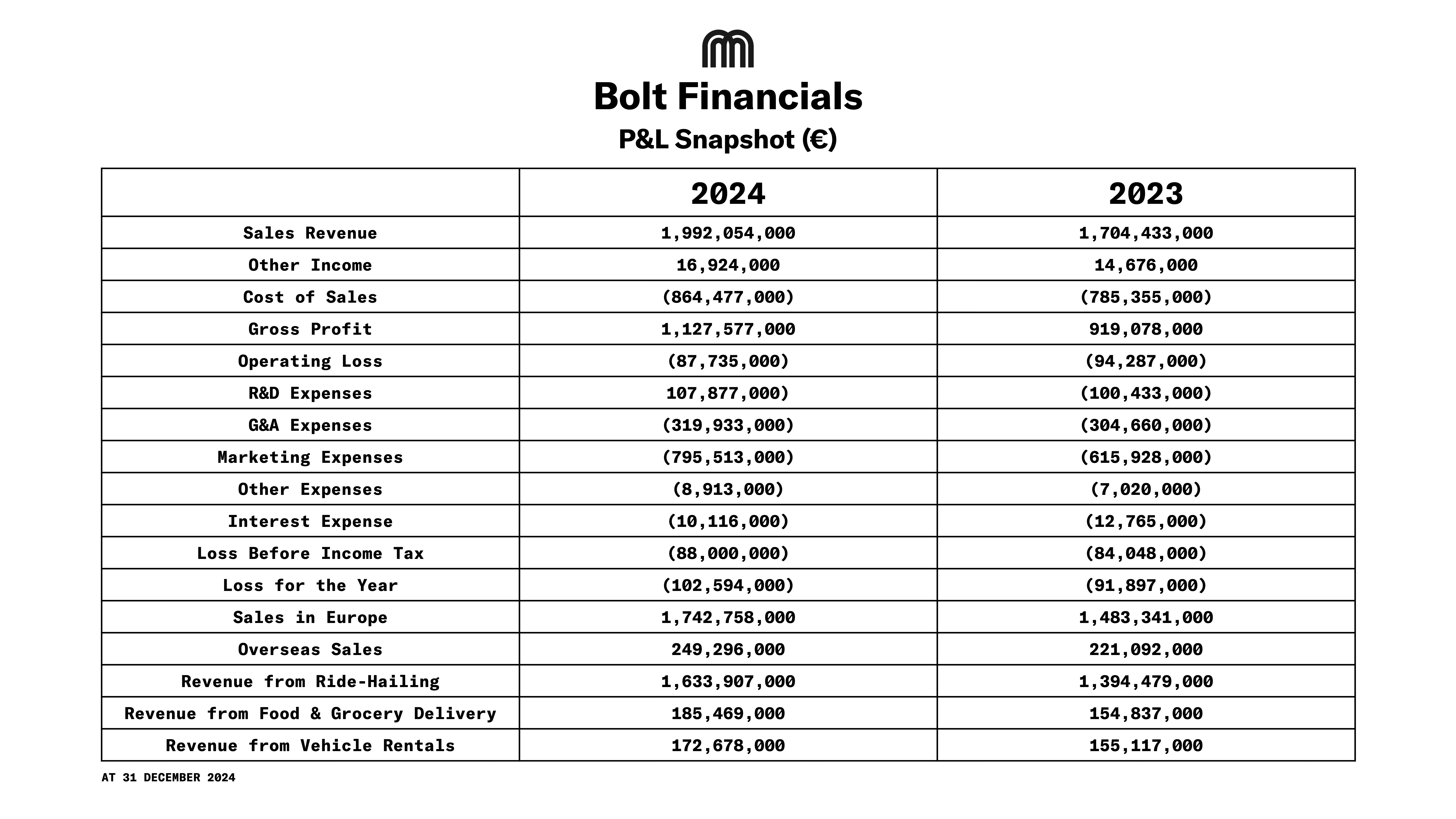

- Table: P&L Snapshot

- Cash Position & Balance Sheet

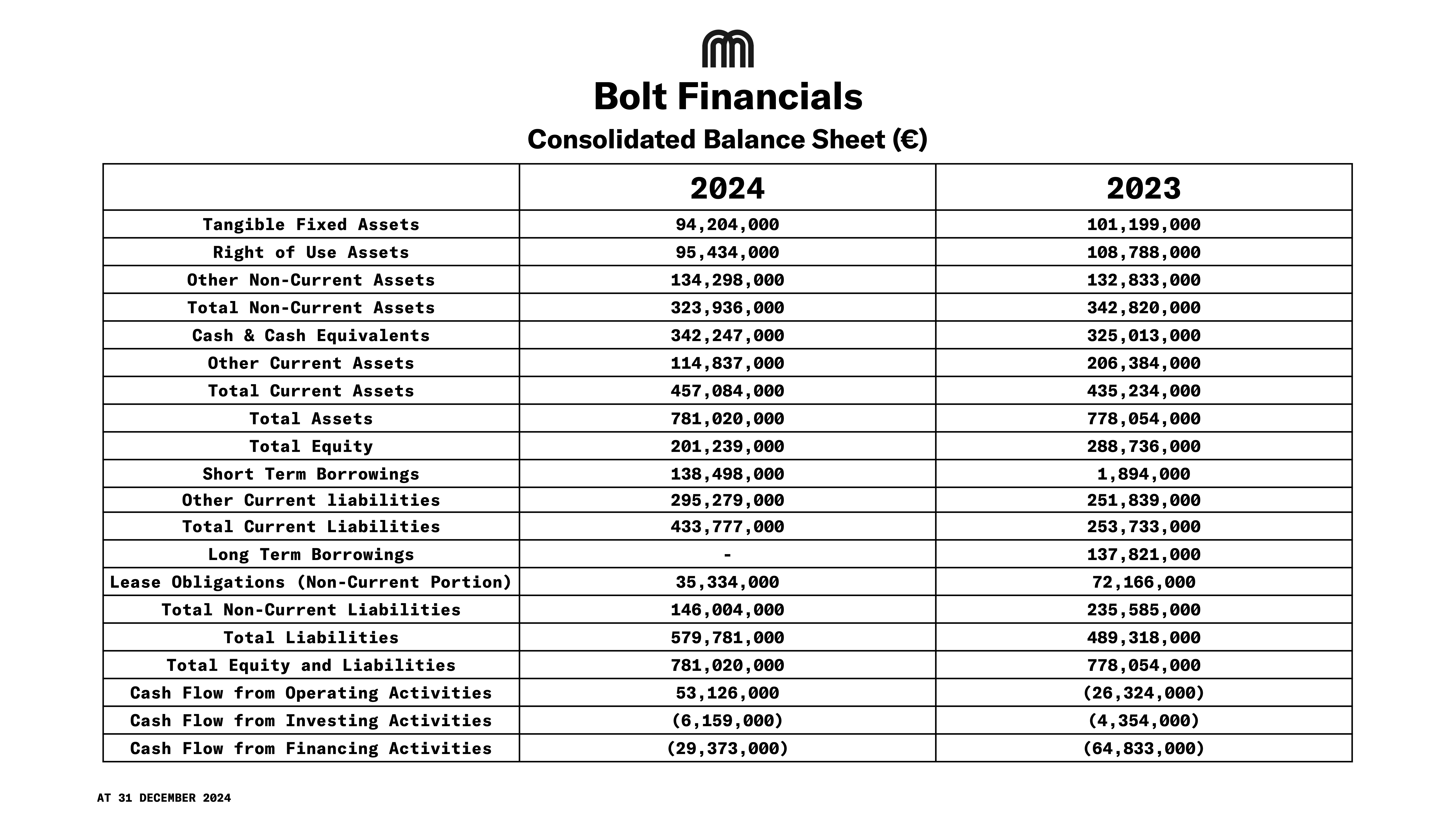

- Table: Balance Sheet Snapshot

- Conclusion

About Bolt

Bolt is a global shared mobility company offering ride-hailing, e-scooter and bike rentals, car sharing, and food delivery in more than 45 countries and 600 cities. The company employs over 4,000 people. In January 2025, it launched 720 Hopp shared e-scooters in Washington, D.C., followed in February by the rollout of ride-hailing services in Canada’s Toronto region. Bolt’s fleet includes around 250,000 rental vehicles, spanning cars, bikes, and e-scooters.

