.svg)

%2Bcopy.avif)

.svg)

.jpg)

%20(1).jpeg)

.jpg)

.webp)

Welcome to Micromobility Pro, a bi-weekly publication which is part of The Micromobility Newsletter, where we deep-dive into the financials of micromobility companies and share exclusive insights tailored for professionals and members.

Contents

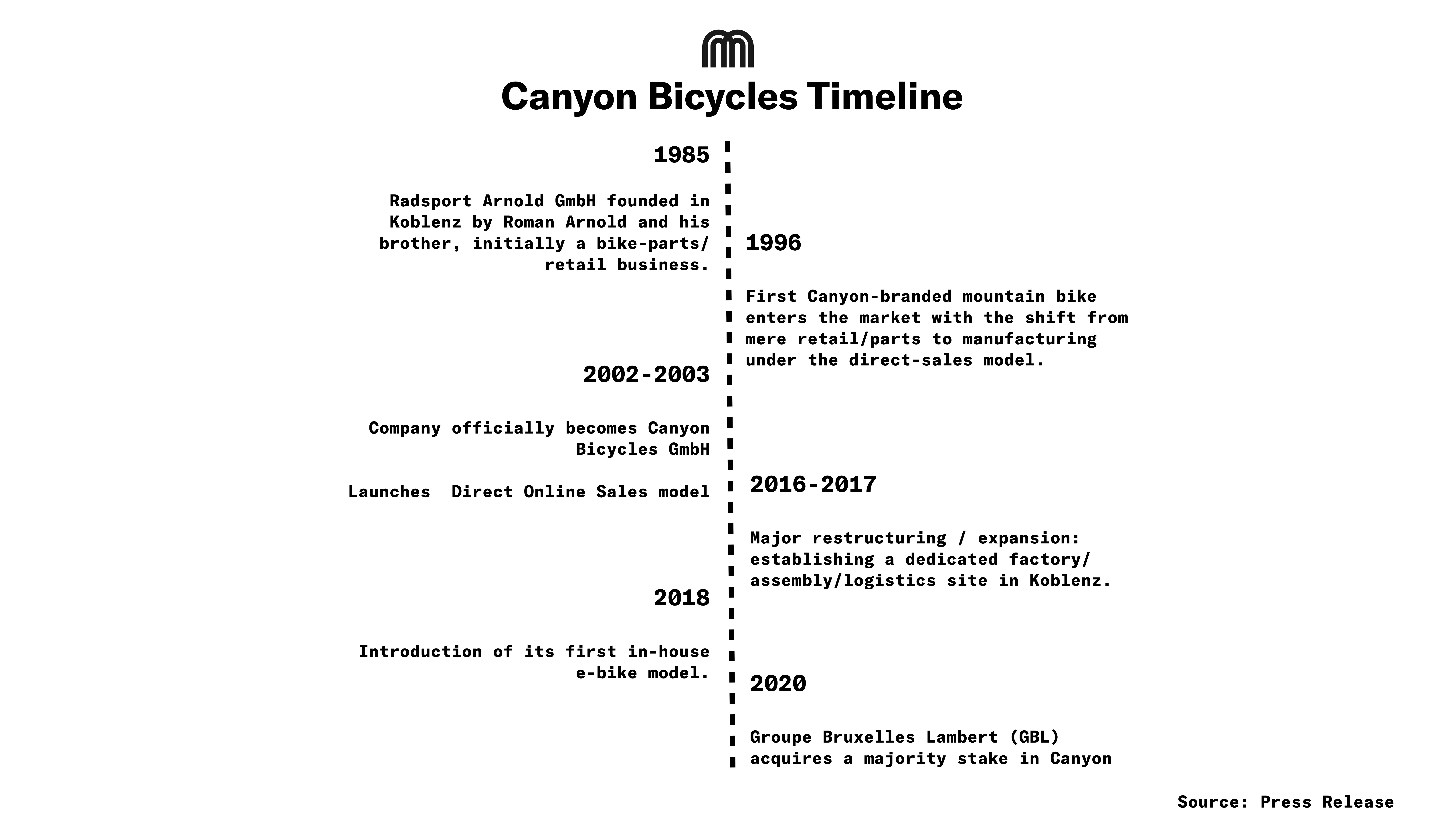

- History: From Humble Beginnings to a Global Brand

- Chart: History of Canyon Bikes

- GBL Acquisition

- 2024 & H1 2025 Performance

