.svg)

%2Bcopy.avif)

.svg)

.webp)

.webp)

.jpg)

A post-pandemic inventory oversupply, combined with rapidly rising import tariffs, is putting serious pressure on bike manufacturers. These added duties, including reciprocal rates plus Section 301 and new Section 232 taxes, are creating an increasingly unstable environment for bike and component makers.

Previous Tariff Landscape

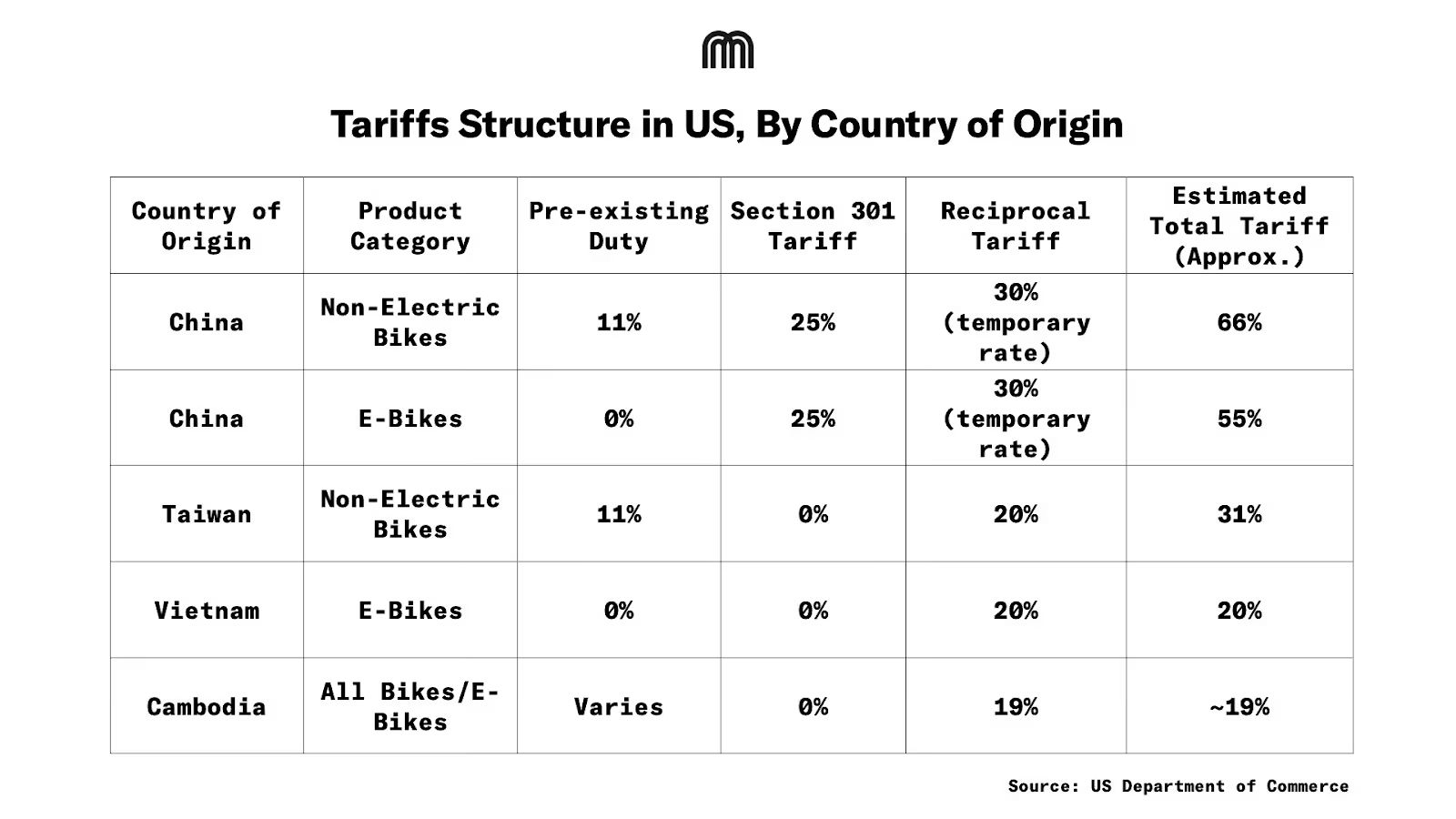

Before the implementation of the recent reciprocal tariffs and the discussion around Section 232 tariffs on aluminum and steel, the primary tariff burden on U.S. bike importers from China came from a combination of standard duties and Section 301 tariffs.