Globally, Bolt works with over 4.5 million registered drivers and courier partners across more than 45 countries.

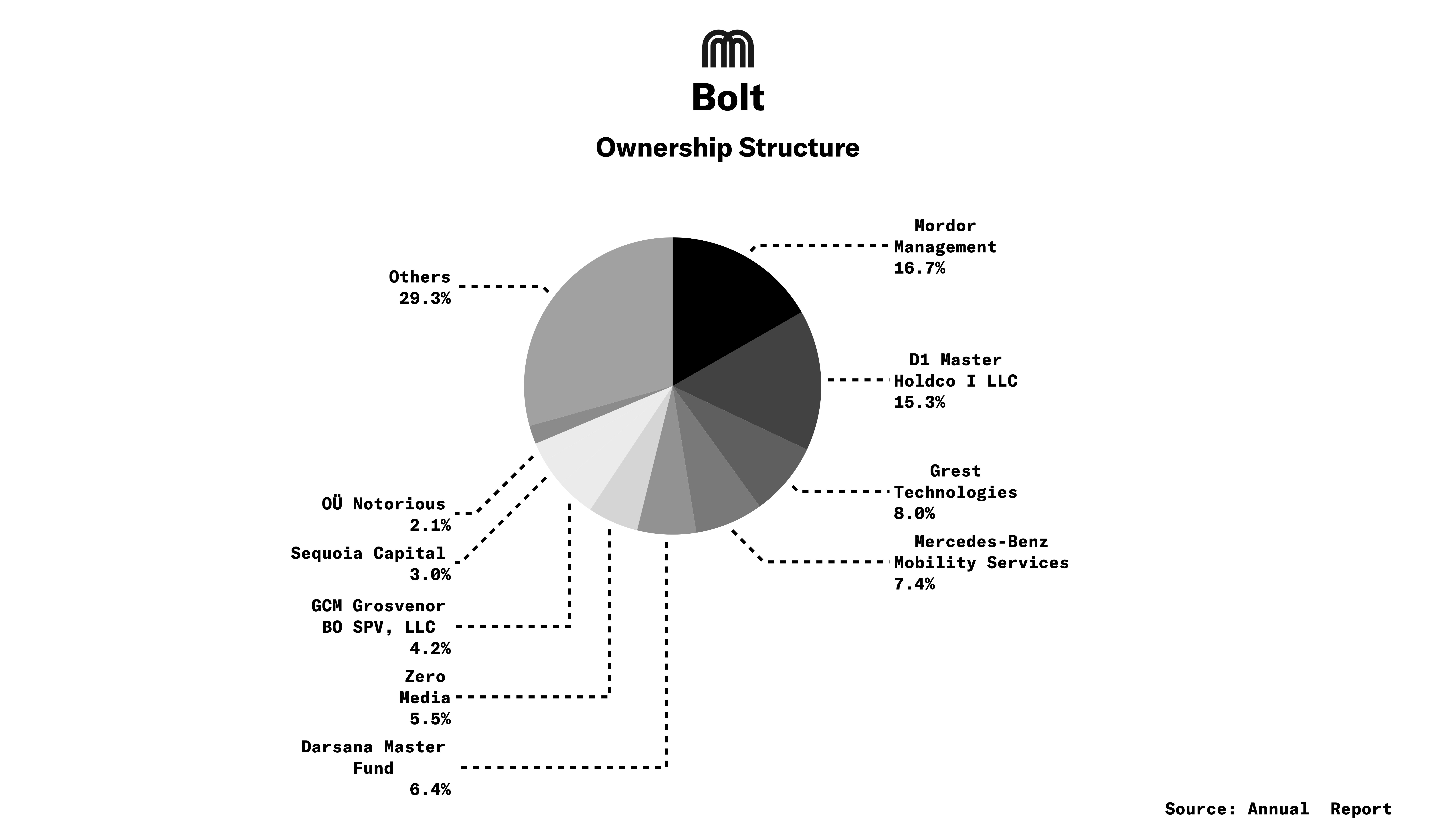

Ownership Structure

No single shareholder owns more than 25% of Bolt Technology OÜ. The largest stake belongs to Mordor Management OÜ, controlled by Markus Villig, which held 16.70% of shares at the end of 2024 (down slightly from 16.88% in 2023).