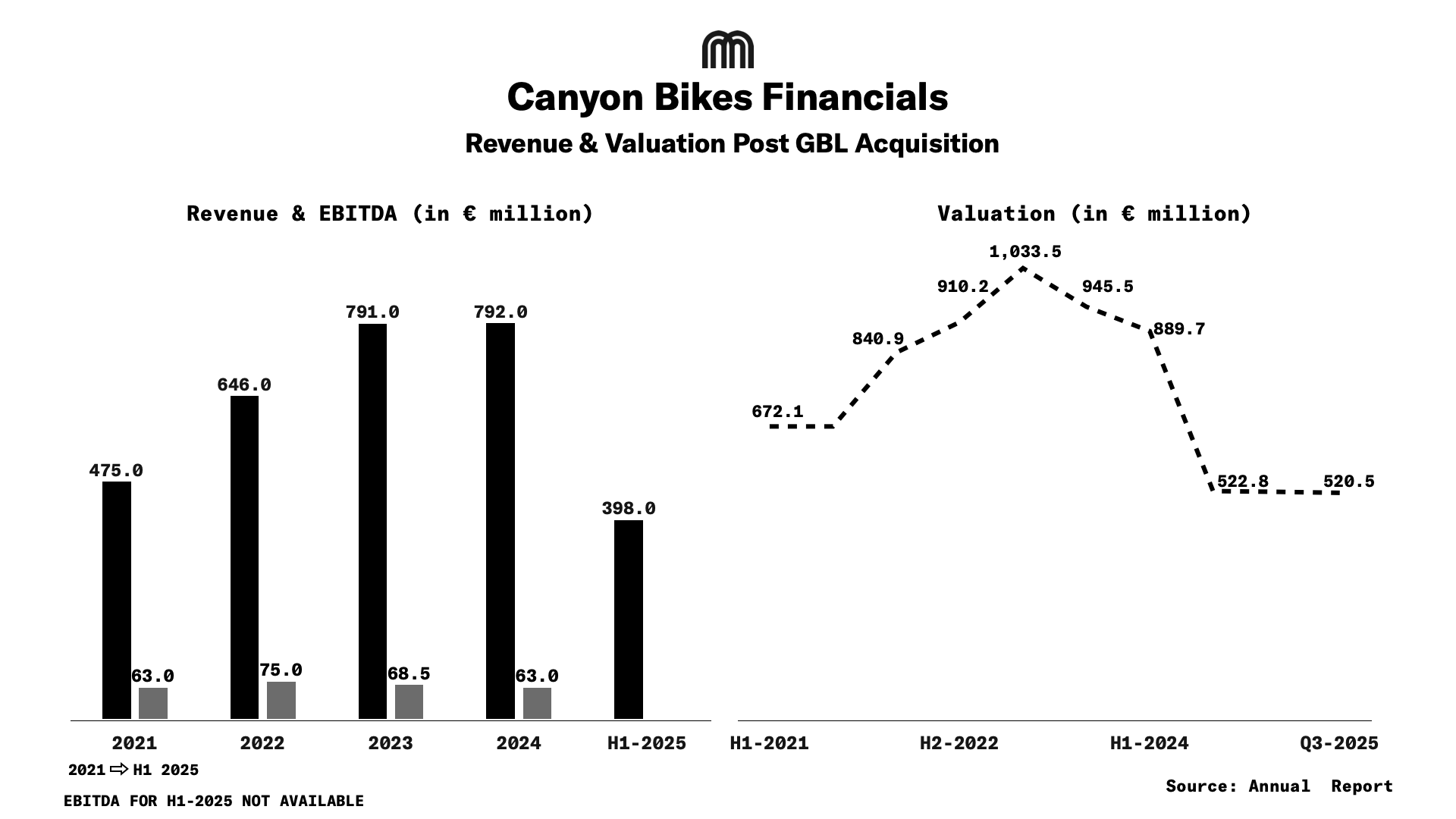

- Chart: Revenue, EBITDA & Market Valuation Chart

- Canyon Group 2020 - 2021 Financials

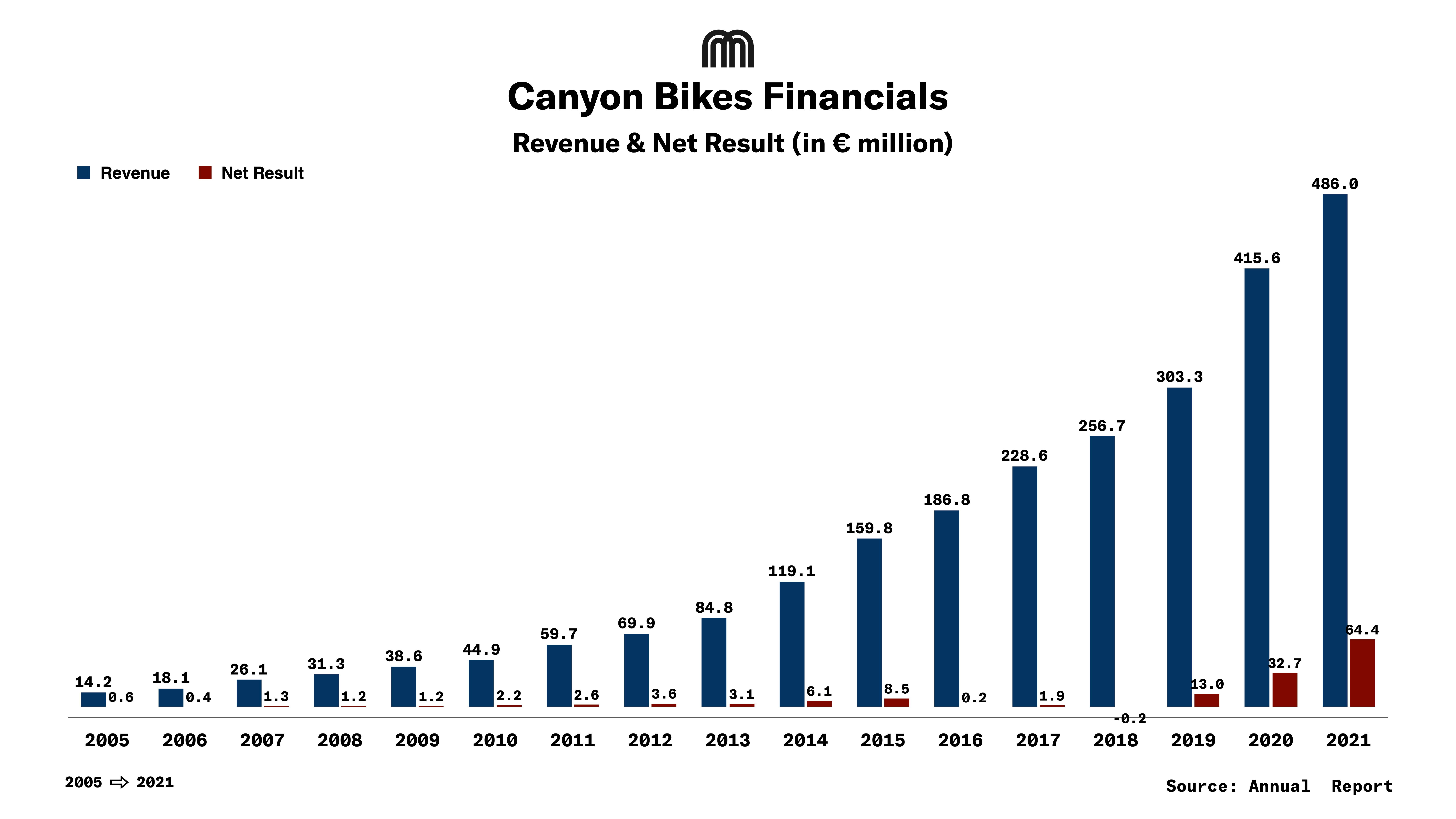

- Chart: Sales Revenue vs Net Income (2005-2021)