- Pre-existing Duty: Non-electric bikes from China were subject to a standard duty of approximately 11%, while e-bikes generally faced a pre-existing duty of 0%.

- Section 301 Tariff: Following trade actions initiated in 2018, bicycles, e-bikes, and many related components imported from China were subject to an additional 25% duty under Section 301 of the Trade Act of 1974.

As a result, before the most recent changes, the total tariff rate on Chinese-origin goods was already high, reaching 36% for conventional bikes and 25% for e-bikes. Certain product categories had secured exclusions from the Section 301 duties, but these exclusions were subject to expiration.

Current Tariff Landscape

The current tariff structure is complex, involving multiple stacked duties that vary significantly by country of origin.

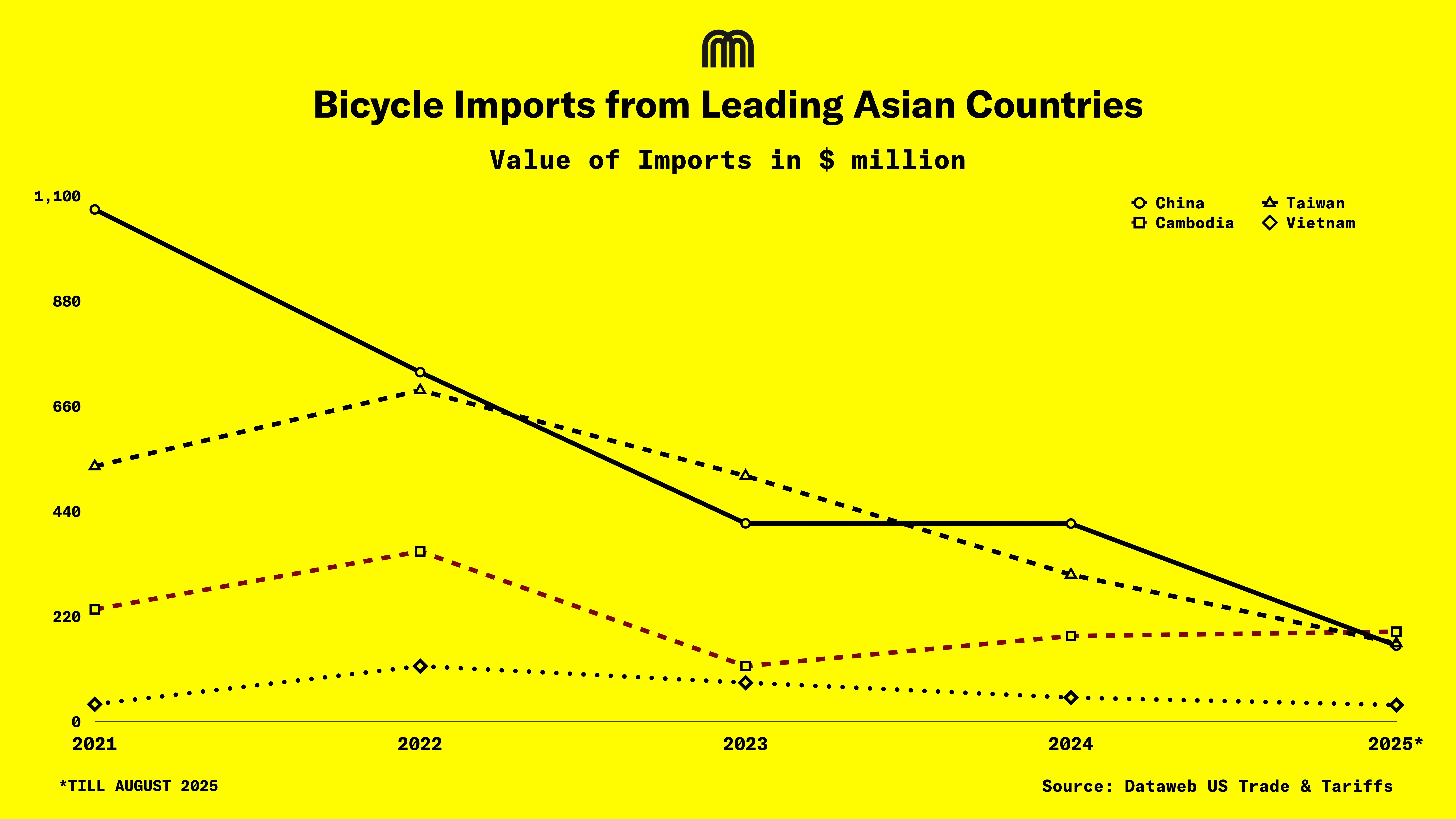

Imports Plunge After Tariff Hikes

U.S. bicycle imports (excluding e-bikes) fell 10% in July and 11% year-to-date, totaling $530m. While import volumes dropped significantly to 4.87m units compared to the previous year, the average customs value per bike rose to $108.69, indicating a market shift toward higher per-unit costs despite declining overall quantities.

