.svg)

%2Bcopy.avif)

.svg)

.webp)

.webp)

Welcome to Micromobility Pro, a bi-weekly publication which is part of The Micromobility Newsletter, where we deep-dive into the financials of micromobility companies and share exclusive insights tailored for professionals and members.

Join the leaders in micromobility. Get an annual subscription today to access the members-only Slack, event ticket discounts, and the full Micromobility Pro content library.

Showcase Your Brand at Micromobility America – Jan 14–15, 2026, San Francisco

Join the leading event for small electric vehicles, shared mobility, and retail opportunities in the US market.

Exhibiting and sponsorship packages put your products in front of industry leaders, innovators, and decision-makers with year-round visibility across the world’s largest micromobility media network.

Early Bird rates end on September 1st - secure your spot now!

Book a Meeting or Fill out the interest form

🎤 Want to speak? Apply here

🎟 Super Early Bird Tickets - Just $1500 $249

Very few tickets left at this price - prices rise once these sell out.

Contents

- About Swing

- Ownership Structure

- 2024 Financial Performance

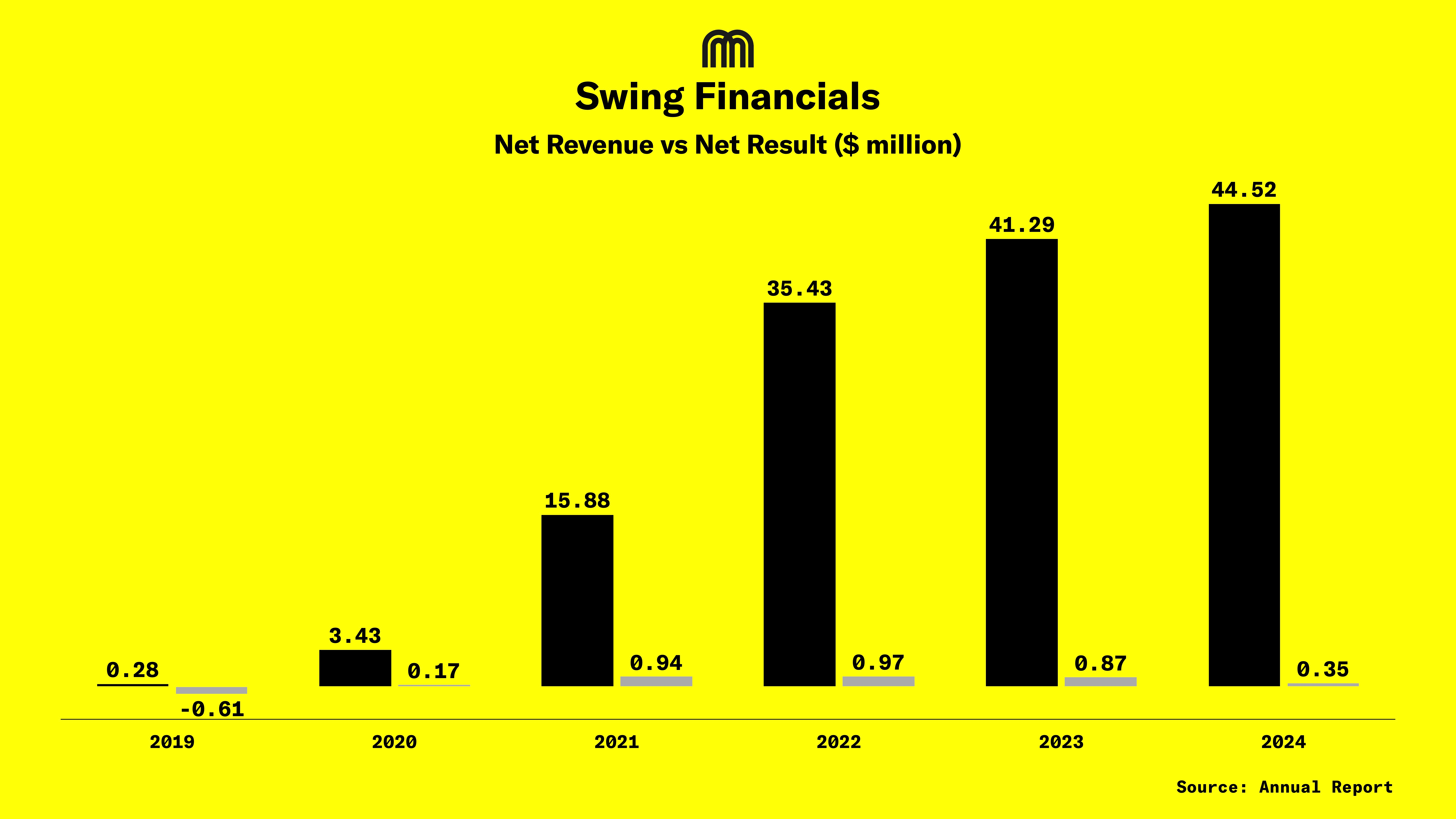

- Chart: Net Revenue vs Net Result ( 2019 to 2024)