- The Pandemic’s Impact on Performance and Strategy

- Cash Flow & Inventory (2020-2021)

- Liability Structure & Bank Debt

- Canyon Bicycles Standalone Company Financials 2022 & 2023

- Conclusion

History: From Humble Beginnings to a Global Brand

Founded in Koblenz, Germany, Canyon began in the 1980s as a small bike parts operation run by Roman Arnold, before evolving into a manufacturer known for precision-engineered performance bikes. The company built its reputation in road racing and mountain biking, later expanding successfully into gravel and e-bike categories.

A defining pillar of Canyon’s growth has been its direct-to-consumer (D2C) online model, allowing it to offer premium, competition-level bicycles at sharper price points than traditional dealer-based brands. Over time, Canyon has become one of the most influential modern bike brands globally, backed by world-class athletes, innovative product design, and a digitally-driven customer experience.

GBL Acquisition

In December 2020, Groupe Bruxelles Lambert (GBL) signed a definitive agreement to acquire a majority stake of roughly 50% in Canyon for €400m. As part of the transaction, GBL acquired the interest held by private equity firm TSG Consumer Partners, which fully exited its position. Founder Roman Arnold remained a significant shareholder and reinvested a large part of his proceeds alongside GBL.

Roman Arnold continued in the business, serving as Chairman of the Advisory Board rather than CEO.

At the time of signing, Canyon had grown to over €400m in sales (pre-deal) with an average annual growth rate of ~25% over the prior seven years.

2024 & H1 2025 Performance

Canyon’s performance softened in 2024 and into H1 2025 as the wider cycling sector faced oversupply and widespread discounting, particularly in mountain and urban bikes. Revenue was €792m, and it reported a net loss of €38m. In 2024, Canyon carried inventory valued at approximately €417.9m at the start of the year, which was reduced to about €351.6m by year-end. Performance was further impacted by quality issues in select e-MTB models, leading to a temporary suspension of sales, with resolution initiated in Q2 2025.

In H1-2025, Canyon generated revenue of €398m, a 5% drop compared to H1-2024 of €419m. Canyon’s H1 2025 results were weighed down by continued oversupply and heavy discounting, particularly in e-MTB and urban bikes, while road and gravel performance stayed solid. Europe remained strong, but demand softened in the U.S. and Asia amid tariff uncertainty. The temporary suspension of select e-MTB models following late-2024 quality issues also impacted revenue and profitability.

EBITDA in 2023 was impacted by higher discounts on certain categories, particularly non-electric mountain bikes, due to oversupply in the market as well as a strong comparable period for Canyon, which had benefited from the sale of high-margin models. Meanwhile, in 2024 & H1-2025, EBITDA has been impacted by aggressive discounting, especially in electric and non-electric mountain and urban bikes.

The parent company GBL’s fair value of the investment was around €460m at the end of 2023, and this was marked down to about €267m as of September 2025. GBL held a 51.3% stake in the company as of September 2025.

Thus, the overall valuation of Canyon has dropped from €1.03B in June 2023 to €520.5m as of September 2025. GBL attributed the markdown to the industry context (discounting pressure) and a one-off quality issue impacting certain e-MTB models.

Canyon Group 2020 - 2021 Financials

Canyon’s consolidated revenues jumped from €416m in 2020 to €486m in 2021 (+17%). Net profit after tax doubled, from €32.7m to €64.4m, while operating cash flow stayed strong (≈€40m in 2020, €38m in 2021). However, the strong topline performance was accompanied by a significant increase in inventory and a notable decline in liquidity, with inventories rising from €131m to €199m while cash balances fell from €43.5m to €12.8m.