Sequoia Capital holds 3% of shares, under two different entities.

- Sequoia Capital Global Growth Fund III - U.S./India Annex Fund, L.P

- Sequoia Capital U.S. Growth Fund IX, L.P

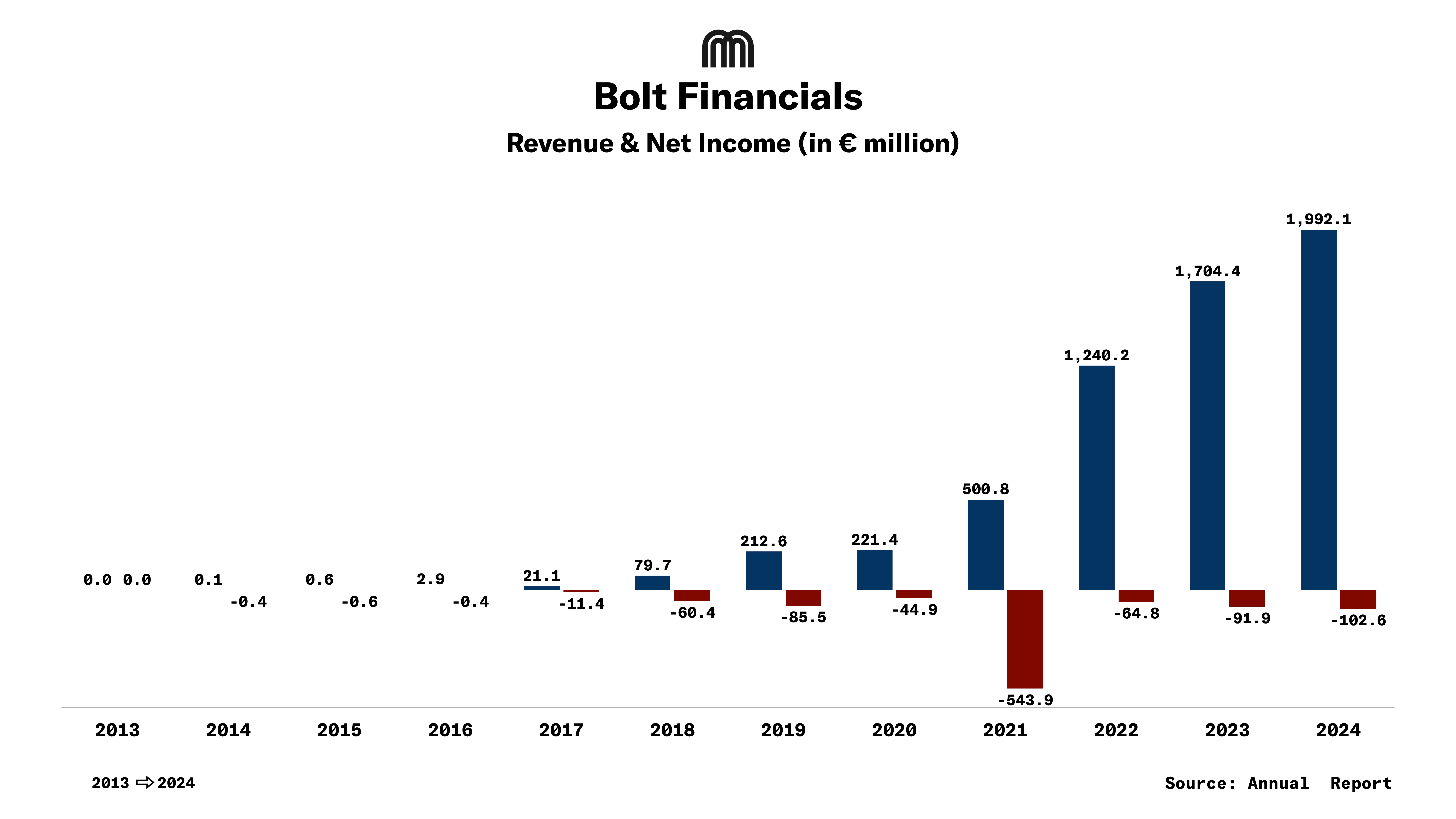

2024 Financial Performance

In 2024, Bolt generated €1.99B in revenue, up 17% from €1.7B in 2023 and posted a net loss of €102.59m, wider than the €91.9 net loss from 2023.