- Revenue Breakdown

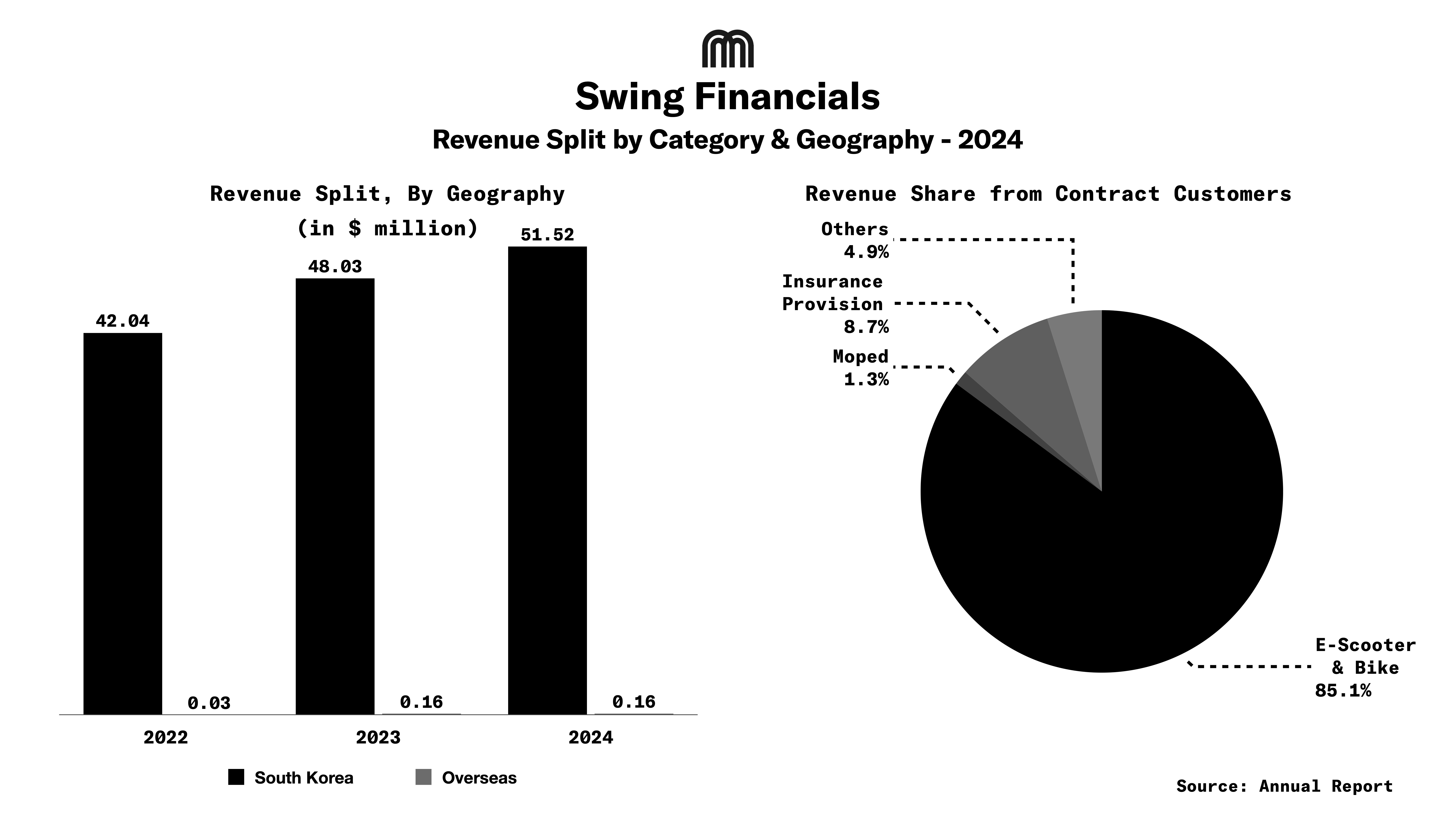

- Chart: Revenue Split by Geography and Category

- Cost Structure

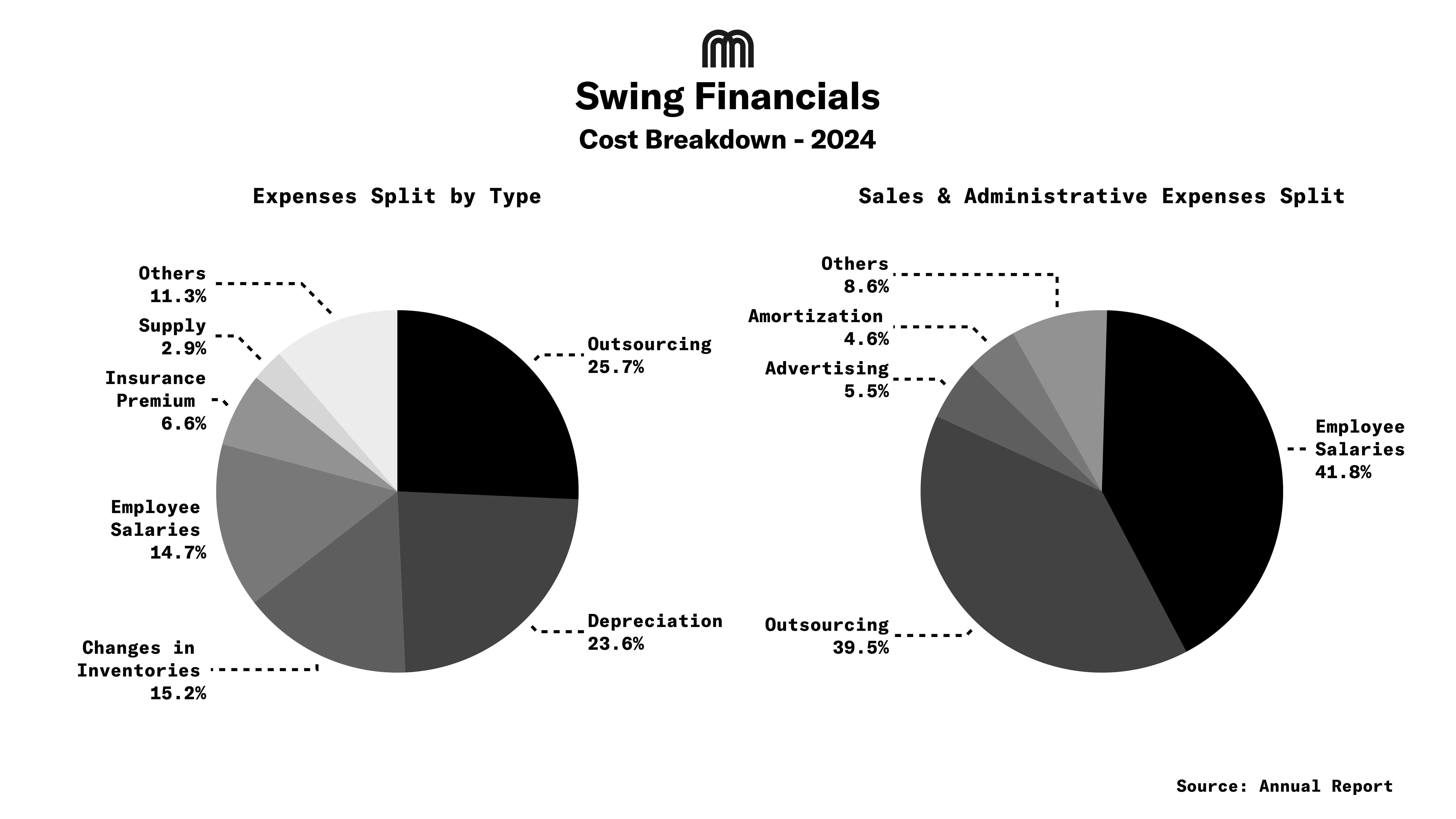

- Chart: Cost Breakdown

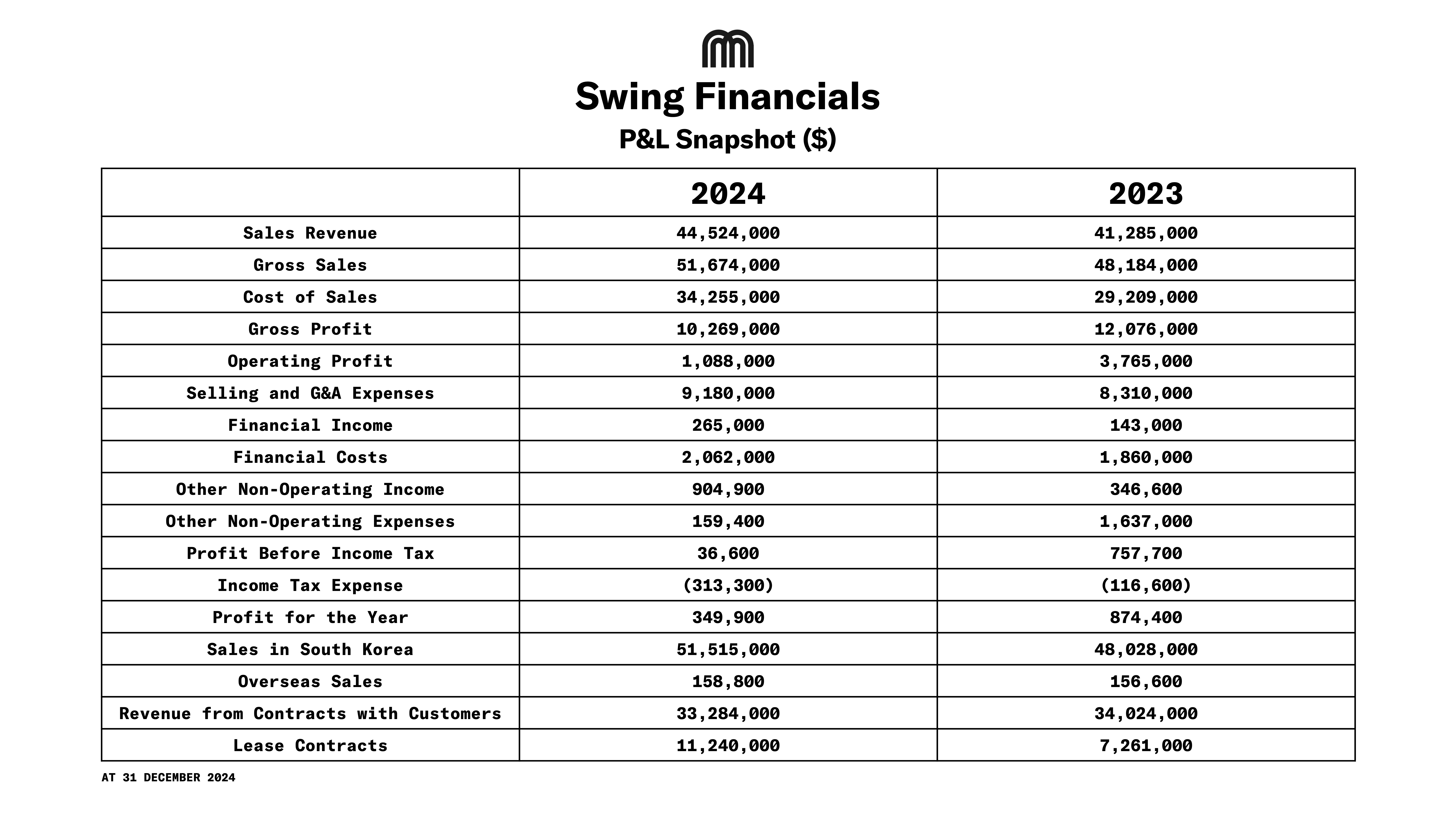

- Table: P&L Snapshot

- Cash Position & Balance Sheet

- Balance Sheet Snapshot

- Strengths & Challenges

- Major Developments (2022–2025)

- 2025 Outlook

- Conclusion

About Swing

Swing Co., Ltd. is a South Korean micromobility company operating shared bicycles, scooters, motorcycles, and kickboards through an integrated online platform. Beyond rentals, Swing develops proprietary fleet management software, licenses mobility technology, and offers insurance products tailored to shared mobility.