Vietnam's U.S. bike exports experienced extreme volatility in the first half of the year, swinging between sharp monthly declines and a 72% surge in June, ultimately finishing effectively flat (+0.1%). These wild fluctuations were driven by uncertainty over reciprocal tariffs, which at one point threatened to reach 46%, then dropped to 10%, and finally settled at a negotiated 20%. While Vietnam exports fewer traditional bikes than its neighbors, it remains a vital production hub for premium e-bikes.

Manufacturers Reaction to Market Shifts

In August 2025, some high-end brands, such as Riese & Müller, temporarily halted U.S. imports of e-bikes following the Section 232 steel tariff announcement to assess financial viability.

Aventon announced it shifted 100% of its e-bike production to Thailand in early 2025, opting for a new factory partnership. The company stated that the move increased its manufacturing and logistics costs by about 10-15%, but that it would absorb most of the extra cost rather than simply raising retail prices.

Aventon will not be bringing the e-bike manufacturing to the US, citing a lack of domestic supply chain for key components like motors, batteries, and controllers.

In April 2025, Giant acknowledged that rising import costs would have to be reflected in U.S. bike prices, indicating that some models could see price hikes of more than 50%.

Giant’s 2024 revenue declined by 7% to $2.28B, while net profit attributable to shareholders plunged 62.8%. By the end of 2024, the company reduced its inventory-to-asset ratio from a high of 44% to 34%, bringing it below 2021 levels.

