.svg)

%2Bcopy.avif)

.svg)

.jpg)

%20(1).jpeg)

.jpg)

.webp)

With cycling demand shifting, Shimano’s results show both strengths and challenges.

Component manufacturer Shimano points to a mixed performance in its core bicycle division over the first three quarters of 2025. While net sales showed steady growth, profitability faced significant headwinds from higher costs and foreign exchange losses.

Growth vs. Profitability

For the first three quarters of 2025, the bicycle components segment recorded net sales of €1.6B, around 5% increase compared to the same period last year.

However, this sales growth did not translate into higher profits. Operating income for the segment fell 27.0% year-on-year to approximately €181M.

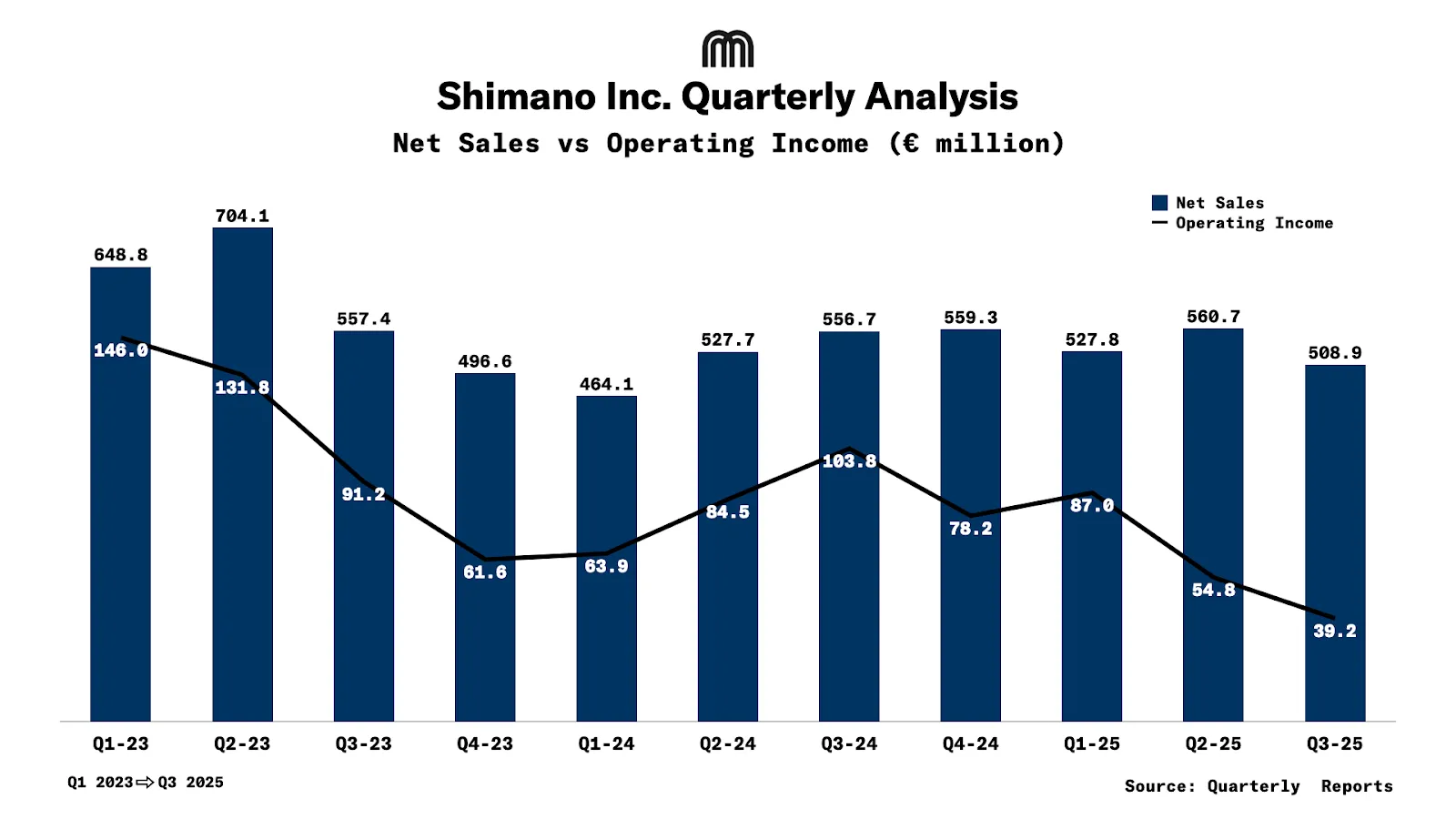

A Closer Look at the Quarters

A quarterly breakdown shows a consistent downward trend in profitability through the years.

After an improvement in Q2, net sales declined from €560.7 million to €508.9 million in the third quarter. Meanwhile, profitability fell at a much steeper rate; operating income plummeted from €87.0 million in Q1 to just €39.2 million in Q3.

Regional Market Dynamics

Shimano's report reveals a nuanced inventory landscape across its key global markets. While consumer demand persists, stock levels present a varied challenge. In Europe, stable weather helped maintain solid retail sales of complete bicycles. Despite this healthy demand, the company noted that inventory in the channel remains elevated. The situation is more pronounced in China, where interest in cycling as a sport has gone down, resulting in too many bicycles remaining unsold.

In Shimano's home market of Japan, steep price increases have dampened consumer spending, causing retail sales to slow. However, inventory levels there are reported to be under control.

Other regions, including Asia, Central, and South America, experienced softer consumer sentiment and weaker sales. A silver lining in these areas was a general improvement in inventory levels, bringing them down to more appropriate amounts. Across the Atlantic, the North American market felt the weight of economic uncertainty, leading to sluggish retail sales. Here, as in Japan, market inventories were successfully managed and kept at suitable levels.

This cautious global outlook was reflected in Shimano's summary of the economic climate, which cited worldwide trade policy shifts and heightened geopolitical tensions as reasons for a restrained forecast.

Product Innovation

Amid the financial pressures, Shimano continues to bet on technological innovation. The company highlighted strong market reception for its flagship mountain bike groupsets like XTR, DEORE XT, and DEORE.

One of the big new products this year was the Q’Auto, an automatic gear system that doesn’t need a battery. By using a dynamo in the rear hub to generate and store power, the system eliminates the need for a separate battery. It uses pre-set algorithms and learns from a rider's manual shifts to personalize gear changes. Initially aimed at urban and gravel bikes, this technology represents a significant step in bringing e-bike-like convenience to non-e-bikes.

Compliance Issue in Home Market

The company also faced a regulatory challenge in its home market. In September 2025, Shimano received a recommendation from the Japan Fair Trade Commission for violating the Subcontract Act.

The Commission determined that Shimano had unjustly required 121 subcontractors to store 4,313 company-owned molds and equipment free of charge, even when no production orders were placed for an extended period. Shimano has apologized and is in the process of compensating the affected suppliers. The company has stated that while the final payment amount is not yet settled, it is expected to be "relatively modest." This expense was not separately detailed in the recent financial report.

Overall Outlook

Shimano's profits took a big hit this year, mainly from a huge loss on foreign exchange. The company lost €110M because of currency changes, which is more than double what it lost last year.

Even with this problem, Shimano is not changing its forecast for the full year. It still expects a small 2% sales increase, but predicts a 29% drop in operating profit and a 60% drop in net income for 2025.