Operating Loss Margin improved to -4.4% from -5.5% in 2023.

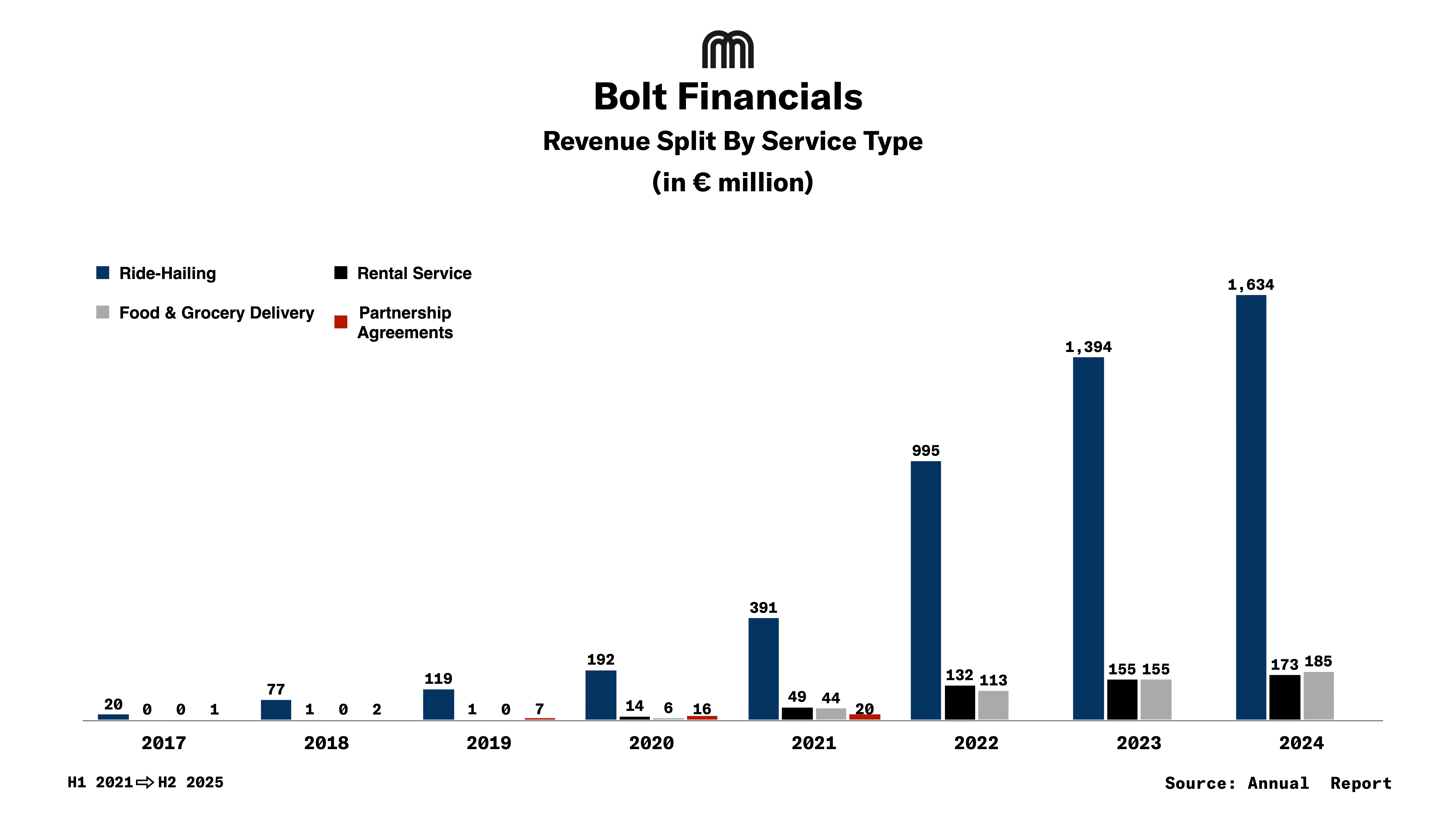

Revenue Split:

Ride-Hailing: €1.634B

Rental Services: €173m

Food & Grocery Delivery: €185m

Bolt earned 87% of its revenue from Europe. Regions such as North Africa, Southeast Asia, and the Middle East are growing significantly, particularly in the ride-hailing segment.