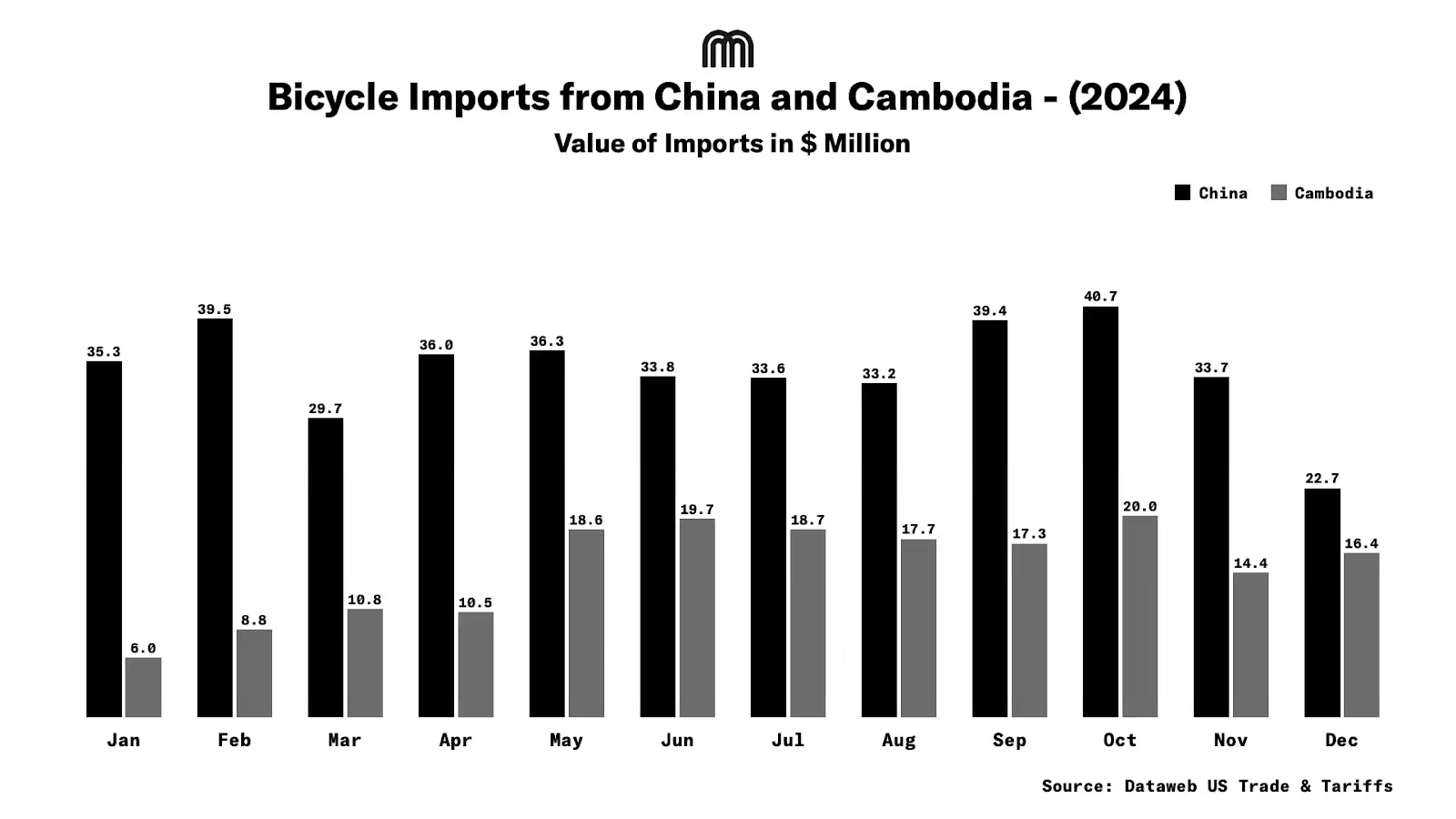

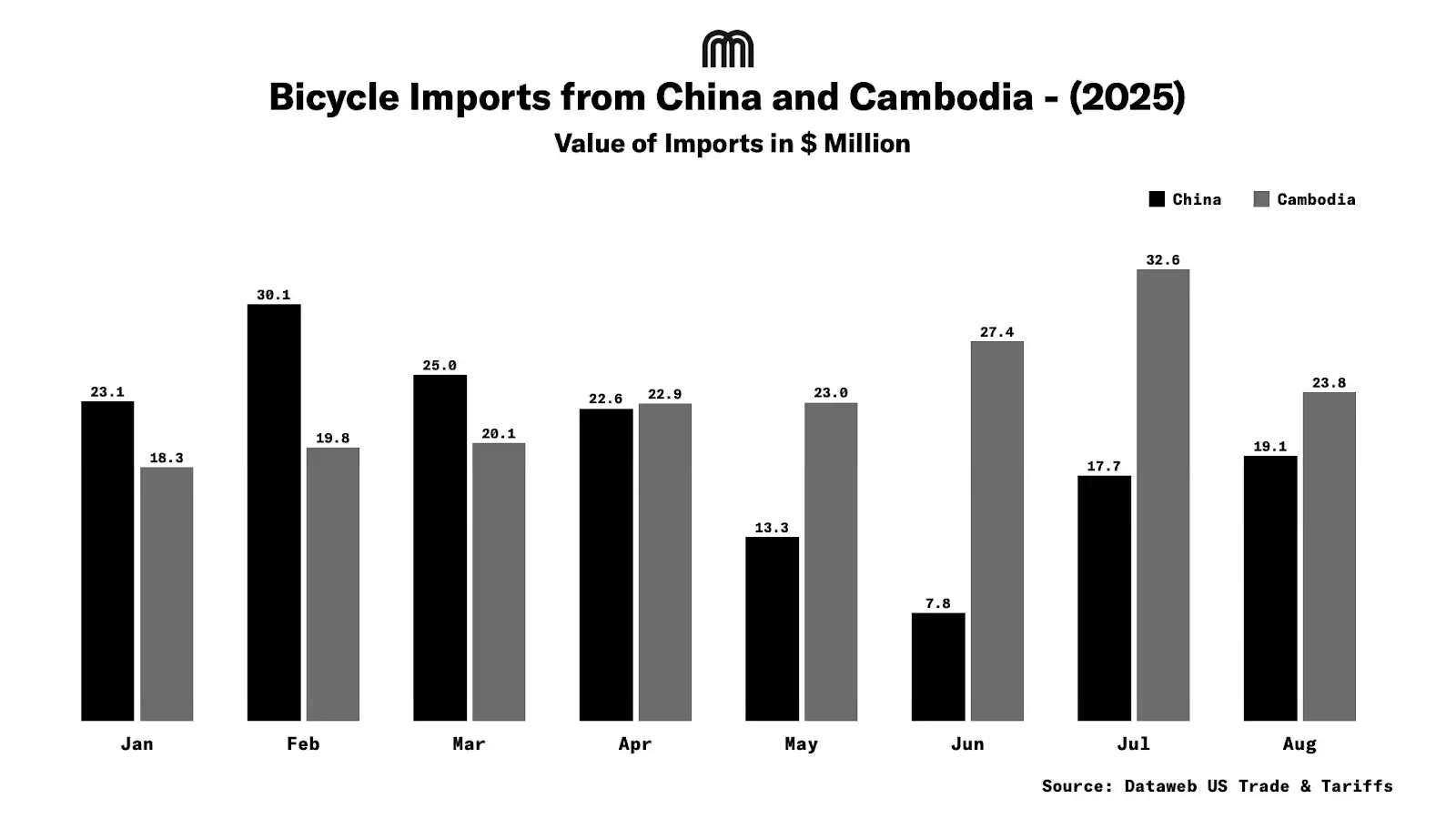

Meanwhile, Chinese bike imports to the U.S. surged 128% in July 2025 as companies rushed to beat the expected triple-digit tariffs planned for August. This panic buying followed months of declining imports, and even after the surge, volumes remained well below last year’s levels.

Specialized, a California-based bike manufacturer, took a more transparent approach by adding a separate 10% “tariff surcharge” line item on B2B invoices, rather than quietly embedding the cost into the MSRP. The surcharge is explicitly linked to the new tariff burden.

Trek and State Bicycle Co. implemented immediate price increases across “most” of their lineup.

Component Manufacturers Feel the Pinch

Component makers, both overseas and domestic, are heavily affected, sometimes even more than bike manufacturers. The reciprocal tariff logic applies not only to complete bikes and e-bikes but also to frames, forks, handlebars, stems, rims, hubs, spokes, saddles, pedals, cranks, tools, and bearings. Chinese components can face total tariffs ranging from 80% to 200%, depending on the category and timing.

As a result, component manufacturers are scrambling to re-source from non-tariffed countries, such as the UK, which has a lower 25% rate, or to shift assembly to Taiwan.

Manufacturers Countering the Tariff Impact

Reshoring to the U.S.: One notable move was Guardian Bikes’ announcement of a $19 million financing deal to launch a large-scale bicycle frame manufacturing and assembly operation in Seymour, Indiana. This is a direct effort to rebuild U.S. manufacturing capability that had been offshored for decades.

"China Plus One" Strategy: Manufacturers have broadly accelerated the implementation of a "China Plus One" strategy, relocating assembly and component production to Southeast Asian countries.