The company operates in both domestic and overseas markets, notably Japan through its subsidiary Swing Japan.

Checkout this panel from Micromobility Europe 2024, moderated by Micromobility Industries CEO Prabin Joel Jones, where Swing’s founder San spoke about how Swing has remained profitable

Ownership Structure

As of 31 December 2024, CEO Kim Hyeong-san and affiliated entities own 26.17% of the company. Other major investors include Hashed Ventures (15.69%) and White Star Capital (10.34%). Swing has 52,786 issued shares, comprising 18,817 common and 33,969 preferred shares.

Swing has issued two types of convertible preferred shares:

- Type 1: 3,227 shares at $250 each, total $0.81M

- Type 2: 11,712 shares at $228 each, total $2.66M

Both mature 10 years after issuance.

2024 Financial Performance

Swing closed 2024 with revenue of $44.5M, up 12.5% from 2023. However, profitability weakened sharply: operating profit fell nearly 70% to $1.1M, while net income declined 58% to $0.35M.

Gross margin compressed to 23.1% from 29.2%, reflecting higher fleet maintenance, depreciation, and financing costs. The company ended the year with a debt-to-equity ratio of 124%, up from 77% in 2023.

Service sales grew to $32.1M, while product sales fell sharply to $1.2M from $4.1M in 2023. Gross profit decreased 11.3% to $10.3M as cost of sales outpaced revenue growth, rising 22.4% to $34.3M.

SG&A expenses increased 15.3% to $9.2M, driven by marketing and R&D, while finance costs climbed 15.7% to $2.1Mdue to higher borrowing.

Revenue Breakdown

Domestic sales contributed $51.51M in 2024, while overseas revenue, primarily from Japan, totaled $0.16M. A domestic sales adjustment reduced reported revenue by $7.14M. No single customer represented more than 10% of total revenue.

Cost Structure

Fleet-related expenses accounted for over 70% of revenue, with depreciation at $10.3M. Inventory write-downs totaled $6.6M.

SG&A spending was led by salaries (42% of SG&A) and included $1.5M in bad debt provisions. Stock-based compensation declined 27.4% to $0.24M. Interest expenses reached $1.9M.