In 2024, ride-hailing revenue grew strongly, driven by demand in existing markets. The company also expanded services into new markets despite economic challenges in Africa and tough competition elsewhere. Key highlights included launches in the UAE, Switzerland, and Malaysia. In Dubai, a partnership with Dubai Taxi Corporation reached a milestone of 1 million rides in just 41 days.

In vehicle rentals, particularly micromobility, Bolt won tenders in Brussels, Milan, and Oslo, which helped it expand into new markets and strengthen its position in existing ones. Micromobility pass, introduced in 2023, gained strong traction, and nearly half of all trips are now made with a subscription, reducing costs and improving customer retention.

Though Bolt doesn’t give revenue split between micromobility and car rentals, it is safe to assume that their micromobility revenues are in the range of €120m to €150m which is roughly the size of Voi

Funds Raised

- In May 2024, Bolt Technology raised €220m ($236m), a syndicated revolving credit facility (RCF).

- The funding is supported by eight lenders: Barclays, BNP Paribas, Citi, Deutsche Bank, Goldman Sachs, JP Morgan, LHV Pank, and Luminor.

- Citi acted as the coordinating Bookrunner and Mandated Lead Arranger.

- This credit facility remains undrawn as of Dec 31, 2024, providing a crucial liquidity backstop.

In total, Bolt has raised over €1.75B ($1.98B) over 14 rounds.