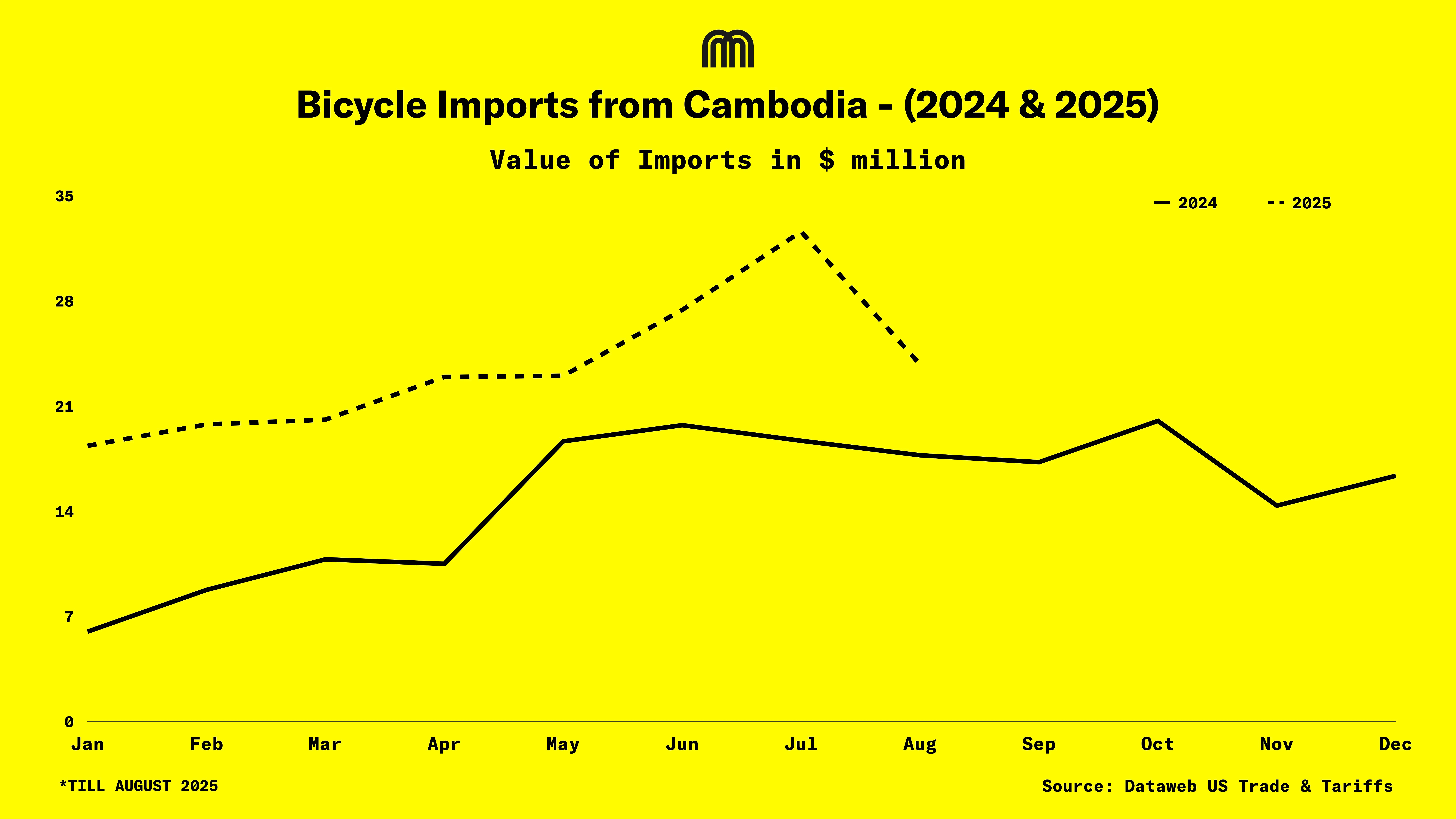

Shifting to Vietnam and Cambodia: Even before the new tariffs were finalized, manufacturers considered a major shift in bike and e-bike production to Vietnam and Cambodia, signaling a long-term relocation of manufacturing infrastructure.

It’s a Bumpy Road Ahead

The tariff situation, both directly and indirectly, has triggered a wave of companies declaring insolvency.

- Electric Bike Company (EBC) | Status: Chapter 7 Bankruptcy

In October 2025, this California-based e-bike assembler filed for Chapter 7 liquidation, ceasing operations immediately and selling off assets. Founder Sean Lupton-Smith noted that import duties on his specific components jumped from 25% to 55% (and sometimes higher), making his "Built in USA" business model mathematically impossible. - Rad Power Bikes | Status: Possible Shutdown in 2026

Once valued at $1.6 billion in 2021, Rad Power issued a WARN notice to employees in late 2025, signaling a potential total shutdown by January 2026 if a buyer or new funding is not found. - E-Cells | Status: Shutdown

This high-power, dual-motor e-bike brand announced a complete cessation of operations in May 2025. The founder cited "unforeseen circumstances," specifically pointing to extreme tariff increases on Chinese e-bikes that reached a staggering 170% in total duties for their specific category, rendering their business model unsustainable overnight. - CSS Composites | Status: Ceased Operations

CSS Composites shut down on September 30, 2025. This is a significant blow to the premium market, as CSS manufactured OEM rims for major brands such as Chris King, Trek, Evil, and Revel.

Higher Costs, Leaner Industry

The immediate impact of the compounded tariffs is a market fundamentally reshaped by cost rather than demand. While manufacturers have responded quickly with price increases and strategic shifts to other Asian countries for sourcing, the financial toll is evident in a wave of bankruptcies. The future U.S. bike landscape will likely feature higher consumer prices and a permanently consolidated, geographically diversified industry base.