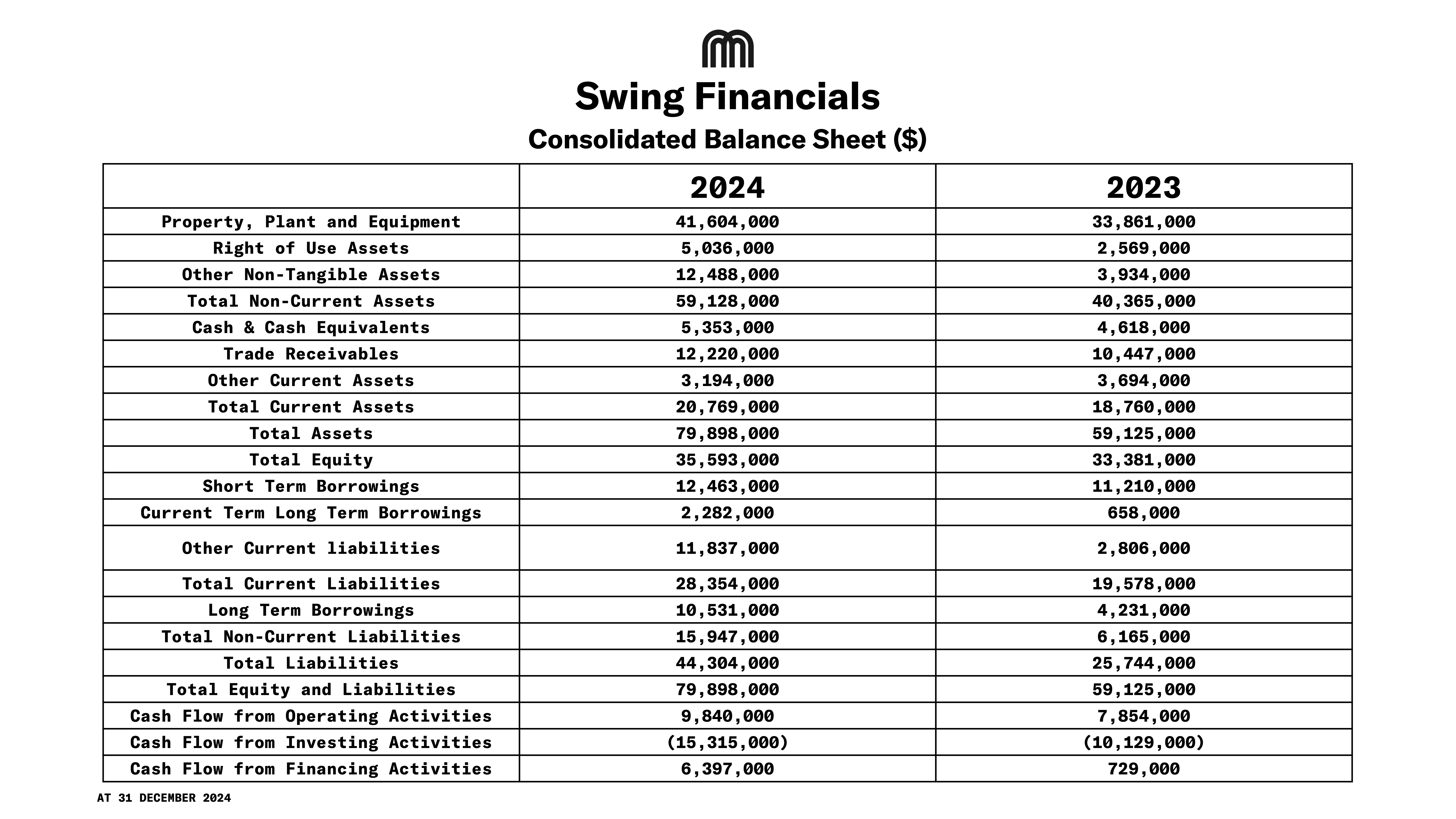

Cash Position & Balance Sheet

Swing’s cash reserves increased 21% to $5.4M, but total liabilities rose 79% to $44.3M. Short-term borrowings climbed to $12.5M and long-term debt to $10.5M, with $29.7M in debt maturing in 2025.

Total assets grew 42.1% to $80.5M, driven by acquisitions and fleet expansion.

By acquisition cost, e-scooters remain the largest category at $38.16M, followed by e-bikes at $21.80M and e-mopeds at $4.05M.

E-bikes saw the sharpest investment increase, with book value rising to $17.56M (from $8.09M in 2023). Scooters’ book value fell to $15.84M, and mopeds to $2.28M.

Strengths & Challenges

Strengths

- Market leader in Korea

- Diversified fleet and service offerings

- Proprietary technology platform

- Strong institutional investor base

Challenges

- Margin erosion despite revenue growth

- High leverage and refinancing risk

- Integration and performance issues at subsidiaries

Major Developments (2022–2025)

- 2022: Raised $25M in Series B funding, launched in Japan, and expanded fleet to ~35,000 EVs.

- 2023: Abandoned planned acquisition of VCNC (TADA) due to integration cost concerns.

- 2024: Launched SWAP (e-bike subscriptions) and Swing Taxi; fleet surpassed 90,000 scooters and 30,000 e-bikes.

- 2025: Acquired Rever Lab (“Yellow Bus” school shuttle service); H1 revenue up 70% YoY, with 92% of growth from new business lines.

2025 Outlook

Key priorities for 2025 include:

- Refinancing $29.7M in maturing debt

- Restoring gross margin through tighter cost control

- Fully integrating Rever Lab and monetizing new services without operational strain

Conclusion

Swing is one of the few players in global micromobility to have achieved profitability early, reporting net profits as far back as 2022. Its strong unit economics, dominant position in the Korean market and proprietary technology platform have provided a solid foundation for growth.

In 2024, the company accelerated diversification, launching new business models such as SWAP (contract-free e-bike subscriptions) and moving into verticals including taxi dispatch and school shuttle services. These initiatives expand Swing’s addressable market and create multiple revenue streams beyond core rentals.

However, this expansion has come at a cost. Revenue grew to $44.5M, but operating profit fell 70% and net income dropped 58% due to higher fleet, SG&A and financing expenses. Leverage has risen sharply with $29.7M in debt maturing in 2025.

The challenge for 2025 is to show that these new verticals can strengthen rather than dilute Swing’s historically disciplined approach to profitability. Success could position Swing as a diversified and cash-generative mobility platform, while failure could stretch both operations and the balance sheet.

.png)