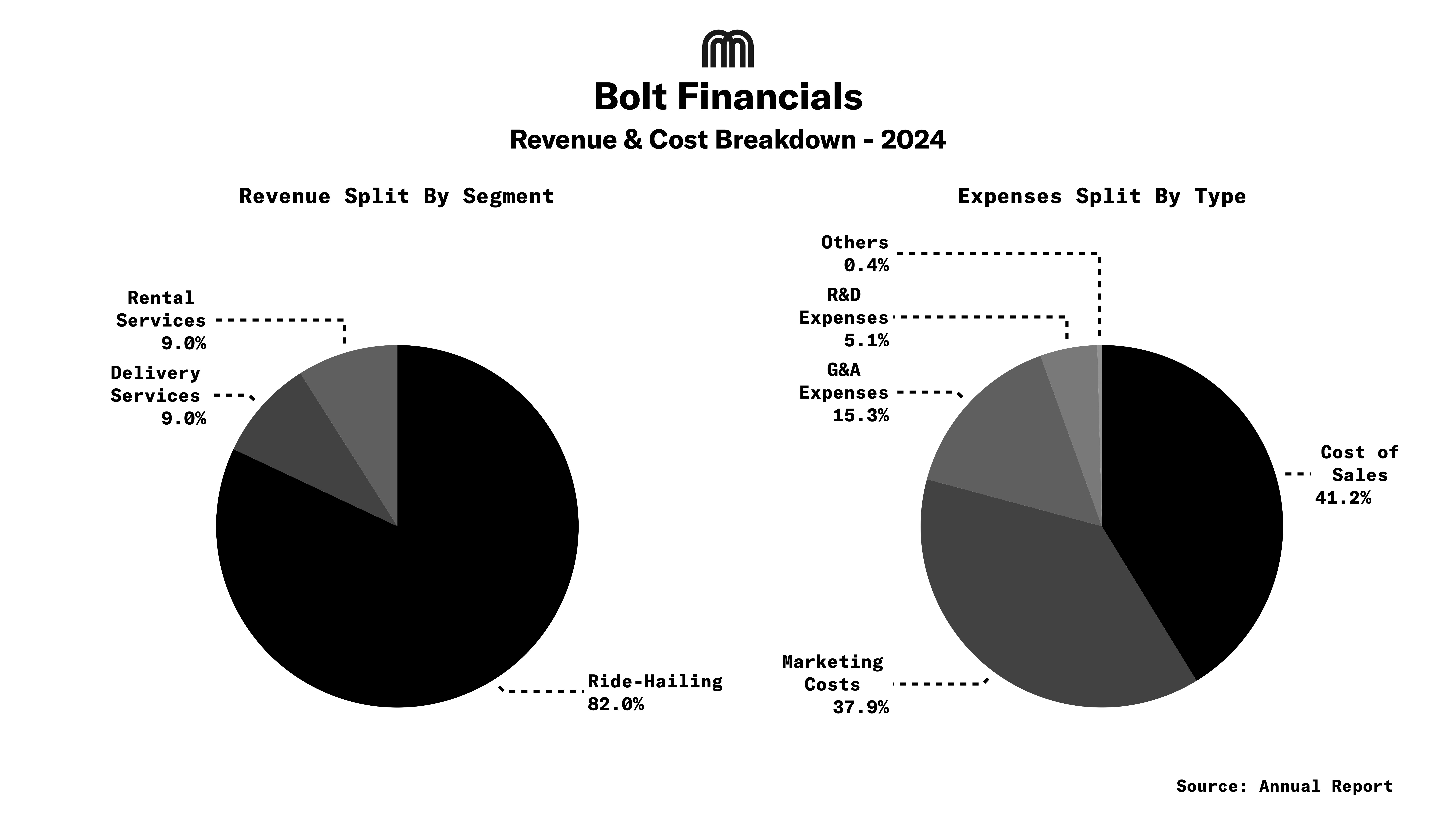

Cost Structure Breakdown

Bolt’s cost structure is dominated by marketing expenses. Overall expenses stood at €2B. Out of which, Selling expenses accounted for 41%.

Bolt’s cost of sales amounted to €864m in 2024, representing a 10% increase from €785m in 2023.

General and administrative (G&A) expenses rose to €319m, up by 5% year-on-year. These expenses accounted for 15% of overall costs, with the increase largely driven by a €102.9m provision for a potential legal settlement (see Risks).

Research and development (R&D) expenses reached €107m, a 7% increase compared to the previous year, making up 5% of total expenses. It is noteworthy that Bolt now expenses all software development costs immediately rather than capitalizing them, reflecting a more conservative accounting approach.

Marketing expenses climbed to €795m in 2024, up 29% from €615m in 2023. A significant portion of this spending was directed towards rewards and campaigns in newly entered markets. Marketing accounted for 38% of overall costs, making it the company’s second-largest expense category.

Bolt’s accumulated losses stand at ~€1B at the end of 2024.

Cash Position & Balance Sheet

Bolt’s cash reserves remained broadly in line with 2023 at €342m, reflecting a 5% year-on-year increase, although this was overshadowed by growing liabilities. Total assets were unchanged at €781m.

Liabilities surged 18.5% to €579m, up from €489m in 2023. These included:

- Short-term loan: €138.5m, due within a year. This is a convertible bond that was reclassified from long-term debt as it now matures on December 31, 2025, creating a significant liquidity requirement for the upcoming year.

- Lease obligations: Nearly €100m in 2024.

- Provisions: Increased sharply to €191.7m (from €99.1m in 2023), primarily due to the €102.9m provision for a potential UK driver liability case.

Equity fell to €201m, a 30% decline from 2023. Leverage also deteriorated, with the debt-to-equity ratio rising 70% from 1.69 to 2.88 in 2024, which signals heightened financial risk, particularly given the €138.5m in debt maturing by the end of 2025.

Bolt’s revenues and cash flow are not affected by market interest rate changes because its assets are primarily short-term deposits and fixed-rate securities. The group uses only fixed-rate instruments, which means it is not exposed to interest rate risk. A notable asset is a €102m tax deposit held with UK authorities (HMRC) in connection with an ongoing VAT dispute, which Bolt expects to recover.

Conclusion

In 2025, Bolt plans to continue its aggressive market expansion by introducing new rider services, launching additional categories, and extending vehicle financing programs to grow its fleet. Growth in shared micromobility is expected to come from securing more city tenders, while the car-sharing segment is positioned to benefit from expanded partnership models and improvements in both unit economics and overall profitability.

With an IPO on the horizon, holding onto the hardware-heavy micromobility and car rental businesses may not be the right focus, given that the majority of revenues come from its asset-light ride-hailing operations. On the car rental side, Bolt has onboarded all Miles cars, which aligns with this strategy of staying asset-light. In micromobility, there is an opportunity for Bolt to follow Uber’s path with Jump and Lime, and there are players in the market who would pursue such a deal if the price is right.

.png)