The Pandemic’s Impact on Performance and Strategy

Demand Surge and Supply Leverage: The pandemic created an unprecedented global spike in cycling demand. Canyon, already a D2C specialist, capitalized on this to grow revenue strongly in 2020 and again in 2021.

Profitability Expanded: Net profit almost doubled in 2021 versus 2020. The company maintained a healthy gross margin of ~41%, and operating leverage combined with a good product mix, including higher-value e-bikes, which lifted the bottom line.

Cash used by Working Capital: To meet surging demand and manage supply chain volatility, Canyon built inventory, which was up by €68m between 2020 and 2021. Cash on hand fell accordingly, even though operating cash flows were robust, because cash was redeployed into inventory and possibly pre-purchases and logistics.

Balance Sheet Shift due to External Financing and Equity. Equity grew sharply (reflecting retained profits and the GBL ownership/transaction impact), while bank debt fell, indicating a balance-sheet strengthening even as liquidity decreased.

Cash Flow & Inventory (2020-2021)

- Canyon produced strong operating cash flow (€38–40m) in both years, evidence of cash generative operations at the income statement level.

- But cash balances fell from €43.5m to €12.8m because the company built up stock, and inventory became a working-capital sink. The inventory build could reflect:

- Intentional bulk purchasing to beat component shortages and freight cost inflation;

- Prepared stock for new e-bike ramps and market expansion;

- Logistical buffering to maintain lead times in a constrained global supply chain.

Liability Structure & Bank Debt

- The drop in liabilities to banks/credit institutions from €49.8m to €31.9m is significant, −36%. This suggests Canyon paid down or refinanced bank debt in 2021.

- However, total liabilities moved only slightly, from €110.7m to €113.2m. That implies other liability categories (payables, provisions, other financial obligations) likely increased or stayed steady while bank debt decreased.

- The absolute level of liabilities €113m, relative to assets €274m, giving a liabilities-to-assets ratio of 41%. That is moderate; roughly speaking, 59% of assets are funded by equity as of 2021.

Asset Profile

Fixed (non-current) assets moved from €17.7m to €20.3m, showing continued investment in production capacity, equipment, or property.

- Within that, tangible assets rose from €9.4m to €12.5m; “other equipment/plant/business equipment” rose €8.6m to €11.3m. This indicates Canyon is scaling its tangible asset base substantially in 2021, likely to support increased production, perhaps e-bike volumes, logistics, etc.

- Current assets are dominated by inventory and cash. Inventory surged to €199m, while cash fell from €43.5m to €12.8m. This shift implies that a large part of the asset base is tied up in working capital (inventory) rather than easily liquid assets.

With €199m of inventory in FY2021, which is about 73% of total assets, the operating model is working at a high-capital-intensity level in terms of stock.

Canyon Bicycles GmbH Standalone Company Financials 2022 & 2023

Canyon Bicycles GmbH recorded a strong increase in sales, rising from €577.7m in 2022 to €677.2m in 2023, a growth of 17%. The company continued to benefit from its direct-to-consumer model and strong brand recognition in performance bikes and e-bikes.

However, profitability weakened significantly. Material costs increased by 45%, outpacing sales growth, while operating expenses also rose. As a result, gross profit declined from €220.7m to €158.7m, and margins compressed sharply. Higher input prices, logistics costs, and discounting to clear inventory contributed to this erosion.

Fixed assets increased from €38.4m in 2022 to €47.5m in 2023, primarily due to growth in intangible assets such as software, proprietary technologies, and licenses. Tangible assets slightly declined from €17.5m to €16.2m.

Conclusion

Canyon’s trajectory reflects a high-growth performance brand navigating the post-pandemic normalization of the global bike market. Demand for premium road and gravel bikes remains strong, and brand equity continues to be reinforced by elite athlete victories, strong industrial design, and award-winning product launches. However, working capital pressure, e-MTB recall disruption, and aggressive sector-wide discounting have weighed on EBITDA and valuation.

.png)